What Exactly Is “Decentralized Finance”?

This post is the first in a three-part series on “Decentralized Finance – a Hype, a Threat or an Opportunity for Regulated Financial Institutions?”

Decentralized Finance (DeFi) has been one of the dominant trends in digital assets at least since the DeFi summer 2020[1]. Since the summer of 2020, the digital assets community’s gaze has turned towards the possibilities of a decentralized financial ecosystem, DeFi applications have become highly popular and the prices of corresponding tokens have multiplied. Why is DeFi seen as having such great potential and what does this mean for regulated financial institutions? In the next three blogposts, I will outline these and other questions, show different perspectives and provide an outlook on the opportunities for regulated financial institutions in the context of DeFi. To get started, this blog post will outline the functionalities of DeFi applications, present selected use cases, and highlight opportunities and risks in this context.

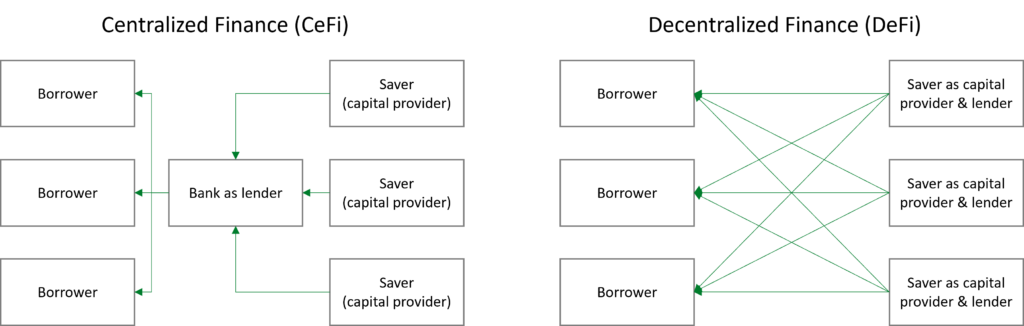

The term DeFi refers to a decentralized, blockchain-based architecture for processing financial transactions, which functions without central intermediaries[2]. Financial transactions in this context include lending, trading on decentralized exchanges (DEX), automated asset management (AAM) or decentralized insurance services[3]. These are comparable to traditional financial transactions, which to date can only be accessed and processed with the involvement of intermediaries such as banks, centralized exchanges or licensed asset managers (centralized finance, CeFi). DeFi applications, on the other hand, are open to anyone who has a wallet with the respective digital assets. Consequently, the majority of financial transactions in DeFi applications are settled directly peer-to-peer (P2P), i.e., from end user to end user. The following sketch illustrates the differences between DeFi and CeFi:

Intermediaries in the traditional financial business create inefficiencies in the execution of transactions, but they also create security and trust because they have to obtain a license and are monitored by the state. This logically leads to the question of how DeFi applications without central intermediaries can ensure a comparable level of trust.

Building trust through blockchain-based smart contracts

For building trust in the context of DeFi, the use of blockchain technology and the shift of responsibility for assets to the investor plays a major role.

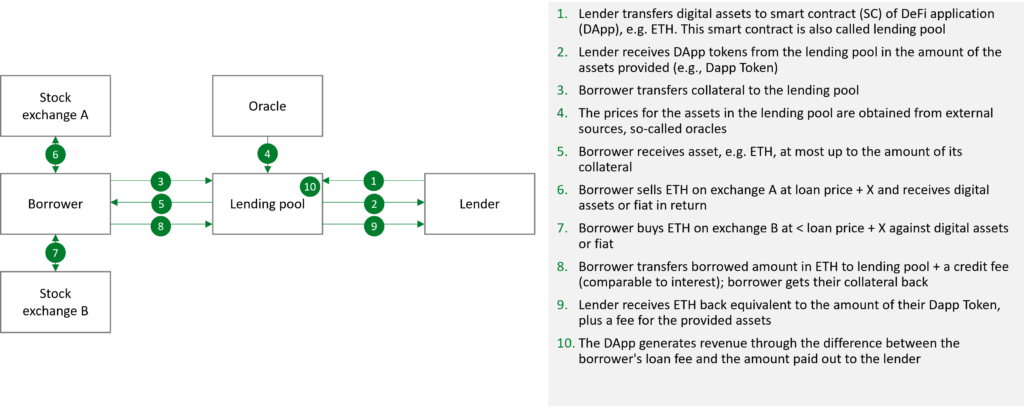

Blockchain technology ensures fundamental transparency as well as the basic tamper-resistance of transactions. Consequently, the use of a blockchain represents a strong trust-building measure. However, this alone is not sufficient to completely replace intermediaries, as the pure blockchain infrastructure does not mediate supply and demand. Intermediaries are replaced by digital, programmable contracts, so-called smart contracts, which execute a predefined action (e.g., a transaction of digital assets) based on a predetermined input. Blockchain-based smart contracts (SC) are essential components of any DeFi application. They enable indirect interaction between users of a DeFi app (e.g., borrower & lender in the case of decentralized lending) without involving an intermediary for reliable transaction processing. Using decentralized lending for arbitrage trading as an example, the processes of a DeFi transaction using a smart contract are outlined in the following figure:

Since there is no certainty that the borrower will repay the loan, the collateral to be deposited must be higher than the loan amount. This is referred to as an over-collateralized loan[4], which is used to repay the debt and the corresponding DeFi application fees in the event of a default by the borrower.

The smart contract forms the central component of the DeFi app by assuming the role of a trusted entity. Based on the defined parameters, such as the amount of the collateral, yield curve, supply & demand or digital assets involved, the SC is always executed in the same way under the same conditions. For more complex use cases, different SCs are combined and build on each other.

A smart contract receives information & data from both other blockchain applications (on-chain) and non-blockchain applications (off-chain). With off-chain data, the challenge is to ensure that the data provider is acting in an honorable manner and not providing false data to the smart contract. An off-chain data source for a blockchain-based application is called oracle and can provide, for example, fiat prices for the digital asset or weather data. Smart contracts rely on this data to bridge the gap between the blockchain and the physical world. In the example above (see Figure 2), the smart contract also requires data from an oracle: In step 2, the lender receives a reward in the form of a DeFi token for the capital provided. The amount of the reward depends on the current market value of the paid-in digital asset; the information about the market value must be obtained from an oracle.

One solution, for example, is the Chainlink protocol, which bridges the gap between on- & off-chain applications. Via application programming interface (API interface), oracles can provide data for the applications on the blockchain. In Chainlink, data providers are encouraged to behave correctly through various technical and economic measures, e.g., data providers operate a node, stake the protocol token LINK, and receive revenue paid out in LINK. The more LINK tokens that are staked, the greater the likelihood that this node will be selected as a data source and thus paid in LINK by the requesting smart contract. If the data is incorrect, the node operators may lose staked tokens[5].

Selected Use Cases of Decentralized Finance

The DeFi example “Borrowing & Lending” is a use case that enables P2P financial transactions by means of smart contracts. Two further use case examples for DeFi applications are listed:

Decentralized Exchanges (DEX)

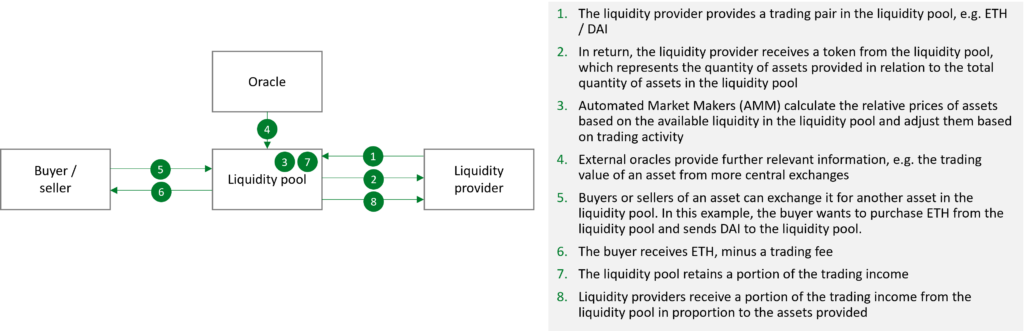

Decentralized exchanges take over the role of central exchanges, e.g. SIX in Zurich or the London Stock Exchange, by automatically matching buy and sell orders. They offer liquidity providers, buyers and sellers of digital assets a decentralized liquidity pool. The liquidity for trading is provided by the liquidity providers, the participants who make a trading pair available in the liquidity pool. In a liquidity pool for ETH/DAI, for example, a liquidity provider would transfer ETH and DAI to the corresponding smart contract, in a ratio that corresponds to the current market value of this trading pair. Trade orders are then executed using the liquidity available in the liquidity pool. Trading prices are set by special smart contracts called automated market makers. In the case of centralized exchanges, this is done by taking into account supply & demand on the trading venue. An AMM algorithm, on the other hand, calculates the price of an asset by relating the quantities of the two assets in a trading pair, thus mapping the demand for an asset. For example, if the amount of ETH in the liquidity pool is reduced and the amount of DAI is increased in a trade, the relative price of ETH will be increased and that of DAI will be reduced based on the mathematical formula underlying the algorithm. Due to the decentralized nature of DeFi and the P2P approach, all participants can act as liquidity providers and create their own liquidity pool. An alternative to AMM is on- or off-chain order books, comparable to traditional centralized exchanges. However, it can be observed that AMM increasingly replace more centralized order books on DEX.

One of the advantages of DEX is that the trade takes place by means of an atomic swap between the parties, i.e. the traded assets are exchanged simultaneously. Thus, the counterparty risk, i.e. the risk that one party does not fulfill its obligations, is greatly reduced. Another advantage is that digital assets remain in the possession of the buyer or seller until the actual trade (in contrast to traditional and/or central exchanges, which require the delivery of the asset to be traded prior to the trade, and thus direct control over the asset is ceded to an intermediary).

Automated Asset Management

DeFi applications use smart contracts to settle financial transactions with digital assets. Borrowing or lending and trading on a DEX are isolated use cases on specific DeFi applications. However, if a token holder wants to use different protocols and/or different DeFi use cases, it may be worthwhile to use Automated Asset Management (AAM). AAM are DeFi applications that follow specific investment strategies, comparable in principle to those in the traditional world. There are different strategies and focuses, e.g. yield (interest), borrowing / lending, liquidity providing (DEX) or staking (ensuring the consensus mechanism of a blockchain). Well-known platforms include Yearn.Finance or Aave.

The investor transfers digital assets (e.g. ETH) to the respective smart contract of the protocol, which is also called “vault” in the case of AAM. In return, the investor receives a token that represents the transferred assets – at Yearn.Finance, for example, this would be the token yETH. In the vault, the digital assets are implemented according to the predefined strategy by means of appropriately programmed smart contracts, e.g., the vault SC transfers a portion of the assets to a lending application and receives a reward for this in the form of the respective token. The investor participates in the return of the vault by increasing the value of the respective token (in this case yETH) or the investor receives additional tokens of the respective DeFi application; these additional tokens can be traded without reducing the size of the invested assets.

Advantages of AAM are, among others, the easy accessibility or also the yield possibilities, which exceed the classic investment returns at banks many times over (for USDC, for example, up to 7.25% rewards[6] are paid out, this in contrast to a savings account at a bank with currently <0.1% interest). On the other hand, the security of the decentrally invested assets depends on the quality of the smart contracts and a faulty programmed or hacked SC can mean a total loss.

Interest in DeFI Is Increasing

Interest in investing in the context of DeFi continues to grow, as can be observed in the rising total value locked (TVL). TVL refers to the value of assets within DeFi applications that are deposited as collateral for loans. Since loans in DeFi applications must generally be overcollateralized, it can be assumed that the amount drawn in the form of loans from borrowers is somewhat lower. An exception to this are so-called flash loans, which are completely settled within a block transaction and do not require collateral. If the borrower is not able to repay the borrowed assets, the flash loan is not settled within the block and the transaction thus never took place. Main applications for flash loans include arbitrage transactions. Since DeFi Summer 2020, the TVL has developed impressively and currently stands at around USD 229 billion:

DeFi applications are often controlled by the community or token holders using governance tokens[7]. By means of governance tokens, holders can influence decisions, e.g., they can prioritize projects on the development roadmap or set trading fees on a DEX. Often, a governance token is equivalent to a vote that can be cast in a DeFi application context (but the token remains owned by the token holder). Governance tokens are often, in theory, the only way to ensure true decentralization of the application, in that all token holders have equal voting rights per token and no one person controls the protocol alone. In practice, however, the development team may receive a large portion of the governance tokens as an incentive for their work, which in turn has a negative impact on decentralized decision making. On the other hand, this also means that there is often no legal recourse against a legal entity.

Advantages & Risks of DeFi Applications

Compared to the classical financial system, DeFi holds various advantages:

- Accessibility: Any investor with a wallet as well as the corresponding digital assets can participate in DeFi applications. This leads to a more inclusive financial system

- Counterparty risk: Atomic swaps within a smart contract drastically reduce counterparty risk and increase security for all parties

- Speed & control over assets: The use of blockchain technology and smart contracts makes it possible to settle financial transactions much faster. Compared to traditional investments, which are often settled after 2-3 days, the period is reduced to a few minutes. Due to the immediate control over the assets on the wallet via private key, users only have to transfer the assets to the respective DeFi app when there is an immediate intention to trade. In traditional stock trading, the securities must be booked into the investor’s securities account at the bank before the trading order is placed, so the investor has already relinquished direct control to the bank before any actual intention to trade. Due to the lack of intermediaries, the assets remain under the investor’s control for longer in the context of DeFi.

- Return opportunities: Compared to traditional forms of investment, investments in the context of DeFi offer new and currently higher earnings opportunities, e.g., a price gain of a digital asset or the earnings for providing assets in a liquidity pool of a DEX. Due to the comparatively lower liquidity on DeFi borrowing/lending applications compared to traditional money markets, lenders can achieve higher interest rates[8].

- Decentralized infrastructure: The decentralized infrastructure of a blockchain, and thus of a DeFi application, prevents all assets from being threatened at once in the event of a hacker attack on a central entity (e.g., a central crypto exchange)

Notwithstanding the benefits of DeFi applications, the use cases as well as the technology are still young and carry various risks:

- Regulation: Regulated intermediaries are usually subject to supervision and auditing of their business activities. DeFi applications are currently exempt from supervision and are not audited by any government agency. However, some efforts are underway to regulate or even restrict the business activities of DeFi applications (e.g. Markets in Crypto Assets in the EU).

- Code is law: The correct programming of the smart contract(s) is crucial for the security and correct functioning of the DeFi application. If smart contracts have errors or security vulnerabilities, this can lead to the loss of the entire investment. An example of this is the DAO hack of 2016, in which ETH worth over USD 60 million were stolen at the time[9]. Especially since there is no regulation at present, there is often no possibility for the investor to receive compensation. However, initial efforts are being made in the DeFi sector to create insurance solutions for such cases (e.g. Nexus Mutal, which insures losses due to faulty smart contracts).

- Understanding DeFi: The adoption rate of blockchain by the general public is low compared to traditional financial transactions. DeFi applications represent a sub-category within blockchain technology with specific technical terms, mechanisms, and peculiarities. That is why it can be assumed that neither the general public nor public authorities possess sufficient knowledge of how decentralized finance works, and what advantages and disadvantages it may offer. This can lead to misjudgments of their own capabilities and consequently to an increased risk of loss.

- Sandwich attacks: Transactions in the DeFi context take place on a pseudo-anonymized[10], transparent blockchain. Each transaction is public before being anchored in a block and is therefore available to all interested parties. Transactions are basically processed according to the amount of the gas fee, the transaction fee for a transaction on a blockchain, which consists of a fixed fee and a variable amount that can be freely determined. If an additional order is now triggered (order B) based on the publicly visible order (order A), which anticipates the price changes due to the execution of order A and is to be executed before it, this is referred to as a sandwich attack[11]. Order B is processed before order A due to the higher gas fee, so that the assets from order B are bought cheaper (frontrunning); after the execution of order A, which increases the price of the asset, the assets from order B are sold at the higher price (backrunning). DeFi-DEX are particularly vulnerable to this, as AMM execute orders continuously as well as automatically. Technical solutions for sandwich attacks are being tested and developed (e.g. ZK snarks for increased transaction privacy[12]).

- Off-chain data sources & oracles: DeFi applications are based on the scalable and reliable application of smart contracts. Thus, oracles play an important role for the correct execution of the DeFi application. In order to reduce the risk of incorrect and potentially harmful data, appropriate measures must be taken into account when designing smart contracts, e.g. with regard to data sources & oracle operators

- Contract security & entity: If a contract is breached in the classical world, the entity (natural person and/or legal entity) behind the contract is usually held accountable. Due to the decentralized nature of DeFi applications and governance token decision making, this is often more difficult – or even impossible – than in CeFi, where a central, uniquely identifiable counterparty can be held contractually liable

- Unknown counterparty: Due to the P2P nature of DeFi transactions and the pooling of assets in permissionless DeFi applications, the counterparty is unknown prior to trading. However, there are already use cases that address this challenge via permissoned DeFi applications and only allow KYC-identified investors (e.g. Aave Arc).

- Impermanent loss: This refers to the loss suffered by the liquidity provider in the event of a price change of the asset provided on a DEX. Liquidity providers have a proportional claim on the assets in the liquidity pool, based on the percentage of the total pool balance at the time of delivery. If demand for an asset in the pool increases, its inventory decreases. When the liquidity provider subsequently receives the assets, it receives the same percentage share of the pool, but the distribution between the two assets may differ from that of the assets delivered. If the price of an asset changes (e.g. if an asset increases in value in absolute terms), it may be more lucrative for the provider to hold it and not make it available to the liquidity pool. To make it still attractive for asset owners to act as liquidity providers, DeFi protocols allow them to receive a portion of the trading fees earned as revenue.

Summary & Outlook

The concept of DeFi as well as the first use cases enable the radical rethinking of financial transactions. Particularly in view of the increasing acceptance of digital assets by traditional financial institutions, it is only a matter of time before they also move into the DeFi area. Currently, various factors are in place that prevent a comparable level of security as with classic financial transactions. On the other hand, investors are offered return opportunities that are very difficult to replicate in the traditional world. DeFi applications are currently still at the beginning of their development and a new generation of DeFi applications is already foreseeable, which will try to solve the challenges known today.

What opportunities and challenges regulated financial institutions face in this context will be discussed in the next blogpost on DeFi in May.

[1] Main blockchain and crypto trends in 2022 – unexpected expectations (Finextra, 2021), abgerufen am 28.3.2022 von https://www.finextra.com/blogposting/21453/main-blockchain-and-crypto-trends-in-2022-unexpected-expectations

[2] E.g. Decentralized Finance DeFi: An Alternative Financial System? (Morgan Stanley Research, 2022)

[3] Decentralized Finance (Ethereum.org, 2022), abgerufen am 29.3.2022 von https://ethereum.org/en/defi/#what-is-defi

[4] Sicherheiten in DeFi (Bitcoin Suisse, 2021). Abgerufen am 31.3.2022 von https://www.bitcoinsuisse.com/de/research/decrypt/sicherheiten-in-defi

[5] Weekly Broker – Chainlink – A decentralized oracle network (Crypto Finance, 2021) ; abgerufen am 15.4.2022, von https://www.cryptofinance.ch/en/weekly-broker-chainlink-a-decentralised-oracle-network/

[6] Crypto Lending Interest Rate April 2022 (DeFi Rate, 2022); abgerufen am 15.4.2022, von https://defirate.com/lend/

[7] What are Governance Tokens? How Token Owners Shape a DAO’s Direction (Decrypt, 2022); Abgerufen am 1. April 2022 von https://decrypt.co/resources/what-are-governance-tokens-how-token-owners-shape-dao

[8] E.g. Decentralized Finance DeFi: An Alternative Financial System? (Morgan Stanley Research, 2022)

[9] What Was The DAO? (Gemini.com, 2022); Abgerufen am 15.4.2022, von https://www.gemini.com/cryptopedia/the-dao-hack-makerdao

[10] The transactions and balances on wallets on a public blockchain are transparent and can be viewed by anyone. However, the owners of the wallets are not known, which is why the term “pseudo-anonymized” is used.

[11] Analyzing and Preventing Sandwich Attacks in Ethereum (Patrick Züst, 2021); Abgerufen am 4.4.2022 von https://pub.tik.ee.ethz.ch/students/2021-FS/BA-2021-07.pdf

[12] ZERO-KNOWLEDGE ROLLUPS (ethereum.org, 2022); Abgerufen am 15.4.2022, von https://ethereum.org/en/developers/docs/scaling/zk-rollups/

- Positioning opportunities for banks in the context of digital assets – A market observation - 13.02.2024

- Tokenization – Potentials, Challenges and Use Cases in the Environment of the Financial Industry – Part 2 - 06.06.2023

- Tokenization – Potentials, Challenges and Use Cases in the Financial Industry Environment - 14.02.2023