Tokenization – Potentials, Challenges and Use Cases in the Financial Industry Environment

In connection with blockchain technology, the financial industry often talks about the tokenization of assets and attributes enormous potential to it. In this context, rights to values, e.g. to assets such as securities, commodities or even non-bankable assets such as works of art or classic cars, are securitized in the form of a token on a blockchain[1]. In 2022, a study by the Boston Consulting Group (BCG) put the potential of tokenized assets at around USD 16 trillion by 2030 (around 10% of global gross domestic product in 2030)[2]. Here, BCG refers to assets as both more liquid assets, such as listed stocks, and more illiquid assets, such as unlisted stocks, real estate, or non-bankable assets. The term non-bankable assets refers to assets that are very difficult or impossible to represent in a portfolio in a traditional financial environment, e.g. intellectual property rights, classic cars, etc.[3]. In the context of the supposed potential of tokenized assets, it is worth taking a more detailed look at the definition of the term at the outset. Over the past two years, there have already been several posts on this blog about tokenization[4]. Complementing these, the first part of this series of posts discusses potentials and challenges of tokenization in the context of the financial industry. Selected use cases are presented in the second part and positioning opportunities for financial institutions are outlined in the third part.

Tokenization of (Asset) Values

The term “token” can be defined from different perspectives, e.g. in the context of security mechanisms for card payments. There, a token contains encrypted information on credit or debit cards, although there is not necessarily a reference to a blockchain[5].

A different view of the term “token” describes it as a digital representation of rights and obligations related to an object of value, e.g., the Liechtenstein Token and Trustworthy Technology Service Providers Act (TVTG) describes a token as “a piece of information on a TVTG system that may represent claim or membership rights against a person, rights in property, or other absolute or relative rights; and is associated with one or more TT [trustworthy technology] identifiers”[6]. A TVTG system describes a blockchain and TT identifiers are identified, unique beneficial owners of the token.

For the discussion in this paper, the definition from the TVTG is used as a basis, as the potentials and challenges discussed are described in the context of the financial industry.

In addition, BaFin understands the term “tokenization” to mean the securitization of values in the digital space by means of blockchain-based tokens. This token contains all rights and obligations inherent to the underlying value and is in principle transferable[7]. Based on the previous definitional approaches, for this series of articles a token is understood to be a digital container that can contain rights and obligations to an object of value. The token is technically based on a blockchain and is transferable. How a token behaves compared to a traditional securitization of rights and obligations is shown in the example below:

- Rights and obligations: In the case of a traditional security, holders are often entitled to a portion of the distributed dividend or can exercise voting rights (e.g., in the case of shares). A tokenized security (either in the form of a digital representation of an already issued share or issued natively on a blockchain) includes the same rights and obligations as its traditional counterpart.

- Transferability: An exchange-traded, traditional security can in principle be sold or bought on a central trading venue; it is therefore transferable. A token backed by a security can also be transferred to others from a technical perspective. In both cases, however, it is not the effective security that is transferred, but the rights and obligations associated with the security.

- Validity: Depending on the applicable regulation, tokenized securities are treated equally to their traditional counterparts, e.g. Switzerland has a corresponding anchoring in the Swiss Code of Obligations with ledger-based securities[8].

In addition to rights and obligations to securities, other rights and obligations can be represented in the form of a token, e.g., rights of use or subscription rights to things. Thus, the token on a blockchain serves in its essence as an almost forgery-proof representation of one or more rights. This principle is relevant to the rest of the discussion, as it gives rise to further use cases. In the example above, tokenization was illustrated using a traditional security. In contrast to a fundamentally liquid asset – such as an exchange-traded stock – various assets exist with much lower liquidity (e.g., real estate, artwork, private market investments, or non-exchange-traded stocks). Based on this, the question arises as to what concrete potential the tokenization of assets holds as well as what challenges need to be addressed.

Exemplary Potentials of Tokenized (Asset) Values

Various potentials are attributed to tokenization, e.g. higher efficiency in the settlement of and trading in assets, the development of new target groups or the decentralization of investments. In the introductory example, tokenization was illustrated using a traditional security. However, in contrast to a liquid asset – e.g., an exchange-traded stock – various assets exist with much lower liquidity (e.g., real estate, artwork, vintage cars, private market investments, or non-exchange-traded stocks). The low liquidity has a direct impact on access to these assets and their operational settlement. The former affects the amount of minimum investments (e.g., so that the value asset is acquired first by the cumulative amount of investments). Furthermore, due to their nature, the valuable assets are often only of (emotional) value to a special group of investors, e.g. art objects from a certain era or luxury automobiles. A direct influence on the operational settlement of such an illiquid asset is, for example, the complex pricing process, since the price is made up of, among other things, the redeemed and resold shares as well as the performance of the underlying asset. In addition, settlement and trading are resource-intensive, since, for example, the origin of an artwork has to be elaborately processed or trading is often only possible through manual or partially automated steps. These factors mean that providers of illiquid assets incur high costs for pricing or processing transactions. In addition, due to the comparatively high barriers to entry, these assets are often only accessible to a limited group of investors, including those with specific prior knowledge or the required capital resources. This is where the blockchain-based representation of the asset as a token comes in. In the following, exemplary potentials are presented based on illiquid assets. Further use cases will be discussed in a later part of this series of articles.

Efficiency in Processing and Trading

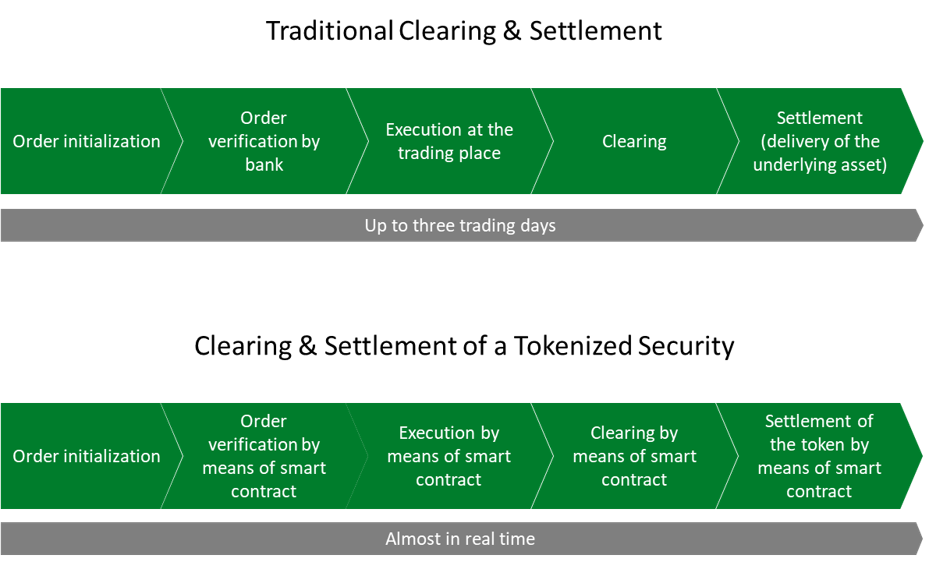

Traditional settlement and trading of illiquid assets involves a variety of intermediaries that provide part of the value chain. For the trading of an illiquid asset, such as real estate or a raw material, the transfer of the asset from the seller to the buyer takes place through several steps. In particular, there is often a discrepancy of several days between the effective purchase, the delivery of the asset, and the transfer of legal control of the security to the buyer (e.g., registration in the shareholder register) [9]. The graphic below shows an example of the advantages of a transfer via token compared to a traditional settlement involving various intermediaries:

As the above example shows, the use of tokens in conjunction with smart contracts[10] enables significantly higher transmission speeds. In particular, disintermediation takes place, i.e. central parties from traditional trading (e.g. a Central Security Depository) are no longer required due to peer-to-peer transmission. The almost immediate settlement between payment and delivery can reduce the cost of capital for both buyer and seller[11]. In addition, smart-contract-based settlements (e.g., in the form of atomic swaps across two different blockchains[12]) also further reduce counterparty risk. In combination with decentralized fnance (DeFi) applications, entirely new settlement and trading opportunities may emerge, e.g., in decentralized marketplaces[13]. Use cases in this context will be taken up again in the third part.

Tokenization of securities offers companies the opportunity to efficiently issue their own securities in the form of tokens. In contrast to a traditional issue of securities, automated issuing and trading platforms are used here[14]. Through standardized tokens as well as in accordance with the legislation applicable to the respective issuing company, security tokens can be issued. The special feature of security tokens is that they make a regulated security tradable on the blockchain by means of tokens. The security token is subject to the same requirements as a non-tokenized security, e.g. with regard to prospectus requirements. The issuance of a tokenized security offers cost advantages for issuers, as e.g. neither investment banks nor brokers are necessary for the placement of the issue amount with investors and the potential investor base is significantly higher due to the digital availability of the token[15].

Development of New Target Groups

Due to the often necessary minimum investments in illiquid assets and the high complexity of these financial products, a rather small but financially strong target group is addressed. Consequently, the potential target market for such investments is small relative to the total investor base and the costs incurred are spread over fewer players and investors. Initial attempts to fractionalize assets and tap into a larger target audience have been made even without the use of blockchain technology. Examples include exchange traded funds (ETF)[16], which, for example, track an index and invest proportionally in the securities traded in the index. Investors purchase the ETF and participate in the performance of the securities in the respective index without directly purchasing each individual security. ETFs are described as relatively liquid because they can be traded on exchanges during trading hours.

By means of tokenization, minimum investments can be set at a level that can open up a large number of new, potential investors. This is possible because investors no longer purchase the entire asset (e.g., the entire property), but only a portion of it. In the traditional acquisition of a property through bank financing, equity is required from investors, e.g., around 40 percent of the income value of the property[17]. If, on the other hand, a tokenized share of an income property is acquired, no equity is required for the financing and it is still possible to participate in the performance of the property as well as the income. In addition to the often high prices of the assets as well as equity requirements, there are traditionally other cost drivers, e.g. the periodic calculation of the net asset value (NAV) in the case of a fund or the distribution costs of issuers, i.e. bringing together investors and owners of real estate, which are eliminated by tokenization. As described at the outset, tokenization offers various potentials for settlement and trading. In combination with fractionalization, fundamentally lower minimum investments can be targeted and thus a larger investor group can be addressed. In addition to real estate, other non-bankable assets can be made available to a broader investor base, such as works of art. Various companies offer investment in such goods by means of tokens, thereby enabling investors to participate in the long-term performance with a low initial investment[18].

Emotionalization of an Asset

Through the tokenization of non-bankable assets, investments can be made in values that previously could not be realized efficiently. Investors can, for example, acquire a share in a unique work of art[19] or directly support their favorite athlete by co-financing his employment contract of several years. Thus, investments in highly emotional values are possible and become visible through tokens in the wallet. Not only purely emotional considerations play a role in these investments, but also legal or financially very practical ones. Often, in an inheritance case, the existing assets are divided between the heirs according to the law in combination with the last will. If all assets have a certain liquidity, the heirs can be paid out comparatively quickly and efficiently. This contrasts with illiquid assets, which often also have a high emotional value for the heirs, e.g. a work of art or the family ancestral home. In order to prevent a sale for the purpose of paying off the heirs, the tokenization of the asset is a suitable solution. As a result, the tokenized assets can be pledged and the liquidity thus gained can be used to pay out the heirs.

Another form of emotionalization of investments is created by non-fungible tokens (NFT). These are tokens that basically represent a specific asset on the blockchain, e.g. a specific image or a clearly identifiable object. This is comparable to the tokenization of other assets, but NFTs are unique in their form and not exchangeable (“non-fungible”), i.e. NFT A does not represent the same underlying asset as NFT B. This allows (virtual) items, e.g. unique items from computer games or trading cards, to be tradable and usable by their owners.

Decentralization of Investments and Transparency

Traditionally, an intermediary provides access to securities, e.g., as shares in a customer’s custody account. Thus, investors pass on operational risks associated with the custody and handling of securities to the intermediary in exchange for a fee. Investors not only pay for custody, but are also dependent on the intermediary’s business activities, e.g., the intermediary’s trading hours or whether a particular asset is offered through the intermediary.

In the case of tokenized assets, the effective power of disposal over the token is exercised directly by investors, e.g. by keeping the token in a non-custodial wallet. A non-custodial wallet is a custodial solution for private keys in which the user manages their keys themselves; if, on the other hand, the management of the private keys is delegated to third parties, this is referred to as a custodial wallet[20]. Investors who store their private keys in a non-custodial wallet exercise complete control over the tokenized asset until the effective trading date. The decentralized custody of assets can bind investors more closely to their investment or further emotionalize them. Likewise, the decentralized custody of tokenized assets offers a lower counterparty risk, as full control is exercised over the asset itself and there is no dependence on a central custodian.

The use of blockchain technology can fundamentally increase the transparency of transactions or assets held. This is particularly advantageous for non-bankable assets when art objects or commodities are mapped in token form. The trading history can be transparently traced across different stations using the token. The prerequisite for this is the use of a corresponding blockchain, e.g., a public blockchain, which can be viewed by third parties as desired in the sense of an open-source approach. An additional requirement for efficient tradability is that during initial tokenization – analogous to the establishment of a banking relationship – the origin of the asset or the beneficial owners are verified within the framework of the usual AML, KYC or CTF guidelines. End-to-end decentralization is therefore not given here either.

Based on the preceding examples, it is clear that tokenization of assets holds various potentials. On the other hand, the widespread adoption of tokenized assets has not yet taken place, partly because some challenges have not yet been solved.

Challenges

Infrastructure and know-how

For an offering of tokenized assets, not only are corresponding underlying assets necessary (e.g., the artwork, the illiquid asset, etc.), but corresponding infrastructure components must also be provided. This includes, for example, smart contracts for the creation (minting) or redemption (burning) of the token, the definition of the information stored in the token (e.g., entitlement to dividends, participation or usage rights) or the governance model to control the setup. In particular, the governance of a decentralized trade with blockchain-based tokens is challenging in a business model designed for centralized service provision. Issues need to be resolved, for example, in the context of on-chain and/or off-chain governance (e.g., who has the right to issue, redeem, or destroy tokens) or what consensus mechanism should be used to validate transactions on a blockchain[21]. Initial efforts by large custodians from the traditional sector are underway[22], but there is still a long way to go before an efficient infrastructure can be deployed across the board.

Another challenge is the connection of blockchain-based infrastructure (e.g., custody, token issuance, etc.) to existing systems. Here, for example, technical questions arise regarding interfaces (e.g., API or FIX interfaces) or mapping in core systems. Various questions need to be clarified, e.g. how a settlement of t+0 can be mapped in a traditional core system if all operations are aligned to at least t+1[23][24].

Additional complexity arises when the infrastructure for tokenizing value is viewed from a business ecosystems perspective: The fragmented service provision to end customers by orchestrators, providers and contributors[25] gives rise to further challenges, which will be addressed in a later part of the series of contributions. Examples include the additional need for coordination between the participants, the definition of operational standards such as the design of tokens, and data exchange. It is not only the management of the companies involved that is affected, but the entire organization, as it involves a large number of interaction fields (e.g., data exchange, regulation, etc.). The greatest challenge in the context of infrastructure for products and services in the context of tokenization is to avoid mapping the current infrastructure 1:1 in a setup that tends to be less stable[26].

Know-how is not only relevant for infrastructure operators, but also for investors. Due to the safekeeping of the token in a non-custodial wallet, investors require basic knowledge in dealing with blockchain-based technologies as well as a corresponding risk awareness. If the token is sent to an incorrect address during a trading activity, various steps must be taken to declare it invalid and send new, equivalent tokens to the investor’s wallet.

From a regulatory perspective, the first laws have come into force, e.g., the DLT Act in Switzerland[27] or the TVTG in Liechtenstein[28]. Other laws are in a pilot phase e.g. the DLT pilot regime in the EU, or will only come into force in the next few years e.g. MiCA in the European Union[29]. First use cases of tokenized values are depicted in the mentioned laws, e.g. the transfer of rights as tokens in the TVTG from Liechtenstein. The formulation of principles on other topics, e.g. non-fungible tokens (NFT) or decentralized finance, is only being discussed in expert groups[30] and is still a long way from implementation. This poses the challenge that the implementation of use cases covered by regulation must take place within very narrowly defined framework conditions (e.g. the offering of tokenized art by a bank in Switzerland[31]).

Tradability in the Secondary Market and Liquidity

Particularly for illiquid assets, tokenization is intended to achieve higher liquidity and thus faster tradability and price discovery in the market. This requires regulated secondary markets that are comparable to traditional stock exchanges and trading venues such as the LSE or the SIX Swiss Exchange. The advantage of traditional trading venues is, among other things, the high liquidity of the traded securities and the highly automated pairing of buyers and sellers. The first regulated marketplaces for tokenized assets are already available, e.g. the SDX of the Swiss Stock Exchange or the SMEX of the Berner Kantonalbank. So far, both trading venues have a very low number of tradable securities and low trading volumes compared to traditional exchanges.

Tokenization of assets does not per se ensure that the liquidity of the asset is increased or that there is regulated tradability. Rather, it provides the basis for improving this or making the asset tradable in a scalable manner. Liquidity is often provided by so-called market makers, who place buy and sell orders on the exchange and simultaneously hedge on other trading venues, each with opposing orders[32]. In addition to the use of existing trading venues for tokenized assets, the available liquidity of the traded assets represents a key element for the further spread of tokenization. Without corresponding demand, the potentials addressed in settlement and trading cannot be exploited to an extent that would make a switch from the established infrastructure to new marketplaces economically interesting. With the DLT pilot regime, a “regulatory sandbox” was created in the EU in 2022 to test a DLT-based financial market infrastructure in a regulated framework[33]. The first trading venues are emerging, but the necessary liquidity for smooth trading of tokenized assets is currently not yet available.

Initial Conclusion and Outlook

As blockchain technology continues to proliferate in enterprises and is adopted by end users, more use cases will emerge, including in the area of value tokenization. Tokenization holds some potential, but for broader use, several hurdles need to be overcome, such as limited accessibility for investors, provision of the necessary infrastructure, and the establishment of new clearing and settlement times for tokenized assets traded almost around the clock.

The next part discusses implementation examples and the positioning of financial institutions in the context of tokenization. The third part of the series of articles deals with the potential of tokenization in the context of decentralized finance and the implications it can have on the business activities of financial institutions.

Sources

[1] E.g. Was ist Tokenisierung? (Finexity, 2023); retrieved 2/6/2023, from https://finexity.com/wealth/what-is-tokenization

[2] Relevance of on-chain asset tokenization in « crypto winter » (BCG, 2022) ; retrieved 2/1/2023, from https://web-assets.bcg.com/1e/a2/5b5f2b7e42dfad2cb3113a291222/on-chain-asset-tokenization.pdf

[3] Blockchain in der Finanzbranche: Drei konkrete Anwendungsszenarien (Bulling, 2021); retrieved 02/12/2023 from https://bankinghub.de/innovation-digital/blockchain-anwendungsszenarien

[4] E.g. Towards a Framework for Understanding the Potentials of Tokenized Assets (Dick & Pohle, 2021); retrieved 2/10/2023, from https://ccecosystems.news/towards-a-framework-for-understanding-the-potentials-of-tokenized-assets/

[5] Tokenization for Debit Cards (SIX, 2021) ; retrieved 2/10/2023, from https://www.six-group.com/dam/download/banking-services/debit-and-mobile-services/en/learning-nugget/learning-nugget-tokenization-en.pdf

[6] § 2 Para. 1c TVTG

[7] Tokenisierung (BaFin, 2019); retrieved 2/1/2023, from https://www.bafin.de/SharedDocs/Veroeffentlichungen/DE/Fachartikel/2019/fa_bj_1904_Tokenisierung.html

[8] E.g. § 973 para. 1d SR/RS 22

[9] Settlement Date: What It Means for Stocks, Bonds, and Insurance (Investopedia, 2020); retrieved 2/6/2023, from https://www.investopedia.com/terms/s/settlementdate.asp#:~:text=What%20Is%20a%20Settlement%20Date,date%20(T%2B2).

[10] Advantages & disadvantages of smart contracts are described in the article “What’s behind the term Decentralized Finance?” in the section ‘Building Trust with Smart Contracts’; https://ccecosystems.news/en/what-do-we-mean-by-the-term-decentralized-finance/

[11] This includes costs incurred when capital is tied up in the transfer and cannot be used for other purposes.

[12] E.g. Was sind Atomic Swaps? (Bitpanda, 2023); retrieved 2/6/2023, from https://www.bitpanda.com/academy/de/lektionen/was-sind-atomic-swaps/

[13] Read more about Decentralized Finance in the blog post ” What Exactly Is “Decentralized Finance”?” at https://ccecosystems.news/en/what-do-we-mean-by-the-term-decentralized-finance/

[14] E.g. Securitize’s Mini-IPO solution (Securitize, 2023); retrieved 2/10/2023, from https://securitize.io/raise-capital/mini-ipo-solution

[15] Tokenization of Assets (EY, 2020); retrieved 2/10/2023, from https://assets.ey.com/content/dam/ey-sites/ey-com/en_ch/topics/blockchain/ey-tokenization-of-assets-broschure-final.pdf

[16] E.g. Was sind ETF? (VanEck, 2023); retrieved 2/3/2023, from https://www.vaneck.com/ch/de/was-sind-etfs/

[17] Ferien- & Renditeobjekte kaufen (UBS, 2023); retrieved 2/10/2023, from https://www.ubs.com/ch/de/private/mortgages/guide/financing/holiday-property.html

[18] E.g. Timeless from Germany (https://www.timeless.investments/about-us)

[19] E.g. Entdecken Sie das Potenzial von Kunst-Tokenisierung (VP Bank, 2023); retrieved 2/3/2023, from https://ch.vpbank.com/de/privatkunden/anlegen/digitale-vermoegenswerte/kunst-tokenisierung

[20] E.g. Non-Custodial Wallets vs Custodial Wallets: Know the Difference (bitpay, 2022); retrieved 2/3/2023, from https://bitpay.com/blog/non-custodial-wallets-vs-custodial-wallets/

[21] A Framework for Enabling Asset Tokenization Business Models in the Financial Services Sector (Heines, 2022)

[22] E.g. Digital Assets – At the Intersection of Trust and Innovation (BNY, 2023); retrieved 2/3/2023, from https://www.bnymellon.com/us/en/solutions/digital-assets.html

[23] “t” corresponds to the trading day; the additional time entry represents the duration for the clearing & settlement of the traded good, e.g. until the security has been booked from the seller’s securities account to the buyer’s securities account.

[24] Further challenges are highlighted in Roger Heines’ article: Need for Change – Challenges for Enterprises in Using Distributed Ledger Technology (Heines, 2022); retrieved 2/10/2023, from https://ccecosystems.news/en/need-for-change-challenges-for-companies-in-using-distributed-ledger-technologies/

[25] E.g. Das Business Model Ecosystem Canvas – eine Einführung (CC Ecosystems, 2021); retrieved 2/6/2023, from https://ccecosystems.news/das-business-ecosystem-canvas-eine-einfuehrung/

[26] How to avoid disaster in the tokenization of financial assets (Kubli, 2023) ; retrieved 2/13/2023, from https://thetokenizer.io/2023/02/07/how-to-avoid-disaster-in-the-tokenization-of-financial-assets/

[27] Blockchain/DLT (SIF, 2022); retrieved 2/3/2023, from https://www.sif.admin.ch/sif/de/home/finanzmarktpolitik/digit_finanzsektor/blockchain.html

[28] Gesetz über Token und VT-Dienstleister (LILEX, 2023); retrieved 2/3/2023, from https://www.gesetze.li/konso/2019301000

[29] Crypto regulation: the introduction of MiCA in the EU regulatory landscape (Clifford Chance, 2022); retrieved 2/3/2023, from https://www.cliffordchance.com/briefings/2022/12/crypto-regulation–an-introduction-of-mica-into-the-eu-regulator.html

[30] DeFi and Financial Market Regulation (Dünser & Guerra, 2022); retrieved 2/13/2023, from https://medium.com/@tduenser/defi-and-financial-market-regulation-4ec8843619b8

[31] Sygnum Bank and Artmundi tokenize Warhol’s Marilyn Monroe Artwork (Sygnum, 2022); retrieved 2/13/2023, from https://www.insights.sygnum.com/post/sygnum-bank-artemundi-tokenize-warhol-s-marilyn-monroe-artwork

[32] Market Maker Definition: What It Means and How They Make Money (Investopedia, 2021); retrieved 2/3/2023, from https://www.investopedia.com/terms/m/marketmaker.asp

[33] Das DLT-Pilotregime (Deloitte, 2023); retrieved 2/3/2023, from https://www2.deloitte.com/de/de/pages/audit/articles/dlt-pilot-regime.html

- Positioning opportunities for banks in the context of digital assets – A market observation - 13.02.2024

- Tokenization – Potentials, Challenges and Use Cases in the Environment of the Financial Industry – Part 2 - 06.06.2023

- Tokenization – Potentials, Challenges and Use Cases in the Financial Industry Environment - 14.02.2023