Effects of the Coronavirus Pandemic on the Financial Industry

Since the beginning of 2020, the coronavirus pandemic has caused an enormous slump in the global economy due to lockdowns all over the world. The IMF expects global GDP to decline by 5%, and for the euro zone it is likely to be as much as 10.2% [1] – and these are the figures before a possible second wave. It remains to be seen how the economy will recover. What can already be assessed fairly well, on the other hand, is the qualitative impact of the pandemic on the macro trends relevant to the financial industry.

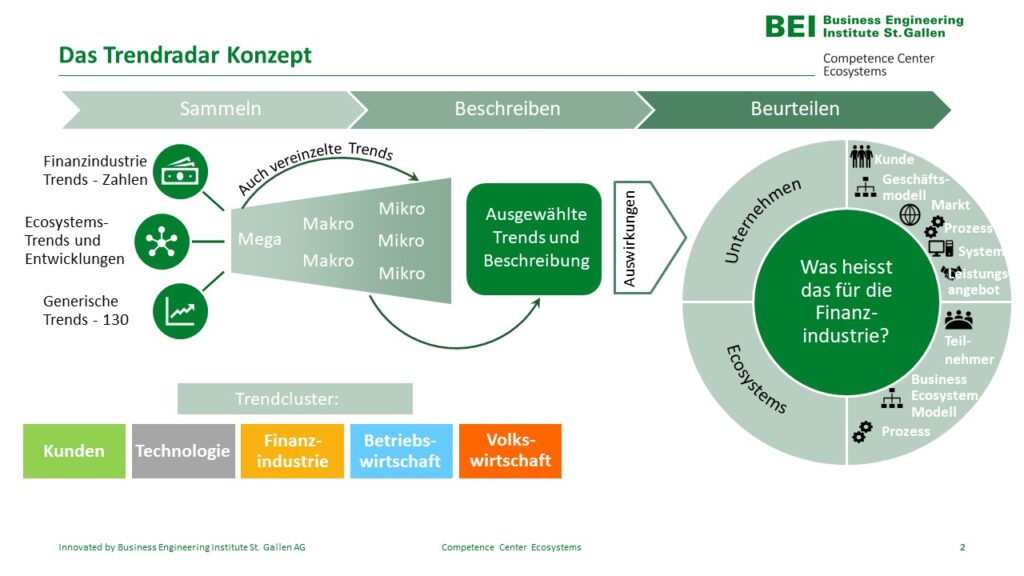

CC Ecosystems Trend Radar

One of our ongoing projects is our Trend Radar, in which we identify the trends relevant to the financial industry in the categories customers, technologies, financial industry, business administration and economics and analyze their impact at the enterprise and ecosystem levels (Figures 1 & 2).

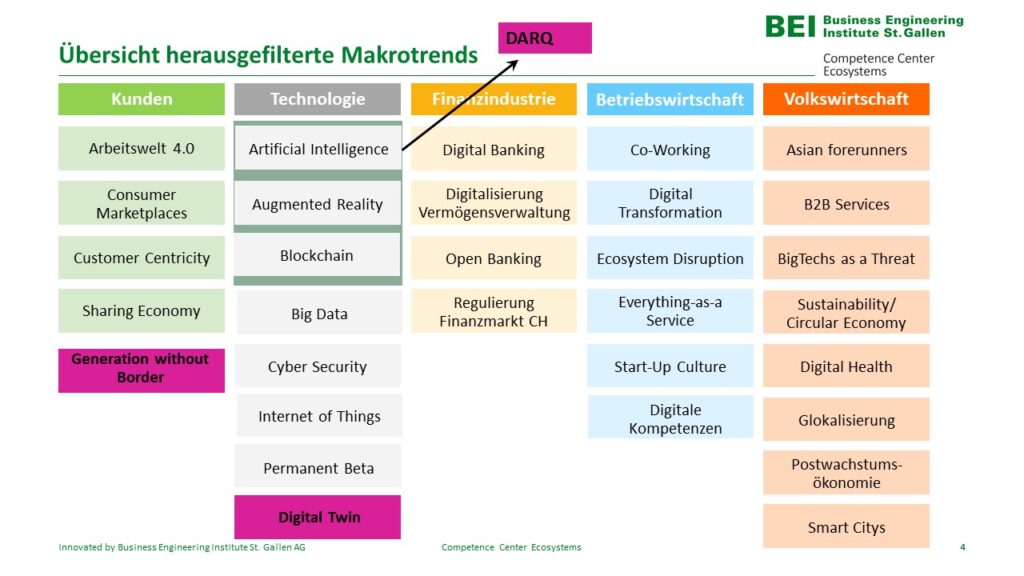

In this article, we present the impact of the pandemic on a number of the macro trends shown in Figure 2.

Working Environment 4.0, Digital Skills & Cybersecurity

In the spring, about three quarters of the companies in Germany and two thirds of the companies in Switzerland relied their employees’ working from home to cope with the coronavirus crisis [2][3]. What was an initial experiment for many has led to many positive experiences among both managers and employees – and generally ensured that companies and employees who had no experience with digital collaboration models to date have built up the necessary skills. Now that this hurdle has been overcome, home office should become a real alternative for many employees – at least part-time. In addition, flexible workplace models can also save real estate costs, a factor not to be sneezed at in the current economic climate. Apart from that, the pandemic is of course not yet over and as long as there is no vaccine available, working from home will continue to be an important addition to the time spent in the company from an epidemiological point of view [4]. The only work-related trend that has suffered a drop in demand as a result of the crisis is co-working, which has been avoided, just like working at the company, in order to reduce the likelihood of contracting SARS-CoV-2.

Another group that has gained digital skills in addition to employers and employees in the wake of the pandemic are consumers who had to switch to digital channels for shopping due to weeks of store closures. This general increase in the use of digital channels, both at work and at home, is also giving a sustained boost to the issue of cybersecurity, as the data of companies, employees and private individuals must be safeguarded, whether we are talking about external access to company networks, applying for the so-called “corona assistance” or protecting privacy when using video chat services.

Artificial Intelligence, Blockchain, IoT & Big Data

However, the pandemic has not only strengthened digital skills, but has also advanced the use or development of some technologies. In particular, the focus was on tracking the infection with SARS-CoV-2 using IoT (e.g. coronavirus tracing apps), Big Data and blockchain. However, a great deal of attention was also paid to predictive analytics, using artificial intelligence to make predictions about the further spread of the pandemic. In addition, IoT and AI have been used to fully automate certain activities in order to minimize the risk of infection. Such efforts range from the sterilization of objects in hospitals by robots to the transport of medical samples and quarantine material by drones[5].

Macro Economy & Sharing Economy

Regarding the keyword ecosystems, two opposing developments can be observed. On the one hand, local networks were strengthened, e.g. in the form of shopping aids for older people, and on the other hand, globally operating ecosystems, such as Amazon or Facebook, experienced a very successful first half of 2020 overall (outliers in the development can only be observed among companies that focus very strongly on the “real” world, such as Airbnb, which suffered a drop in sales of around 70% in the second quarter compared to the second quarter of the previous year).

The successful development of globally operating ecosystems is due to the state of digitalization within these ecosystems, with which local companies are currently unable to keep up. This strengthening of global structures is, however, limited to such ecosystems: the pandemic has put a decisive damper on the globalization of production by creating supply bottlenecks. As a result, more than half of all German companies with cross-border operations are considering replacing offshoring at least with nearshoring [6]. European economies also need to think about their competitiveness beyond this, because the Asian frontrunners have handled crisis management (e.g. Taiwan, South Korea, Singapore etc.) better than the USA, England and other European countries. As a result, they had fewer coronavirus cases to mourn and were able to move to the “new normality” earlier. This in turn has had a positive effect on economic recovery. A culture war has already been predicted between the centrally controlled Asian countries and the enlightened individualism of Western countries.[7]

Since the economic slump, however, people have been thinking in completely different directions at the same time, keyword “post-growth economy”. Because if we expect further pandemics in the future, or even just further lockdowns until the end of this pandemic, we will inevitably have to think about how a company or an economy can function even without growth. A decisive contribution to this could be made by the Sharing Economy, the sharing of objects or spaces. However, it is precisely this that has been weakened by social distancing, albeit probably only for the foreseeable future. The focus on activities in the area and therefore also on one’s own (Smart) City and the need for information on local developments (e.g. shopping aids for older people) have increased[8].

Effects of the macro trends on the financial industry

Customer

During the pandemic, all customers were forced to do without branch services to a considerable extent. For example, ZKB closed more than 50 branches, while only 13 were open continuously. At UBS, CS and Raiffeisen, one third of the branches closed. So for better or worse, customers had to contact their bank via digital channels. On the one hand, this is an opportunity for the banks to expand digital channels and downsize their branch system. On the other hand, this naturally also increases customer demands on their bank’s user interface. Asset preservation, which had previously been the focus of greater attention due to the low interest rate environment, is now playing an even bigger role than before due to the stock market slump, as the need for protection is increasing. With regard to the origin of customers, the trend towards regionalization could be actively pursued further, especially by cantonal and Raiffeisen banks.

Business model

The topic of post-growth economics questions the profit motive of companies in general and places greater emphasis on the social benefits of value creation. This should differentiate banks that base their value proposition on serving society, an area in which cantonal or cooperative banks have a clear advantage. But commercial banks can also take this trend into account in their strategy, for example by offering sustainable investment opportunities. The revenue model shows that the demand for unpaid digital services continues to grow. On the cost side, savings can be achieved by downsizing branch systems, reducing office space and cutting down on business travel. Large companies such as UBS, Swiss RE or Zürich Versicherung have been working on the workplace of the future for years, and this has been further accelerated by the pandemic.

Market

The intensity of competition in the Swiss banking industry will depend on when the expected industry consolidation in the tourism industry, the events industry or the gastronomy sector will occur, to name just a few examples. The resulting credit defaults will in any case have an impact on bank balance sheets, the only question is: how strong will it be? Currently, the “corona loans” granted in Germany and Switzerland seem to have tended to ease the strain on bank balance sheets. However, the first globally active banks are showing signs of a slump – at HSBC, for example, in the form of a 65% drop in profits in the first half of 2020[9]. With regard to sales orientation, there will probably be shifts in the attractiveness of individual regions (USA vs. Asia), the same applies to investment areas (e.g. downsizing at shipping companies, cruise operators).

Process

As a consequence of the increased emphasis on cashless payments, the ideally completely digital processing of “corona loans”, and the closure of many branches in general, the automation and digitalization of processes has inevitably been strengthened. With regard to the depth of value creation, internationally operating banks will probably review the issue of outsourcing.

Come to stay

The pandemic has given an enormous boost to digitalization in the financial industry, and many of the observable developments will be permanent. In this respect, the coronavirus pandemic is also a transformation driver for the financial industry at the strategy and process levels. Only at the system level is there no impact to be observed. Although some interesting DLT and AI cases have been initiated or implemented worldwide, this has been more the case in the healthcare sector with a focus on the analysis or prognosis of the pandemic, not in the financial industry.

[1] https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020

[2] Litsche, S., S. Sauer, S. und K. Wohlrabe (2020), »Konjunkturumfragen im Fokus: Coronakrise trifft deutsche Wirtschaft mit voller Wucht«, ifo Schnelldienst 73(5), 57–61

[3] https://www.netzwoche.ch/news/2020-04-22/homeoffice-ist-gekommen-um-zu-bleiben

[4] https://www.netzwoche.ch/news/2020-04-22/homeoffice-ist-gekommen-um-zu-bleiben

[5] https://www.terra-drone.net/global/2020/02/07/terra-drones-business-partner-antwork-helps-fighting-corona-virus-with-drones/

[6] https://www.nzz.ch/wirtschaft/corona-krise-deutsche-unternehmen-passen-lieferketten-an-ld.1565362?reduced=true; https://www.stahl-online.de/index.php/neuausrichtung-der-lieferketten/

[7] https://www.bertelsmann-stiftung.de/fileadmin/files/Projekte/84_Salzburger_Trilog/Salzburger_Trilog_2006-Diskussionspapier_dt.pdf

[8] At https://www.bei-sg.ch/cc-smart-citizen you will find information about our competence center “Smart Citizen”.

[9] https://www.finanzen.net/nachricht/aktien/corona-krise-schlaegt-bei-britischer-bank-hsbc-ins-kontor-9149150