The way out of the digitalization trap

Digitalization is necessary, but its costs are often not offset by corresponding additional revenues. Ecosystems can provide a solution.

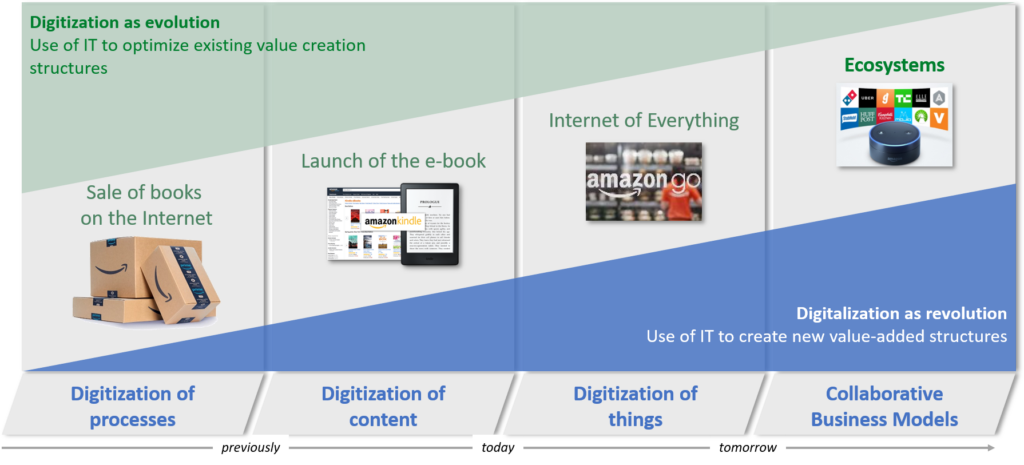

Innovations and changes in today’s world are due in part to digitalization. Every organization is in some way confronted with technological progress and tries to drive innovation by means of modern technologies, be it in the form of process optimization (incremental) or new business models (radical) (Beck, Lopes-Bento and Schenker-Wicki 2016). Digitization, i.e. the digital representation of physical objects, events or analog media, is the starting point for technological innovation. Technological innovations lead to lower marginal and transaction costs. As a result, more efficient ways of providing services can be used. At the same time, new competitors appear on the market and customer needs change. Amazon offers an example of how digitalization is changing the value-added structures and business models of companies (see Fig. 1). For example, Amazon first digitized book sales and then content (in the form of eBooks). Afterwards, information technology was used to create new value-added structures in the form of collaborative business models (e.g., entrepreneur loans for merchants on Amazon). With the advent of the Internet of Things (IoT), Amazon, along with other big players such as Google, Apple and Microsoft, also entered the digital assistant business and launched the Alexa product or the Amazon Alexa Ecosystem. This ecosystem essentially consists of various Alexa devices that are capable of communicating with the Alexa cloud (Chung, Park and Lee 2017). Through the Alexa application, the Amazon Echo device can be controlled by voice. The best-known functions fall into the category of the smart home (e.g. voice-controlled handling of light, temperature and car doors via application) and flash briefing (i.e. question-answer system; users receive information in summarized form via application) (Orr and Sanchez 2018).

Amazon is just one of many examples that show what changes digitalization can bring about. This development – from analog to digital – is also noticeable in the financial industry. Banks and insurance companies are facing a multitude of challenges. On the one hand, these are increased customer requirements (e.g. integrated services) and the pressure on margins, which results from the continuing low interest rate phase and regulatory requirements, among other things. On the other hand, there are other challenges, such as the high competitive pressure within the industry and the need to respond to changing market conditions. New competitors for the financial industry include BigTech (Amazon, Apple, Google, Microsoft) and FinTech (innovative financial service providers with technological innovations). At the end of 2019, for example, the British FinTech start-up Revolut was able to count 250,000 Swiss among its customers (Heim 2019). This is still low compared to the classic universal banks, but they are increasingly gaining customers. This is because Revolut offers inexpensive services that are also highly convenient (ZHAW 2019). The new competitors are not competing with the overall offering of the classic providers from the financial industry, but are specifically selecting individual offers. In the case of the British neo-bank Revolut, it is the prepaid credit card. This leads to a break-up of the value chain of the traditional providers. The question therefore arises: How can the financial industry react to this?

Digitalization seems to be the obvious solution to all problems, but appearances are deceptive. Customer interfaces and processes can be optimized with new technologies, which improves the customer experience. But such digitization efforts cause higher costs, which in the best case can be associated with a reduction of process costs. In some cases, there is also the opportunity to tap into new customer groups. For example, the Swiss cantonal banks have the opportunity to win customers beyond the cantonal borders through online comparison portals and online offers. However, there is the dilemma that the digitalization costs of companies often cannot be compensated by correspondingly higher sales or cost savings on the other side. Customers appreciate improved services, but are seldom or hardly willing to finance them. So how can we deal with this digitalization trap? One interesting approach is to have companies participate (or offer their services) in different business ecosystems. This is because the constant change in customer needs, but also the rapid development of technologies, requires new forms of collaboration, also for the financial industry. Customers no longer ask for individual products or services, but want integrated problem solutions. In this context, the development of technology usage by customers should also be mentioned. More and more people are becoming more technology-aware – the smartphone is their daily companion – as a result of which their needs are also changing, and they are accordingly demanding smarter products and services. Therefore it is obvious to consider IoT as a possible technology concept: Connecting the physical object (smartphone) with virtual services (e.g. financial services) can lead to more targeted customer addressing and satisfaction of new customer needs. This requires, however, that different actors, mostly spanning different industries and disciplines, jointly develop a service offering. Involvement in business ecosystems can generate various benefits for financial service providers, such as new forms of revenue generation, possibly a stronger customer focus and retention, the involvement of specialized partners, and the sharing of risks and associated costs.

In the following articles you will learn exactly what business ecosystems are, what opportunities they open up for financial service providers and how to design an ecosystem strategy:

In English:

- Structuring Ecosystems – An Applied Example

- Strategy in an Age of Increasing Interconnectedness – Taking Stock

- Open Banking White Paper – The Future of Collaboration in Corporate Banking

In German:

- Ecosystems – Positionierungsmöglichkeiten für die Finanzindustrie

- Ecosysteme von A(nalyse) bis P(ositionierung)

- Ecosysteme des Ostens – Was wir von WeChat lernen können

- Banking im Ökosystem wird zur neuen Normalität

- Strategie im Zeitalter zunehmender Vernetzung – Eine Bestandsaufnahme

- Ecosystemradar des CC Ecosystems – aktuelle Entwicklungen und Trends

- Innovative Technologien fördern die Entwicklung von Ecosystemen

- Governance im Ecosystem

- Open Banking: Eine elementare Grundlage für offene Geschäftsmodelle und Ecosysteme

- Open Banking: Chance für die Schweiz, wenn wir die Kräfte bündeln

- Koevolutionäre Perspektiven – Was wir aus der Natur über Organisationsansätze lernen können