The Robo-Advisor – A Substitute for the Human Investment Advisor?

Online asset management has been experiencing a rapid rise in Germany for several years. Since 2017, the number of users has grown by a factor of 7 from around 291,000 in 2017 to around 2.01 million in 2020 (cf. Statista 2020), while the investment volume has increased more than tenfold from around 756 million euros to 8.068 billion euros (cf. Statista 2020). Two factors in particular are key to this trend: firstly, the loss of trust in personal banking advisory services caused by the financial crisis in 2007, and secondly, the increasing demand for digital offerings by digital natives. The new generation of customers who have grown up with smartphones and tablets, also known as “Generation Y,” is much more attuned to electronic communication, which means that personal contact such as with customer advisors at banks is losing relevance (cf. Alt/Puschmann 2016, 29). In the course of the shift from a personal, individual customer experience at a bank to the desire for standardized and digitized processes, “robo-advisors”, which replace personal, human advice with the offer of algorithm-based investment proposals, are becoming increasingly important (cf. Dapp 2016, 1).

For this reason, in this series of articles, I would like to provide an overview of what a robo-advisor is, what business models and strategies robo-advisors are pursuing, and how the traditional customer advisory process is changing through the use of robo-advisors. The articles are based on my bachelor thesis “An Analysis of the Impact of Robo-Advisors on the Customer Advisory Process in the Investment Sector”, which I wrote at the Information Systems Institute of the Faculty of Economics at Leipzig University.

In my last post, I explained what characteristics distinguish the robo-advisory process from that of traditional client advice provided by a human advisor. Today, I explain how exactly these characteristics affect the traditional client advisory process and change it to create the robo-advisory process that I presented in the third post of this series. Finally, I answer the question of which of the two advisory processes is the better one.

Impact of Robo-Advisors on the Traditional Client Advisory Process

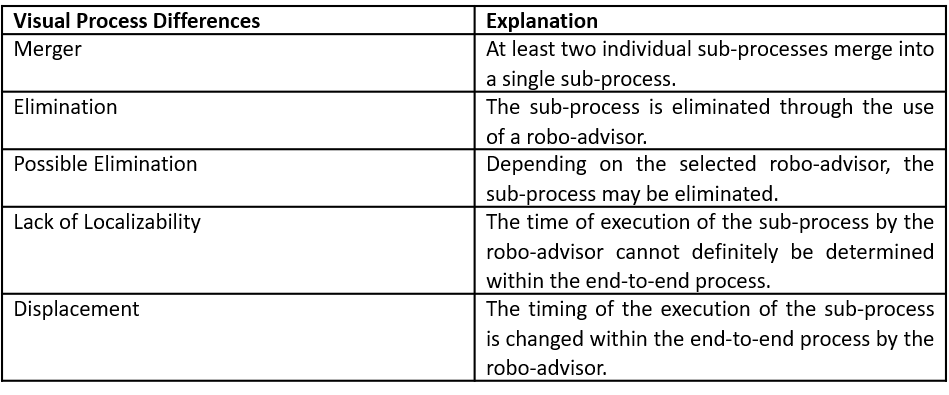

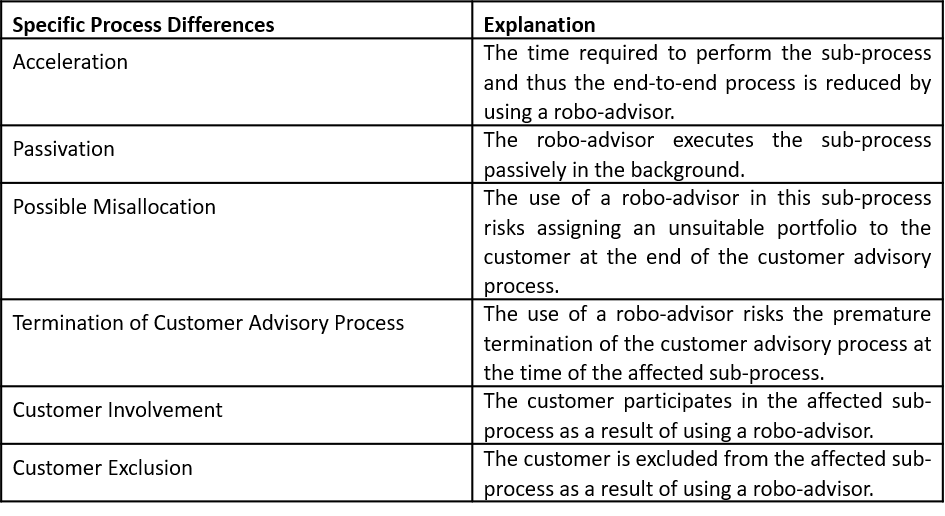

The aim of this series of articles is to explain how and why robo-advisors influence the process of traditional customer advice and whether this improves or deteriorates the advisory process. To this end, I have investigated how the process characteristics presented in the fourth article, which are characteristic of a robo-advisor, affect the traditional customer advisory process. I then divided the identified influences into the categories “visual” (can be visualized using the traditional customer advisory process) and “specific” (cannot be visualized). The five manifestations that can be visualized are Merger, Elimination, Possible Elimination, Lack of Localizability, and the Displacement of a Sub-Process. The specific influence can be subdivided into the following six characteristics: Acceleration, Passivation, Possible Misallocation, Termination of Customer Advisory Process, Customer Involvement, and Customer Exclusion.

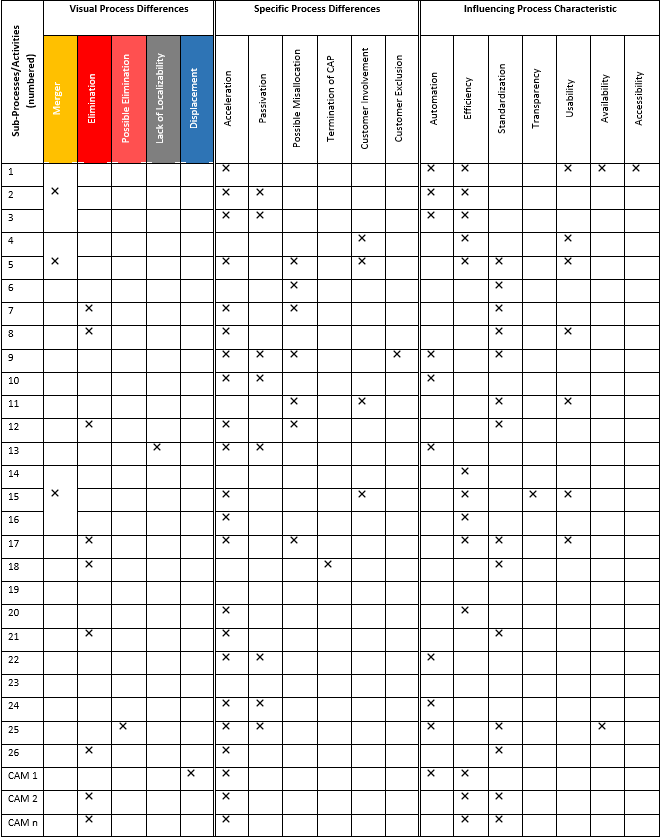

This matrix summarizes the extent to which the robo-advisor influences the traditional investment advisory process, which sub-processes are affected by it, and the process characteristics of a robo-advisor which the effect can be attributed to:

For better orientation, the identified visual influences were highlighted with colors in Table 4 and Figure 3. As can be seen from the matrix, all seven process characteristics derived from the literature lead to a change in the advisory process. Only two of the sub-processes remain the same.

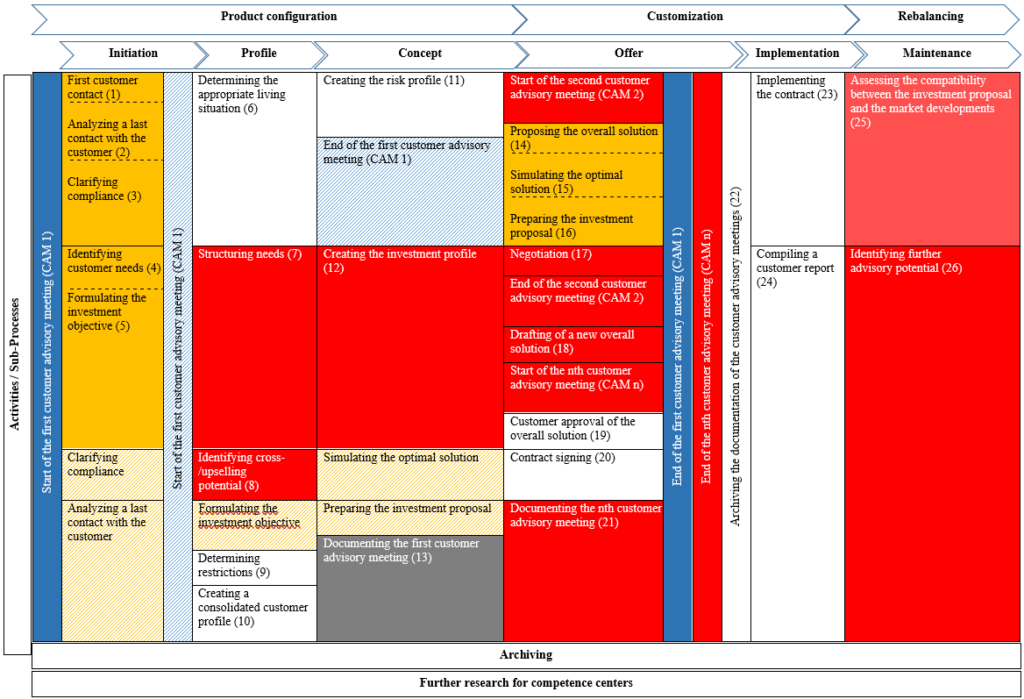

An example of the displacement of a sub-process is the first customer advisory meeting, which in traditional investment advice is not initiated until the beginning of the second process phase Profile. With a robo-advisor, almost the entire process takes place within a single “advisory meeting” that begins directly at the start of the first process phase Initiation and ends only at the conclusion of the process phase Offer. An example of the Lack of Localizability of a sub-process is documenting the first customer advisory meeting (13), as a robo-advisor directly captures a customer’s details. Depending on the chosen management strategy, it is also possible that the use of a robo-advisor eliminates the need of assessing the compatibility between the investment proposal and the market development (25). Thus, this sub-process would be an example of the Elimination of a sub-process in the case of an actively managed robo-advisor, while the process would remain the same in the case of a passively managed robo-advisor.

In contrast to the visual influence, where a sub-process can have a maximum of one characteristic, one and the same sub-process can have several specific characteristics. This means that the process can, for example, be simultaneously accelerated, newly executed in the background and lead to a Possible Misallocation. Eight of the total 29 sub-processes are passivated through the use of a robo-advisor, which means that the respective actions are automatically executed in the background and have no active component. In 15 percent of all sub-processes, a robo-advisor reinforces a possible misallocation of the customer portfolio. Thus, these seven sub-processes pose the risk that a robo-advisor will recommend an unsuitable product to the customer at the end of the entire advisory process. Under this scenario and if the customer is aware of the misallocation, the robo-advisory process must be terminated at the time when a new overall solution (18) is drafted in the traditional advisory process, since the robo-advisor is also unable to offer the customer an alternative investment proposal due to Standardization. Due to the fact that with a robo-advisor the determination of restrictions (9) regarding an investment is carried out automatically in the background, this sub-process is accelerated and, in contrast to the traditional advisory process, the customer is excluded from active participation. On the other hand, customers are more involved in four other sub-processes, since there is no preparation for a customer advisory meeting at all and the investment proposal, including the simulation of the optimum solution (15), is presented to the customer. In addition, it is possible to a certain extent to determine the risk of the portfolio independently. Only seven percent or three of all sub-processes do not exhibit any specific influence.

Conclusion

The analysis revealed that the robo-advisory process differs from the traditional investment advisory process in 27 out of 29 sub-processes. Robo-advisors eliminate or merge 20 out of 29 sub-processes, mainly as a result of Standardization or Efficiency, while the acceleration of the end-to-end process, which affects almost half of all sub-processes, is the most significant specific difference between traditional investment advice and a robo-advisor. The process is accelerated largely by the Elimination or Passivation of the respective sub-process.

Whether a robo-advisor is better or worse than the traditional investment advisor cannot be answered unequivocally. On the one hand, the traditional client advisory process can be sped up in quantitative terms by eliminating and merging sub-processes, among other things. The fact that activities are carried out automatically in the background and only a single consultation is required with a robo-advisor also shortens the advisory process. The high Usability of robo-advisors also leads to greater involvement of the customer in the advisory process. On the other hand, the Elimination of a sub-process can also have a negative impact in terms of quality. For example, there is a risk that the customer will be presented with an unsuitable investment recommendation and that the advisory process will subsequently have to be discontinued. The cause of a Possible Misallocation is also primarily due to the standardized products and predefined answer options for the customer, as a result of which the consulting process loses a considerable amount of individuality. Another negative factor is the exclusion of the customer from a sub-process, which is only marginally caused by a robo-advisor.

In view of the results, we can conclude that the robo-advisory process, compared to the traditional customer advisory process in the investment area, is at this point merely an evolution in terms of time savings. In terms of the quality of the customer advisory process, there is clearly a regression compared to traditional investment advice.

Accordingly, robo-advisors cannot currently replace human advisors, but they can certainly supplement them. A solution is already emerging on the capital market in which humans and machines work together – a “hybrid advisor” that is intended to combine the advantages of both traditional and robotic investment advice (see Fisch et al. 2018, 22). Such a prototype is already being used by some asset managers.

It remains to be seen how the customer advisory process in the investment sector will evolve in the future. Robo-advisors, however, seem to be indispensable for this development.

Sources

| [Alt/Puschmann 2016] | Alt, R., Puschmann, T., Digitalisierung der Finanzindustrie, Springer-Verlag, Berlin, 2016. |

| [Dapp 2016] | Dapp, T.-F., Robo Advice, Deutsche Bank Research, 2016. |

| [Fisch et al. 2018] | Fisch, J.E., Labouré, M., Turner, J.A., The Emergence of the Robo-advisor, University of Pennsylvania Law School (Institute for Law and Economics)/Harvard University/Pension Policy Center, 2018. |

| [Nueesch et al. 2016] | Nueesch, R., Zerndt, T., Alt, R., Ferretti, R.G., Tablets Penetrate the Customer Advisory Process: A Case from a Swiss Private Bank, Business Engineering Institute St. Gallen AG/University of Leipzig/University of Lugano, 2016. |

| [Statista 2020] | Statista, Robo-Advisors, 2020, https://de.statista.com/outlook/337/137/robo-advisors/deutschland#market-revenue |

- The Robo-Advisor – A Substitute for the Human Investment Advisor? - 03.02.2021

- What Distinguishes a Robo-Advisor? - 22.01.2021

- Robo-Advisors vs. Traditional Customer Advisors - 08.01.2021