Target Models for a Digital Asset Offering in the Regulated Space

The topic of digital assets has finally reached the mainstream. Reports in various non-specialist media such as blick.ch[1] or the Neue Zürcher Zeitung[2] on the price performance of Bitcoin show that there is great interest in the topic and that a new asset class has established itself. The term digital assets generally covers all coins and tokens based on a blockchain. This includes not only cryptocurrencies, such as Bitcoin or Ethereum, but also other types of tokens, such as tokenized assets[3]. However, despite the great interest in these assets, it is difficult for potential investors to access digital assets compared to traditional financial products. Often, there is no choice but to open their own account on a crypto exchange or buy the digital assets through a specialized provider. Independent trading on crypto exchanges and private storage of the private key require a basic knowledge of digital assets, e.g. how a transaction is triggered on the blockchain, which on-chain services are available or how the private key for one’s own wallet is stored securely. In contrast, specialized providers, such as crypto brokers, often have barriers to entry in the form of a minimum investment. The potential for services that make it easier for customers to acquire digital assets is great, but so far only a few financial institutions offer such services. According to the banks, there are many reasons for the lack of a comprehensive offering, e.g. concerns about the value of digital assets, high scepticism regarding money laundering or a lack of know-how in the operational handling of the new asset class. This blog post addresses the last point and aims to show that there are various operational implementation options for a basic digital asset offering for regulated banks. The basic digital asset offering here is understood to be trading as well as custody of digital assets. Additional high margin products & services related to digital assets by a regulated bank will be discussed more fully in a future blog post. The different options should serve as a rough guideline for further discussions in the context of the digital asset offering at banks, e.g. for the verification of the desired operational risk or for the detailed design of the product & service offering.

What Are the Components of a Digital Asset Offering?

The value chain for digital assets consists of various specialized providers and can be compared to the value chain for securities trading at a bank today. It includes in particular:

- Crypto exchanges: Trading takes place via a specialized crypto exchange where the corresponding asset can be bought and sold against fiat currency, e.g. US dollars, euros or Swiss francs. The crypto exchange provides an order book and, depending on the order size, offers additional services, e.g. over-the-counter (OTC) trading. To trade on a crypto exchange, a stock of fiat money must first be transferred to an account with that exchange, which can then be used for trading. For this, the crypto exchange requires an account with a regulated bank, as it often does not have a banking license. Crypto exchanges usually offer not only trading, but also the custody of assets. However, customers do not get access to the private keys, as the exchange often keeps them itself for security reasons. Thus, each transaction must be initiated by the exchange; customers cannot independently dispose of their digital assets.

- Brokers: If trading is not to take place directly via an exchange, brokers offer a different access to digital assets. They trade on behalf of a client and often offer custody and settlement of digital assets themselves or in cooperation with partners. The advantages of brokers are that a provider can distribute an order across various crypto exchanges and tend to realize a better buy or sell price.

- Custody providers: Custody providers offer a wallet for the safekeeping of digital assets, which is publicly visible by means of a public key and protected by a private key[4]. The private key ensures that digital assets can be moved, while the public key is the public address of the wallet on the blockchain. Custody providers keep the private key safe for their customers and can provide other services in this context, such as checking the digital assets to ensure they comply with money laundering regulations. If the private key is lost, the digital assets can no longer be moved, resulting in the de facto loss of the entire digital assets. Custody providers therefore ensure the secure handling of the private key and thus access to the digital assets.

- Compliance software: A feature of the blockchain is that all transactions made on it are stored in a tamper-proof manner. Therefore, the origin of most blockchain-based assets can be digitally traced. This is particularly necessary in terms of compliance with money laundering laws. Assets are verified using software that enables an assessment of the risk associated with the specific asset.

- Trading software: The requirements of end customers for professional trading with digital assets are comparable to the requirements for trading securities, e.g. shares. Different order types should be possible, e.g. a limit order, and different functions should be available, e.g. that an order can be automatically split across different trading venues and thus achieve a better price.

- Service provider for price information: Due to the high number of trading venues and the comparably young blockchain industry, there are different prices for the same digital asset on different trading venues. To counteract this fragmentation and information inequality, more traditional information service providers are also offering prices for digital assets.

- Auditors: Due to the high degree of specialization of the individual participants, specialized auditors are essential. They check whether the respective regulatory requirements are met, whether the underlying technology is safe, and whether appropriate risk management is in place.

From the bank’s point of view, various questions need to be answered for the operational implementation of a digital assets offering: Do you build up the know-how in-house or do you buy in the relevant skills from external providers? Which part of the value chain do you want to control, which operational risk do you want to take? What should the earnings structure look like? In the following, three possible implementation scenarios for banks in Switzerland are described, which have different characteristics depending on risk, know-how and earnings structure. The purchase and custody of a digital asset serve as an example.

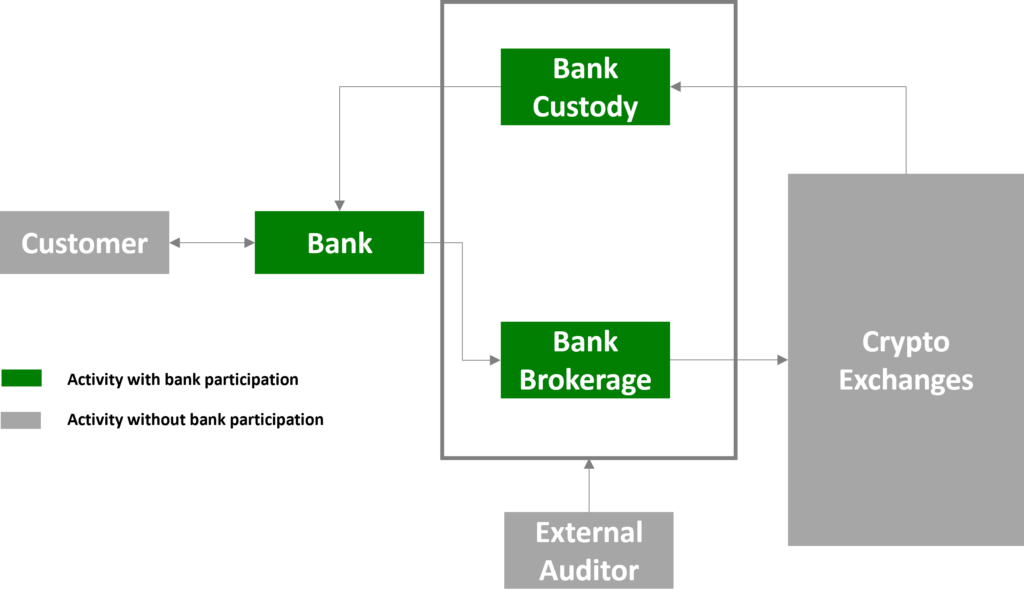

“Full Service Provider”

In the “full service provider” model, the bank trades directly on crypto exchanges on behalf of its customers, handles settlement and takes over custody. The most important advantage is the control over all activities as well as the complete value chain from a bank’s point of view in connection with the trading of digital assets and thus the freedom to design the offer, e.g. with regard to pricing or the offer of digital assets. The latter point in particular speaks in favour of this scenario, as the bank can independently initiate further business cases in the context of digital assets, e.g. on-chain services such as staking or lending with digital assets as collateral. In addition, the bank has the private keys and can thus control access.

With a view to future developments, the bank can position itself promisingly with in-house expertise (e.g. regarding the entire value chain and the handling of digital assets) as well as control over the custody of digital assets. This can come into play in particular if further blockchain-based digital assets are to be offered, e.g. tokenized assets. In order to be able to act as a full service provider, a larger budget is required in addition to very specific in-house expertise. In addition, the bank assumes a large part of the operational risk (e.g. the counterparty risk relating to crypto exchanges) and bears the loss in the event of a possible failure of a crypto exchange, for example. Part of the operational risk is reduced by keeping the digital assets in-house if the relevant know-how and skills are available. Since the know-how often has to be built up first, the implementation of the offer often takes longer than in the following two scenarios.

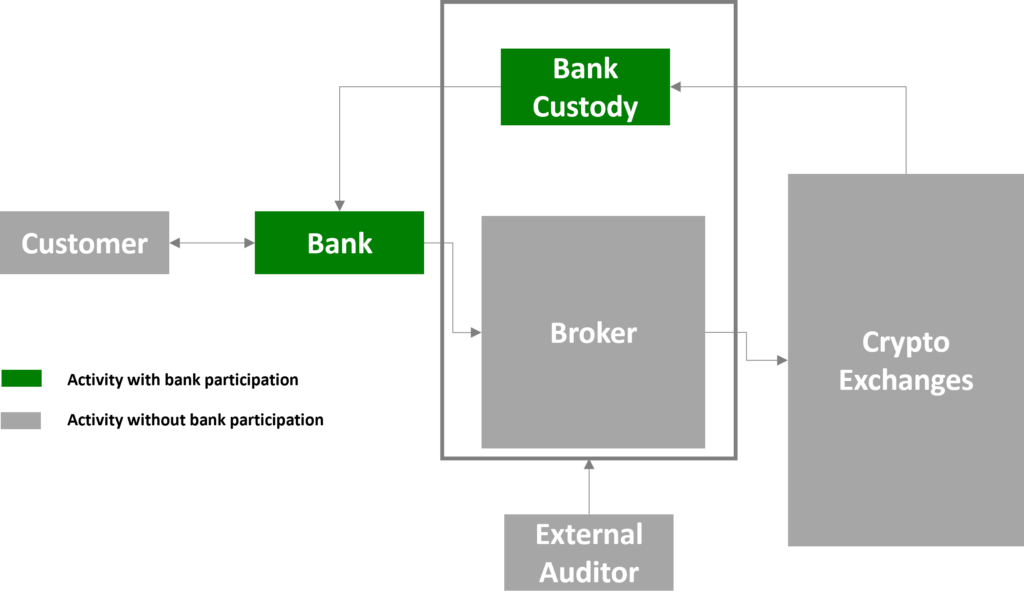

Bank as “Custody Provider”

Compared to the “full service provider”, the “custody provider” trades via brokers or liquidity providers and focuses on the custody of digital assets. Trading via brokers & liquidity providers has the advantage that various trading venues are indirectly accessible. The speed of implementation for a digital asset offering is higher compared to a “full service provider” as there is no need to open relationships with various crypto exchanges. In addition, the cost of capital for the bank can be reduced as the collateral required to obtain digital assets is reduced to one or more brokers. Another positive aspect is that the bank builds up know-how in the area of handling digital assets through independent custody.

By including brokers & liquidity providers, an intermediary is used, which on the one hand reduces complexity, but on the other hand can have a negative impact on pricing.

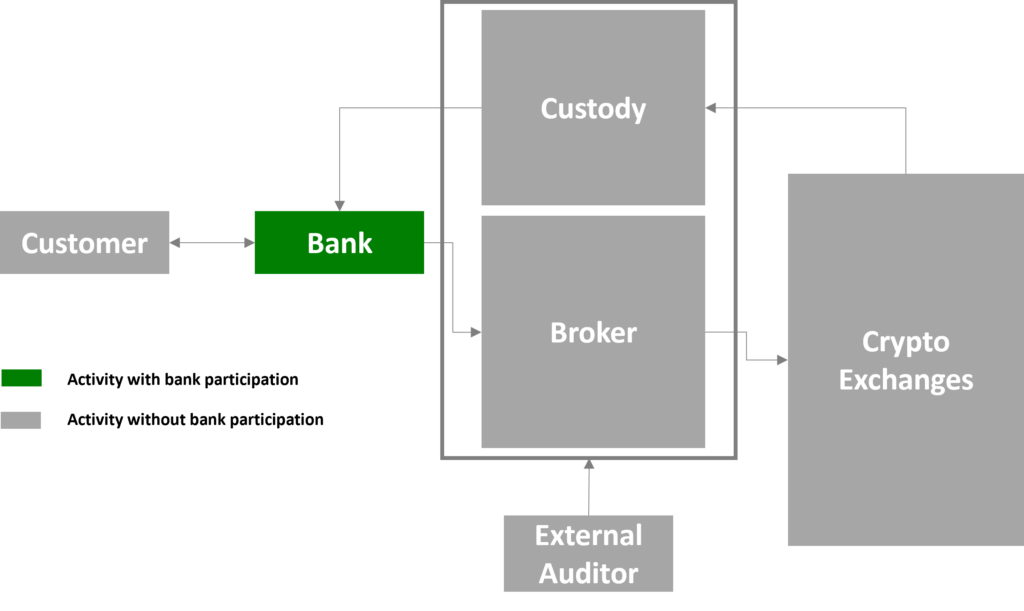

Bank as Intermediary for Digital Assets

In the third scenario, the bank ensures access to digital assets for its customers and specialist providers are used for operational settlement. This scenario has the highest implementation speed and offers the delegation of operational risks in connection with the settlement and custody of digital assets. Thus, specialized providers bear the risks that the bank would otherwise have to bear, e.g. the default risk of a crypto exchange or the handling of digital assets. The latter is particularly advantageous if the bank itself does not (yet) have the necessary technical know-how.

On the other hand, there are dependencies on third parties in the areas of know-how, access to digital assets and operational risk. On the one hand, these dependencies mean that the bank is dependent on third-party providers when it comes to creating its offering and thus cedes freedom of design, particularly in the areas of pricing and margin. On the other hand, the delegation of activities and the associated operational risk also entail a certain loss of control.

Outlook

Digital assets have already established themselves as an asset class and it can be assumed that demand will continue to rise. Existing regulations (Switzerland, Liechtenstein) or concrete regulatory intentions as well as their harmonization (EU with Markets in Crypto Assets, MiCA) benefit this process by providing banks with a legal orientation framework for digital assets. In addition, financial products such as the Bitcoin Future ETF are boosting investors’ price expectations. With the presented scenarios, a first discussion about implementations is possible, but further details need to be clarified, such as the mapping of digital assets in the core banking system, the reconciliation between the holdings in the core banking system and on the blockchain, and the implementation of specific regulatory requirements. Depending on the available expertise, the risk profile of the operational implementation or the desired design freedom, banks can already provide their customers with secure and scalable digital assets today.

[1] https://www.blick.ch/wirtschaft/ueber-66000-dollar-bitcoin-erreicht-neues-allzeithoch-id16922979.html

[2] https://www.nzz.ch/themen/bitcoin

[3] This blog post is primarily about cryptocurrencies; however, the broad principles of the scenarios outlined here can be applied to other types of digital assets as well.

[4] The public key can be thought of as an account number to which digital assets can be sent, while the private key acts as a password that can be used to access the corresponding “account” (the wallet) to perform transactions.

- Positioning opportunities for banks in the context of digital assets – A market observation - 13.02.2024

- Tokenization – Potentials, Challenges and Use Cases in the Environment of the Financial Industry – Part 2 - 06.06.2023

- Tokenization – Potentials, Challenges and Use Cases in the Financial Industry Environment - 14.02.2023