Strategic Positioning in the Insurtech Jungle

– Results of an Insurtech Analysis

Insurtechs are constantly making news in the financial world. Whether they are seen as the big competitor to insurers, exploiting the limping digitalization of the big players, or helping conventional insurers to arrive in the 21st century, startups are bringing a breath of fresh air to the industry through new technologies such as artificial intelligence (AI) or natural language processing (NLP). According to the Insurtech study by the New Players Network, around 130 new Insurtechs have been founded in the DACH region alone in the last five years and are still active today (New Players Network, 2021). Due to the abundance of new services and business models, it is appealing from both an entrepreneurial and scientific perspective to gain an overview of the structure and innovative capacity of the market.

As a subcategory of Fintechs, Insurtechs are subject to different structures and regulations. Taxonomies for Fintech business models cannot be applied to Insurtechs. It was recognized early on that there is a lack of structured valuation models for Insurtechs. This is primarily attributed to the lack of definition of characteristics and the lack of research into their impact on business models. As a result, the new approaches of the mostly fully digital business models are either not understood or misclassified.

Insurtechs as Disruptors of the Insurance Industry

A fundamental problem associated with the term “Insurtech” is the often divergent approaches to defining it. The term “Insurtech” is made up of the word “insure” and “technology”, in the same way as the term “FinTech”, and on the one hand refers to technology companies that specialize in services in the insurance industry. On the other hand, the services offered are also referred to as “Insurtechs”. As the Insurtech phenomenon becomes more widespread, it is becoming increasingly difficult to draw a line between the different business models. Current market observations suggest that startups (1) are no longer exclusively in the insurance industry, (2) are increasingly organized in ecosystems and perform different tasks within them, and that (3) the heterogeneity of business model approaches is increasing (New Players Network, 2021). In the course of the research, researchers also found that the analysis of Insurtech business models in Germany yields different results than in the U.S. or China. Depending on the region, market conditions or external influences, different archetypes can be identified regionally.

Linking Technology and Value Creation

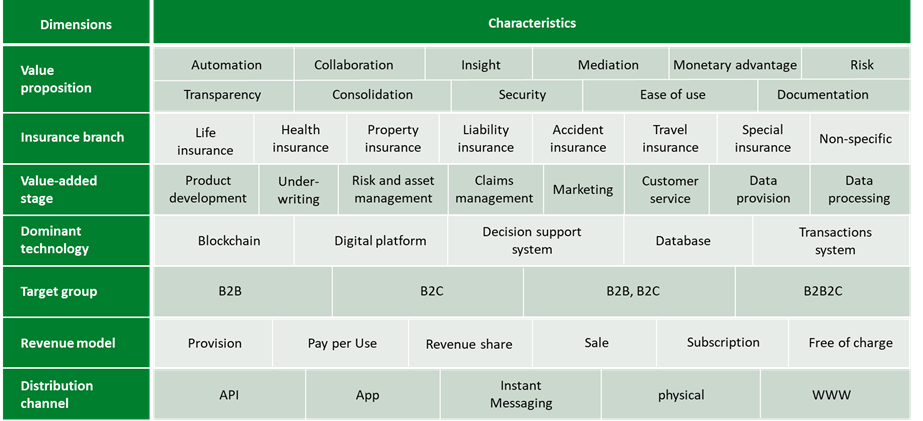

The classification of new business models is often based on technological factors. However, there is a risk here that the industry-specific value creation addressed by the start-ups is pushed into the background. In order to combine both the technological and the value-creating aspects, an overview will be created for Insurtech business models in the form of a taxonomy that combines the technological characteristics of the start-ups and the specific characteristics of the insurance industry. The taxonomy is then used to empirically derive Insurtech business model archetypes for different regions and markets. To achieve this objective, the first step was to draw on an existing FinTech taxonomy by Eickhoff et al. (2017), which was specified for Insurtechs in an iterative development process following Nickerson et al. (2013). For this purpose, 165 start-ups from the DACH region were examined in the first iteration, while the second iteration included 275 European Insurtechs. The resulting taxonomy consists of the seven dimensions insurance line, value creation stage, dominant technology, value proposition, sales channel, target group and revenue model (Figure 2).

Derivation of Insurtech Business Model Archetypes

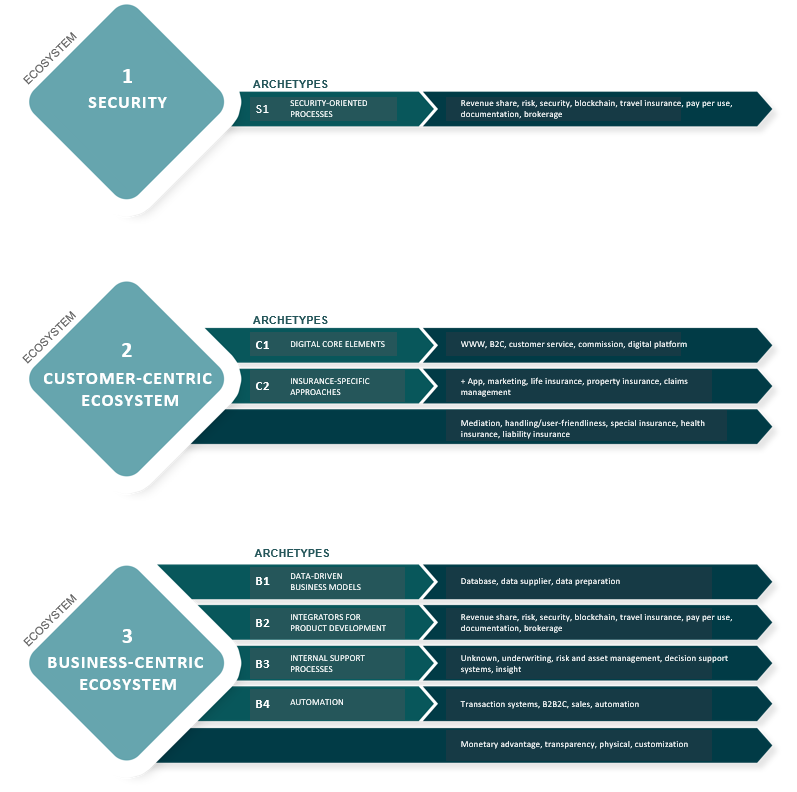

Furthermore, the Insurtech taxonomy was applied to analyze the 275 European Insurtechs in order to derive business model archetypes. The statistical cluster analysis yielded seven archetypes, which in turn could be assigned to three different ecosystem approaches, resulting in strategic fields of action for players in the insurance market. It can be seen that corporate networks are also pointing the way in the insurance industry and that the boundaries of the industry are becoming increasingly blurred. The three ecosystem approaches identified comprise Insurtech archetypes in the areas of “security”, “customer centricity” and “digital insurance processing” (Figure 3). Here, the different ecosystems build on each other. The digital security business models can be interpreted as a prerequisite for the customer-centric and the enterprise-centric business models, especially in the digitalized world.

(1) Digital Security

The digital security business models focus mainly on the prevention, averting and analysis of cyber risks. The cluster is more concerned with protecting operations, data and processes in the course of digitization than with general insurance protection. The associated business models evolved in the course of digitization, as more and more digital processes increased the risk of attacks along the way. The topic of cybersecurity moved more and more into the focus of the industry due to widespread attacks, as especially industries with highly sensitive data were affected by cyberattacks. Examples include the attacks on Yahoo, Adobe and J. P. Morgan (Süddeutsche Zeitung 2014, Handelsblatt 2014). In the insurance sector, the large amount of sensitive customer data created an enormous need for action and a niche that could be filled by Insurtechs such as Mailo, Cogitanda and Perseus. Mailo offers cyber insurance for freelancers, small business owners and the self-employed and specializes in the commercial sector. Cogitanda and Perseus have even focused their entire business model on the insurability and technical implementation of cyber risks and take care of data security before and after cyberattacks. The differentiation of the digital security ecosystem from the other ecosystem approaches is also evident, as the security of data and processes takes on an overriding role as a hygiene factor, so to speak, for conducting the insurance business. After all, the core of insurance is trust in providers, so all business models and value creation activities are affected by this aspect. However, the new risks are also giving rise to insurance policies against digital risks or, primarily, cyber risks, such as Allianz CyberSchutz or HDI’s cyber insurance.

(2) Customer Centricity

The second major ecosystem that has emerged focuses on customer centricity, mostly via digital platforms. This category combines many of the characteristics from the Insurtech taxonomy, which are directly or indirectly connected with the digital customer process. In order to describe these clearly, the archetypes C1 digital core elements and C2 insurance-specific approaches were derived. The elementary characteristics for business models in the customer-centric sector are explained in archetype C1 and summarize the basic common features of companies in relation to digital platforms and thus also relate to customer-centric ecosystems. In order to expand the core area, which describes customer-centric models regardless of the industry, additional characteristics are included in archetype C2. These relate specifically to the Insurtechs sector and to the insurance industry in general. This allows business models to be described that have more links to the insurance sector.

Two strategic orientations were observed in the insurance-specific approaches: On the one hand, Insurtechs position themselves with a small, specialized offering in order to secure an advantage (example: Fintiba with a focus on foreign students in Germany or Wetterheld with a focus on weather and event insurance). Such business models are advantageous in that they cover a niche market and can thus take an offensive role in the market. On the other hand, start-ups also seek their market positioning in the digitalization of already existing insurance areas in order to leverage efficiencies for the customer (Wagner, 2017). In addition to their solvency and security, insurance companies consider their established brand, existing service units and sales structures with established access to end customers as advantages in the market. Insurtechs, on the other hand, are characterized by high agility and consistent end-customer orientation in process and user experience design. Through cooperation, the different strengths can be combined, which have been painstakingly built up in a mutual competitive situation. In this way, the visibility and usability of the previously often bulky insurance products are improved for both the end customer and the insurer.

(3) Insurance Processing

The third ecosystem approach that emerged from the analysis comprises Insurtech archetypes that address insurance processing in a broader sense. In contrast to the customer-centric ecosystem, these companies tend to operate in a closed manner and are less interested in sharing and disclosing data. Processes tend to be closed and secrecy takes a high stance as a trade secret. This fear of disclosure on the part of established insurance companies forms a major obstacle on the path to digitization. However, this hurdle is increasingly being mitigated by the offerings of Insurtechs in the insurance processing ecosystem, which include startups of the archetypes (I1) data-driven business models, (I2) integrators, (I3) internal support processes, and (I4) automation. This section provides one example Insurtech per archetype:

- (I1) Data-driven business models: e.g. Claimsforce, which offers AI-based automated claims management in the composite sector.

- (I2) Integratoren: z. B. hat sich dieSDA SE auf eine Service-orientierte Architektur (Service Dominante Architecture – SDA) spezialisiert und will somit über ihre Plattform verschiedene Drittanbieter an Versicherungen anbinden.

- (I3) Interne Unterstützungsprozesse: z. B. unterstützt TrueMotion das Underwriting im KfZ-Bereich, indem Live-Prämien per Telematik aufgrund des Fahrverhaltens generiert werden.

- (I4) Automatisierung: z. B. automatisiert AvoCard die Rechnungseinreichung und Erstattung von Belegen.

Particularly due to the increased interface connection, insurtechs are succeeding in addressing individual parts of the internal value chain and in some cases even taking them over. For example, insurtechs such as Paladino are helping insurance companies to digitize individual processes such as underwriting or contract management and are thus also allowing external players to intervene in internal processes. This is leading to an increasingly interconnected market. A large number of the insurtech business models in the insurance processing ecosystem are necessarily focusing on a stronger exchange of players in the insurance market due to the services offered. Here, there is a close connection to the archetypes of the customer-centric ecosystem approach, as both approaches together map the complete value chain of the insurance industry.

Benefits

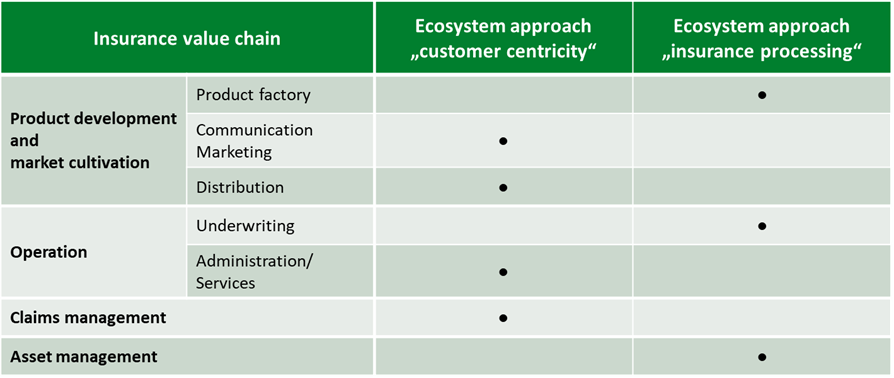

The three identified ecosystems and the seven insurtech archetypes provide orientation in the otherwise very heterogeneous insurtech market. This not only provides interested parties with simplified insight into the industry, but also lays a foundation for analyzing the market and generating new ideas. The concept of business model archetypes can also simplify market communication on the various business models and services. The results are relevant for established insurers as they can use the ecosystem approaches and insurtech archetypes to determine their positioning in the market, rank existing collaborations and identify new partners. Unlike the approach of classifying insurtechs as a holistic or even only technological phenomenon, the insurtech taxonomy enables the consideration of multiple dimensions. Thus, it also enables the classification of previously unknown business models in the context of insurers. In addition, the generated archetypes contribute to a better understanding of one’s own insurtech business model, as further potential extensions can be identified here by assigning the characteristics. For example, obvious opportunities and risks can be identified, which have been proven in other business models in the same cluster. Thus, a simpler market analysis becomes possible. The illustration of the parts of the value chain covered by the two ecosystem approaches of customer centricity and digital insurance processing offers an initial approach or inspiration for such analytical projects (Figure 4).

Future Research

There are several possibilities for future research, which can build on the insurtech business model taxonomy and the identified archetypes. Since mainly business models of start-ups were investigated, another approach would be to take a closer look at innovative services of established insurance companies and compare the results. Thus, further strategic positioning and cooperation approaches could be identified and evaluated. From a scientific perspective, it would also be interesting to develop further artifacts for analyzing adjacent sectors such as healthtechs, regtechs or proptechs in addition to the insurtech taxonomy that has been created. Thus, a detailed overview of innovative trends in the insurance and finance industry would emerge.

In addition, the three developed ecosystem approaches could be tested and further extended and the connections between the approaches could be analyzed. Since the taxonomy is suitable for conducting further studies, dimensions, characteristics or ecosystem approaches could be added to the insurtech taxonomy through continuous screening of insurtechs. Furthermore, it could be investigated which exact relationship certain dimensions have to the ecosystem approaches or how the dimensions are interconnected.

Conclusion

This summary of the research work around insurtech business models is intended to contribute to the understanding of the insurtech phenomenon and its implications. The findings have a high practical relevance, as insurtechs are a fundamental part of the insurance industry and thus also of the financial industry and the start-ups are changing both industries. Both the insurtech business model taxonomy and the insurtech archetypes serve as a knowledge base and foundation for insurtech research in business informatics and provide practitioners with a guide for analyzing innovative business models for positioning in the insurance industry. For example, they can help insurance company executives understand the often very confusing insurtech market and situate their own business model. Based on this, they can make well-founded decisions about the new or further development of their own services and about potential cooperations.

Sources

| Bruhn & Harwich (2017) | Bruhn M, Harwich K, 2017, Dienstleistungen 4. Konzepte – Methoden – Instrumente. Band 1. Forum Dienstleistungsmanagement, https://doi.org/10.1007/978-3-658-17550-4 |

| Eickhoff et al. (2017) | Eickhoff,M., MuntermannJ., Weinrich,T., 2017, What do FinTechs actually do? A Taxon-omy of FinTech Business Models https://www.researchgate.net/publication/320215812_What_do_FinTechs_actually_do_A_Taxonomy_of_FinTech_Business _Models |

| Handelsblatt (2014) | Handelsblatt, JP Morgan meldet Hackerangriff auf 83 Millionen Konten, https://www.handelsblatt.com/finanzen/banken-versicherungen/banken/us-grossbank-jp-morgan-meldet-hackerangriff -auf-83-millionen-konten/10790182.html?ticket=ST-5248278-xHAfEEsL1fc7TPaCtxSF-ap3 |

| New Players Network (2021) | New Players Network, 2021, Insurtech-Übersicht 2021, https://newplayersnetwork.jetzt/wp-content/uploads/2021/04 /INSURTECH_U%CC%88BERSICHT_2021.pdf |

| Nickerson et al. (2013) | Nickerson, Robert & Varshney, Upkar & Muntermann, Jan. (2013). A Method for Taxon-omy Development and its Aplication in Information Systems. European Journal of Infor-mation Systems. 22. 10.1057/ejis.2012.26. |

| Süddeutsche Zeitung (2014) | Süddeutsche Zeitung, 2014, FBI untersucht Cyberangriffe auf Banken https://www.sueddeutsche.de/wirtschaft/jp-morgan-fbi-untersucht-cyberangriffe-auf-banken-1.2106938 |

| Wagner (2017) | Prof. Dr. Wagner F , 2017, Gabler Versicherungslexikon, , ISBN 978-3-8349-4625-6 |