Robo-Advisors vs. Traditional Customer Advisors

Online asset management has been experiencing a rapid rise in Germany for several years. Since 2017, the number of users has grown by a factor of 7 from around 291,000 in 2017 to around 2.01 million in 2020 (cf. Statista 2020), while the investment volume has increased more than tenfold from around 756 million euros to 8.068 billion euros (cf. Statista 2020). Two factors in particular are key to this trend: firstly, the loss of trust in personal banking advisory services caused by the financial crisis in 2007, and secondly, the increasing demand for digital offerings by digital natives. The new generation of customers who have grown up with smartphones and tablets, also known as “Generation Y,” is much more attuned to electronic communication, which means that personal contact such as with customer advisors at banks is losing relevance (cf. Alt/Puschmann 2016, 29). In the course of the shift from a personal, individual customer experience at a bank to the desire for standardized and digitized processes, “robo-advisors”, which replace personal, human advice with the offer of algorithm-based investment proposals, are becoming increasingly important (cf. Dapp 2016, 1).

For this reason, in this series of articles, I would like to provide an overview of what a robo-advisor is, what business models and strategies robo-advisors are pursuing, and how the traditional customer advisory process is changing through the use of robo-advisors. The articles are based on my bachelor thesis “An Analysis of the Impact of Robo-Advisors on the Customer Advisory Process in the Investment Sector”, which I wrote at the Information Systems Institute of the Faculty of Economics at Leipzig University.

My last post before the Christmas break was about which business models and strategies a robo-advisor can align its offering with. Today, I will present the customer advisory processes of traditional, human banking advisory services and robo-advisors. In the rest of the series, I will then discuss the impact caused by robo-advisors which form of advisory is better and whether robo-advisors will be able to replace bank advisors in the near future.

Traditional Investment Advice Vs. Robo Advisory

Traditional Advisory Process

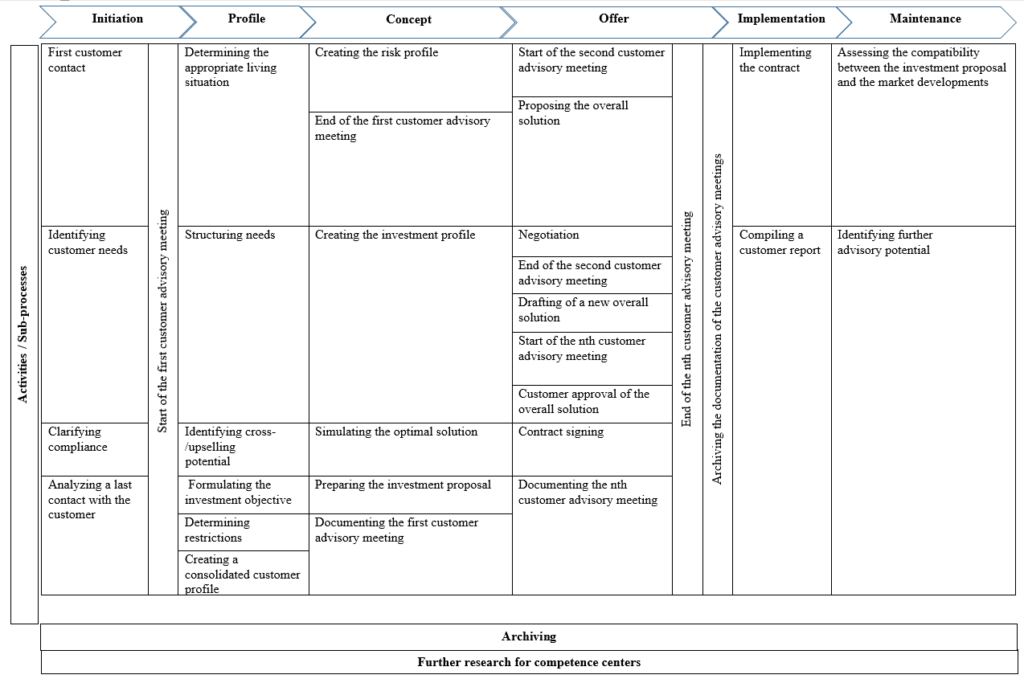

Figure 1 describes the traditional customer advisory process in the investment area, i.e., the process carried out by a human investment advisor. It encompasses all activities from the desire to invest on the part of the customer to the actual investment and maintenance of his portfolio by the advisor. All these activities can be divided into a total of six process phases: Initiation, Profile, Concept, Offer, Implementation and Maintenance. The following graphic describes the individual process phases and their associated activities from the perspective of the investment advisor[1].

At the beginning, during initiation, the customer gets in contact with the advisor before the actual consultation, during which the advisor records the customer’s master data and works out possible investment goals and wishes. If possible, the advisor analyzes a previous first customer contact. He or she then arranges and prepares for a personal meeting with the customer, taking into account compliance regulations. In the second process phase, the profile, there is a personal meeting with the customer. In this meeting, the advisor and the customer work out a final customer profile that takes into account the customer’s life situation, wishes, needs, and possible restrictions for an upcoming investment, as well as the goal of the investment. At the same time, the advisor identifies the best possible products and additional services with cross/upselling potential. In the subsequent process phase, the Concept, the advisor and customer create the risk profile in the last sub-process within the first advisory meeting, taking into account the customer’s life situation. Then, after the meeting, the advisor draws up an individual investment profile for the customer with the help of the risk profile obtained and simulates the solution with the most suitable financial products on the basis of a performance chart. After he/she has created the investment proposal, the advisor manually documents the previously completed client meeting. In the Offer phase, the advisor presents the elaborated overall solution to the customer in the second advisory meeting and negotiates it if necessary. Once a solution has been identified that the customer agrees to, the contract is signed. If needed, additional customer meetings must be scheduled for this purpose, with a new overall solution being worked out prior to each meeting. Manual documentation follows each customer meeting. After all meetings are completed, the advisor archives all documentation. In the Implementation phase, he/she purchases the securities on the capital market on the basis of the strategy contained in the solution discussed and prepares a customer report with all the relevant information about the person and the product developed. In the sixth and final phase of the process, Maintenance, the advisor continuously monitors the portfolio for price fluctuations and checks it for compatibility with the risk profile and investment objectives, so that – if necessary – the portfolio can be adjusted to achieve a higher market return. If the investor’s preferences change, the portfolio must also be adjusted. In the last sub-process of the end-to-end process, the client advisor strives to identify further potential for other advisory services (cf. Nueesch et al. 2016, 49f, Nueesch et al. 2014, 18f).

Robotic Investment Advice

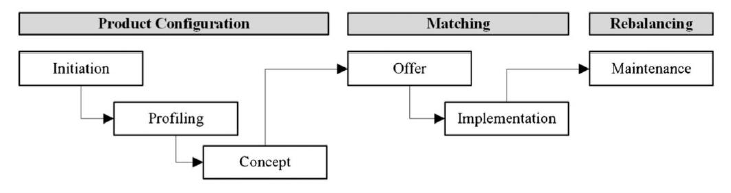

In contrast to the traditional advisory process, the literature summarizes robotic investment advice into three process phases, which, however, include all six phases of traditional investment advice. The first phase is Product configuration, which is a fusion of Initiation, Profile, and Concept (see Jung et al. 2017, 368). During product configuration, an attempt is made to reduce any information asymmetries between the provider and the customer in order to obtain as accurate a picture of the customer as possible and thus to be able to assign the best possible product solution to him/her. At the same time, the customer should be able to understand the process steps.

Depending on the robo-advisor, the customer is asked between five and 20 questions (cf. Hölscher/Nelde, 69). The aim of this procedure is to determine an investor profile. The questionnaire includes personal as well as financial questions, with the former determining the risk-bearing capacity and the latter the risk attitude. For risk-bearing capacity, the robo-advisor mainly asks about the following topics: age, occupation, monthly net income and freely available investment capital, assets and debt. For the risk attitude with the help of the financially relevant questions, the robo-advisor asks for an investment goal, such as financing studies or retirement, and the desired investment horizon in years. In addition, the customer is asked to assess his or her attitude to fluctuations in returns using a series of scenarios. Further criteria for determining the attitude to risk are the maximum loss the customer would accept before investing and his or her prior knowledge of financial products (see Wedlich 2018, 225, Petry 2017, 29). Depending on the customer’s answers, the robo-advisor determines an investor profile using a simple point system. The point value achieved is assigned to a defined investment strategy, including portfolio, which is recommended to the customer in matching (cf. Wedlich 2018, 225). This phase comprises the Offer and Implementation of the traditional advisory process. In the final third process phase, if necessary, Rebalancing takes place, which corresponds to Maintenance within traditional investment advice (cf. Jung et al. 2017, 368).

The advisory processes described in the literature are similar to each other, but they also display significant differences. In order to explain and evaluate these differences, next week I will conduct a more in-depth analysis of the characteristics of the robo-advisory process. So be sure to come back next week or register so you don’t miss a post.

[1] Since the process presented here takes the perspective of the investment advisor, it begins with the first customer contact. From the customer’s perspective, however, the process already begins with the desire to invest.

References

| [Alt/Puschmann 2016] | Alt, R., Puschmann, T., Digitalisierung der Finanzindustrie, Springer-Verlag, Berlin, 2016. |

| [Dapp 2016] | Dapp, T.-F., Robo Advice, Deutsche Bank Research, 2016. |

| [Hölscher/Nelde 2018] | Hölscher, R., Nelde, M., Darstellung, Funktion und Portfolioaufteilung von Robo-Advisory, in: Zeitschrift für das gesamte Kreditwesen (2018) 2, S. 68–73. |

| [Jung et al. 2017] | Jung, D., Dorner, V., Weinhardt, C., Pusmaz, H., Designing a robo-advisor for risk-averse, low-budget consumers, in: Electronic Markets, 28 (2017) 3, S. 367–380. |

| [Nueesch et al. 2014] | Nueesch, R., Puschmann, T., Alt, R., Realizing Value From Tablet-Supported Customer Advisory: Cases From the Banking Industry, University of St. Gallen/Business Engineering Institute St. Gallen AG/University of Leipzig, 2014. |

| [Nueesch et al. 2016] | Nueesch, R., Zerndt, T., Alt, R., Ferretti, R.G., Tablets Penetrate the Customer Advisory Process: A Case from a Swiss Private Bank, Business Engineering Institute St. Gallen AG/University of Leipzig/University of Lugano, 2016. |

| [Statista 2020] | Statista, Robo-Advisors, 2020. |

| [Wedlich 2018] | Wedlich, F., Wie wirken sich Verhaltensanomalien von Anlegern auf Robo-Advisory aus?, in: Corporate Finance (2018) 07-08, S. 225–229. |

- The Robo-Advisor – A Substitute for the Human Investment Advisor? - 03.02.2021

- What Distinguishes a Robo-Advisor? - 22.01.2021

- Robo-Advisors vs. Traditional Customer Advisors - 08.01.2021