PSD2 as an Enabler for Data-Driven, Intelligent Banking Services

The banking sector is currently undergoing major change processes due to increasing digitization and new technologies, changing customer needs, growing regulatory requirements and the entry of new market players. These developments challenge banks to further develop the customer interface in the digital age in order to offer a comprehensive and user-friendly digital banking experience. This also opens up the possibility for third-party providers such as fintechs to address individual parts of the value chain of banks and thus change the business models in the financial industry.

The Legally Mandated Disruption of Business Models

Breaking up the value chain in the financial industry has been explicitly promoted and demanded in all states of the European Union since January 13, 2018 by the Payment Services Directive II, or PSD2 for short. The new Payment Services Directive is a significant step towards a digital single European market and poses far-reaching challenges for the financial industry. Its objectives are (1) to increase the security of payment transactions, (2) to strengthen consumer protection and (3) to create a level playing field and allow two new innovative business activities: By regulating Account Information Services (AIS) and Payment Initiation Services (PIS) and requiring banks to provide the necessary interfaces for data exchange, banks’ control over customer transaction information is broken. This offers opportunities for third-party providers specializing in the analysis and marketing of account information to establish new services and business models.

The Role of Artificial Intelligence Among PSD2 Services

PSD2 gives AIS and PIS open access to customer account data and payment behavior via application programming interfaces (APIs). This creates potential for the use of AI technologies. However, when I started to look more closely into the topic, I found that the impact of PSD2 on the use of AI in the banking sector has not been studied so far; both topics have only ever been addressed separately. Therefore, in order to be able to assess how PSD2 affects the dissemination of AI in the banking sector, I investigated the business models and services of fintechs licensed to execute the PSD2 services Account Information and Payment Initiation in my master’s thesis “Analysis of Data-Driven Intelligent Banking Services Under the Influence of PSD II” under the supervision of Christian Dietzmann.

Market Analysis of European PSD2 Services

The basic authorization of commercial execution of the payment services AIS and PIS is granted by the competent supervisory authority. For this purpose, the European Banking Authority (EBA) has developed a register in which all licensed institutions are listed after being reported by the national supervisory authorities. The data basis for the market analysis described below is therefore 286 of the companies included in the EBA register that are licensed to execute PIS and/or AIS. The cut-off date for the survey is May 14, 2020. Based on the business models examined, I classified the services into the business areas of investments, loans and mortgages and payments. In addition, the area “connector” was added for the case that none of the business areas mentioned apply to certain services, such as software providers or account aggregation services. Subsequently, the services were analyzed for their AI maturity level as well as the type and range of AI functionalities used.

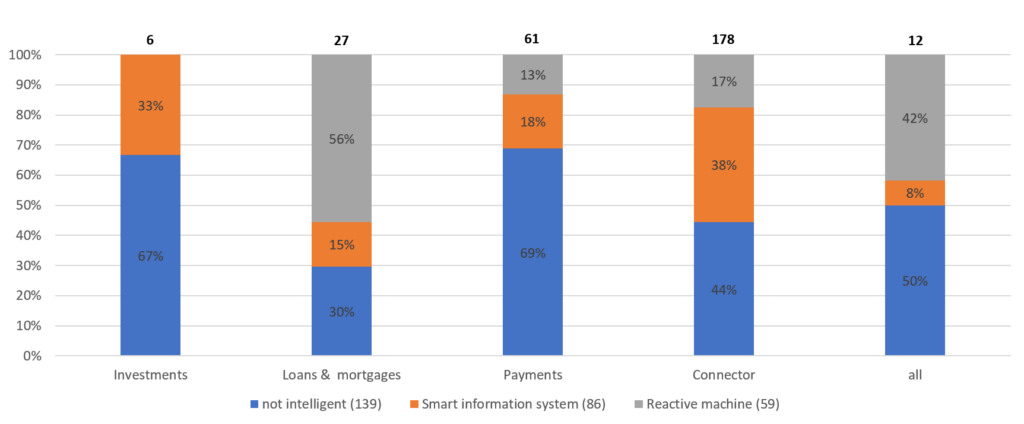

(1) Analysis of the Business Areas by AI Maturity Level

As the basis for examining the PSD2 services with regard to their AI maturity, I used the model by David Abele and Sara D’Onofrio, which classifies AI systems into the categories “smart information systems” and “reactive machines” according to their capabilities. “Smart” information systems or “intelligent” information systems refer to systems whose capabilities go somewhat beyond those of traditional IT. You are able to handle variable and poorly structured data as well as record incomplete inputs and draw conclusions based on them. However, they can only be used in limited, specific areas and do not have the ability to process complex situations. They are based on algorithms for which every possible action and process has already been predefined and are not able to generalize their capabilities or apply them to new areas because they cannot store memories/information.

Reactive machines, on the other hand, can respond immediately to input without being explicitly programmed for the input beforehand. Reactive machines are thus able to deal with complex or imprecise information or situations. They do not necessarily have to fully understand the information to generate an appropriate response. They can also consider historical information and past experience to a certain extent and plan ahead for future actions or strategies. The maturity level “not intelligent” was added to the model of Abele and D’Onofrio. All other AI maturity levels present in the model exist only in theory and were therefore not included in the analysis.

The analysis shows that the loans and mortgages and connector business areas have the largest percentage shares of intelligent services (see Figure 1). The connector business area represents a large proportion of PSD2 services with 178 services and includes aggregation services such as account aggregation, accounting software for businesses, and contract management apps. To enable these services, a number of AI systems of varying maturity are being deployed to analyze input and output structures and categorize and evaluate payments for customers. Smart information systems account for 38% of the connectors. If these evaluations also have forecasting functions, they are classified as reactive machines and account for 17% of connector services. The remaining 44% of services are not intelligent.

27 of the PSD2 services can be assigned to the loans and mortgages area. Although this figure is much lower than for the connector business area, the proportion of reactive machines is much higher at 56%. The reason for this is that this area primarily offers services in the area of automated financing decisions. The AI systems must be able to develop forecasts for the future solvency of borrowers based on historical data – this requires characteristics of a reactive machine. In addition, 15% of services in the loans and mortgages area are smart information systems, which typically involve the automated presentation of credit reports. The largest share of non-intelligent services is found in the areas of investments and payments, with 67% and 69% respectively. Currently, only smart information systems are found in the data set for the investments area; unlike in the payments area, no reactive machines have been observed to date (see Figure 1).

(2) Analysis of AI Functionalities

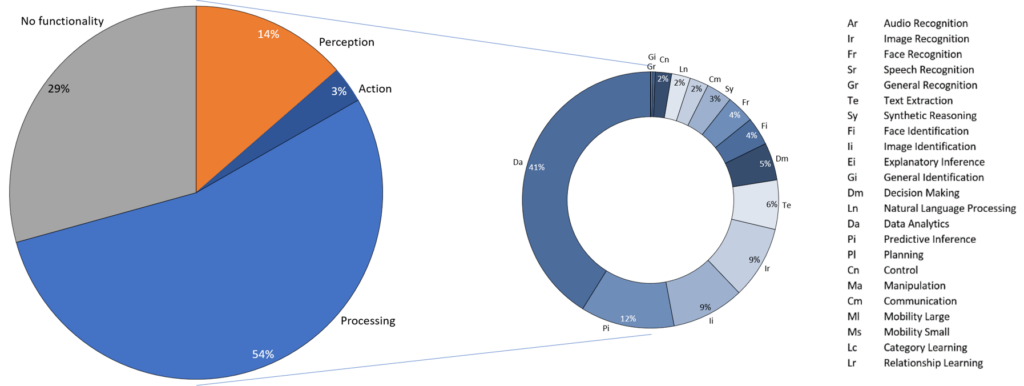

After assigning the AI maturity levels, I examined the functionalities of smart information systems and reactive machines in more detail using Dietzmann and Alt’s enhanced periodic table (version 2). The definition of the individual functionalities is based on the findings of the German digital association Bitkom e.V.

Across all services, the AI functionality Data Analytics (Da) is used most frequently and accounts for 41%, followed by Predictive Inference (Pi) at 12% and Image Recognition (Ir) and Image Identification (Ii) at 9% each.[2]

(3) Combined Analysis of Business Units and AI Functionalities

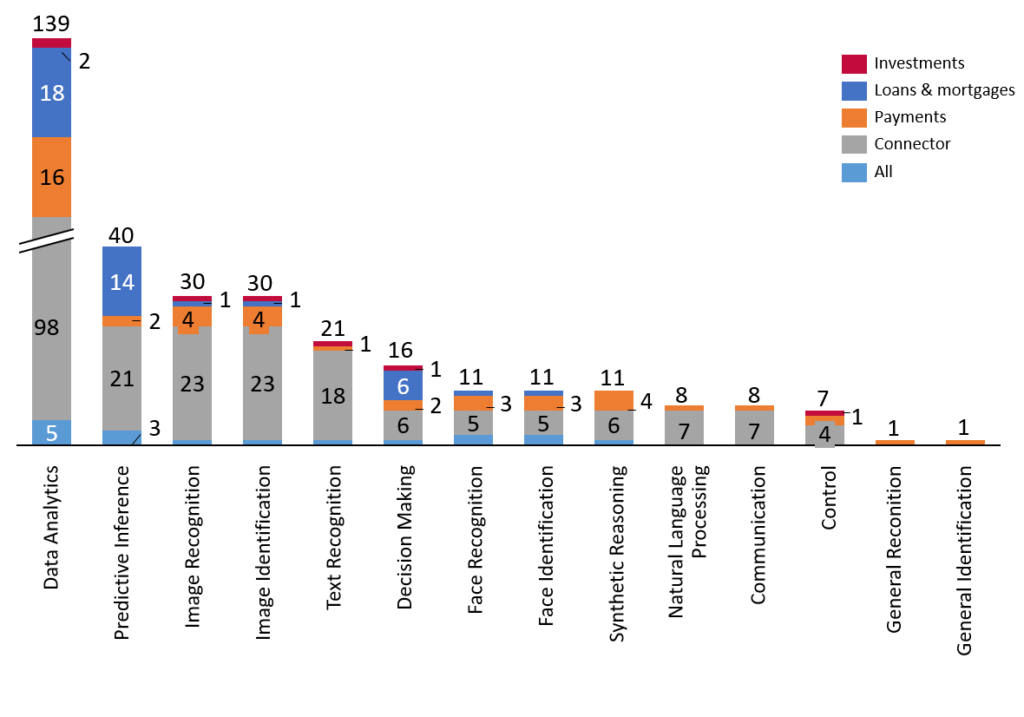

In the area of investments, only seven AI functionalities could be identified. These relate to two specific use cases:

- Investment software that uses facial recognition as authentication (Image Recognition; Image Identification) and automatically analyzes uploaded documents (Data Analytics; Text Extraction)

- An investment platform for credit portfolios, which invests partially automated according to certain criteria (Data Analytics; Decision Making; Control)

In the area of loans and mortgages, seven functionalities were identified, which are used within 19 services. The most frequently used functionality, Data Analytics (Da) (18 services), relates to the evaluation of financial data within the credit process. Predictive Intelligence (Pi) (14 services) is used to predict future solvency, and Decision Making (Dm) (6 services) is used in the final credit decision. In addition, the functionalities Image Recognition (Ir), Image Identification (Ii), Face Recognition (Fr) and Face Identification (Fi) are applied in one case each. These functionalities are used, for example, in a financing software for authentication by means of fingerprint recognition (Ir; Ii) or face recognition (Fr; Fi).The Payments domain comprises 19 services that use 14 of the AI functionalities listed in Figure 2. The range of functionalities used is thus highest in this area; however, if we count the concrete implementations of the functionalities across all services together, the use of artificial intelligence is similarly pronounced in the areas of payments and loans and mortgages (42 instances in the area of loans and mortgages, 45 in the area of payments). Of the 19 services, 16 use the Data Analytics (Da) functionality for various analytics tools within payments. Four applications use facial recognition (Fr; Fi) and fingerprint recognition (Ir; Ii) for authentication. Furthermore, there are four fraud detection applications in the field of payments. These use the Synthetic Reasoning (Sy) functionality to detect suspicious payments. One of the fraud detection applications also uses automated blocking of suspicious payments and thus uses the Data Analytics (Da), Synthetic Reasoning (Sy), Decision Making (Dm) and Control (Cn) functionalities. Another company offers payments using SMS. This works similar to a chatbot and makes use of the elements Data Analytics (Da), Text Extraction (Te), Communication (Cm) and Natural Language Processing (Ln). The functionalities General Recognition (Gr) and General Identification (Gi) are only applied in one case. In this case, software is used that triggers so-called “IoT payments”. This means that an automated payment process is triggered when an industrial machine is used.

In the connectors area, a total of 12 functionalities are applied in 98 services. Due to the larger number of services, the number of concrete functionality implementations grows to 223, but in relative terms this corresponds to the intensity of AI deployment in the areas of loans and mortgages and payments. The majority of services consist of the applications already mentioned in the form of analysis tools, authentication, document recognition and chatbots. In addition, there are applications in the area of risk management systems. Since these systems include functions based on historical data as well as future predictions, they belong to the group of reactive machines and use the functionalities Data Analytics (Da), Predictive Inference (Pi), Decision Making (Dm) and Synthetic Reasoning (Sy).

PSD2 as a Fertile Ground for Intelligent Banking Services

Since the introduction of PSD2 in 2018 and the associated regulation of AIS and PIS, many companies have already obtained authorization for these services. As of May 14, 2020, 286 companies hold a total of 2554 active authorizations in various European countries. The largest business area in terms of the number of AIS and/or PIS is the connector area. In the Financing business area, there are primarily AIS registrations. The Payments business area primarily comprises companies with both AIS and PIS approvals and hardly any companies that only have PIS approvals. In conclusion, this means that the companies are interested in account information in addition to payment initiation.

When examining the level of AI maturity, I found that both PIS and AIS have a high proportion of intelligent services, i.e., smart information systems or reactive machines are present. AIS has the highest proportion of AI-based services. When looking at the business areas, investments and payments had the lowest proportion of intelligent services. Reactive machines appeared primarily in the area of loans and mortgages. The decisive criterion for being categorized as a reactive machine was the ability to forecast credit decisions. smart information systems were mainly used by connectors. The goal of those services that were categorized as smart information systems was usually the aggregation or collection of financial data and the creation of user-friendly evaluations. These were primarily categorization, analysis and account aggregation functions. Applications rated reactive machines were primarily forecasts, automated credit decisions, fraud detection, planning tools, and authentication functions. Nearly all applications exhibiting some form of AI included Data Analytics (Da) as a functionality.

In conclusion, many of the companies initially focus their services and applications on collecting and analyzing customer data. From the customer’s point of view, this usually offers the advantage that applications are developed which combine a solution for all financial matters.

As demonstrated in the analysis, numerous approaches for AI services are already available on the market. Since PSD2 requires access to banks’ account data via APIs, this offers third-party providers, such as fintechs, the opportunity to intervene in the value chain of the financial industry. Thus, PSD2 has opened the way for technology-driven companies to access customer data and develop AI applications. Moreover, with the introduction of PSD2, new business models are developing in the banking sector. Some companies are using so-called open banking as a new business model, either offering an already developed API as a service or using their PSD2 licenses as a business model. The latter companies have acquired licenses for AIS and/or PIS and make these licenses available to other companies. Thus, for example, software companies without their own PSD2 license can gain access to the account data and offer special AI applications in the banking sector.

All in all, the PSD2 offers great potential for the banking sector in combination with AI applications, which will most likely become established in the future. Consequently, traditional banks face the great challenge of not completely losing customer contact to technology-driven third-party providers and not losing touch with the digitalization of the financial industry.

[1] “All” refers to services that can be used in all of the four business areas mentioned.

[2] The category Learning and its functionalities Category Learning (Lc) and Relationship Learning (Lr) were not included in the analysis. The reason for this is that no detailed information on the AI syst[ems was available, only the descriptions of the services based on the websites. It is assumed that all applications classified as Smart Information Systems or Reactive Machines already have learning functionalities or will soon get them.

Sources

Bitkom e.V. 2018, Digitalisierung gestalten mit dem Periodensystem der Künstlichen Intelligenz Ein Navigationssystem für Entscheider, Berlin. Available at: https://www.bitkom.org/sites/default/files/2018‑12/181204_LF_Periodensystem_online_0.pdf [06 Mai 2020]

Dietzmann C & Alt R 2020, `Assessing the Business Impact of Artificial Intelligence´, Proceedings of the 53rd Hawaii International Conference on System Sciences, pp. 5170-5179. Available at: http://hdl.handle.net/10125/64377 [06 Mai 2020]

Abele D & D’Onofrio S 2020, „Artificial Intelligence – The Big Picture“, in Cognitive Computing, Eds. Portmann E & D’Onofrio S, Springer Gabler, Wiesbaden, S.31-65.

Payment Service Directive II (PSD II) 2015, Available at: https://eur-lex.europa.eu/legal-content/DE/TXT/HTML/?uri=CELEX:32015L2366&from=EN

After completing his master's degree at the University of Leipzig, Benjamin Deubner started working as a consultant for a medium-sized management consultancy. Here, his focus is on mergers & acquisitions as well as restructuring and reorganization.