Five Data Strategies for Banks

The following blog post provides an overview of data strategies for banks and associated use cases that can be observed in practice.

Ideally, a bank’s data strategy should be derived from its corporate strategy. Possible goals of the data strategy can be process optimization with associated cost reduction, better customer understanding (which can also lead to cost reduction or revenue optimization), or the development of new business models.

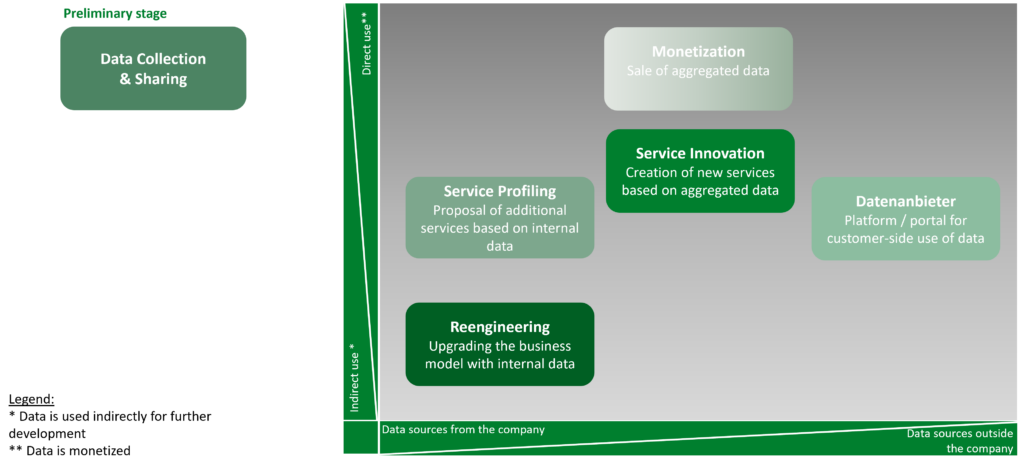

Basically, we distinguish between five strategic thrusts depending on the type of data source and the type of data use: Reengineering, Service Profiling, Service Innovation, Monetization and Data Provider. Data Collection & Sharing is a precursor to data use in the context of one of these thrusts.

Data Collection & Sharing involves providing free services for the purpose of collecting additional external customer data. In Deutsche Bank‘s multibanking app, for example, all accounts, cards, loans and securities accounts can be viewed at a glance – regardless of the bank. Offers from third-party banks can be added using the “Add bank” function. Expenses from third-party bank accounts are assigned to categories, such as living expenses, housing or travel[1]. The Australian Financial Crimes Exchange (AFCX), on the other hand, brings together businesses, government, law enforcement and industry groups to protect Australian consumers and businesses from financial and cybercrime. It does this through a platform where members can share fraud stories with each other and access leading security features, technology and information[2].

In Reengineering, internal customer data is evaluated and used to optimize existing processes or develop new processes. The evaluation of internal customer data can, for example, help to improve fraud detection or to obtain a 360-degree view of the customer.

One example in the area of fraud detection is Finnova, which enables customer risk-based profiling and behavioral analysis based on the analysis of customer and transaction data and behavioral patterns. The analysis includes both structured and unstructured data[3]. Another example is Danske Bank, which worked with Teradata to train a deep-learning algorithm that reports 60% fewer false positives and detects % 50 more true fraud cases. This allows the company’s internal resources to be better focused on the actual fraud cases[4].

Examples of the 360-degree view include AXA and Atruvia:

- With the EB360® platform, AXA provides its agents and brokers with tools for analyzing business performance or identifying and retaining clients[5].

- Atruvia is currently working on several projects for the cross-channel, intelligent analysis of customer data. This should, for example, enable the impulse manager to predict real estate purchases or other relevant customer events. When such an event is identified, the next-best actions stored in the system will then be triggered automatically and corresponding instructions for action will be sent to the consultants[6].

Service profiling describes the analysis of (internal) customer data to be able to offer the customer additional, precisely tailored services. If internal data is combined with external data and condensed into knowledge to develop new products and services, this is called service innovation. Examples of service profiling and innovation are as follows: Schwyzer KB developed a recommender system together with the Institute for Financial Services Zug. The goal of the project was to find out which customers might be interested in which additional products based on their history and characteristics. The machine learning algorithm suggests possible target products from the combination of products already purchased and customer attributes. Additionally, the bank can specify its own recommendations (product preferences of the bank), which are subsequently suggested to the customers[7]. Another example of service profiling is offered by the voucher FinTech Optiopay. It operates two product solutions: the payment solution analyzes the reasons participating companies pay out money to their customers, such as an insurance claim, and offers customers advantageous payout options in the form of higher-value vouchers in cooperation with retail partners. In the account solution, Optiopay obtains access to the bank transaction data of the payee, such as the insurance customer, upon consent. Based on this data, the payout options can be personalized to a much greater extent[8].

Monetization is the process of condensing customer data into knowledge and making it available to external players for a fee. So far, only Australian and Japanese banks have dared to break what European banks usually consider a “taboo”: Mizuho Financial Group Inc. is starting to sell information about consumers’ spending behavior and other aggregated data in order to expand beyond the traditional lending business[9]. Westpac isselling anonymous, aggregated information on consumer spending patterns to other companies through a data-sharing platform called Data Republic. Commonwealth Bank, on the other hand, sells anonymous, aggregated information about transactions to its commercial bank customers[10].

What all three approaches have in common is that data leaves the company and there is therefore a risk that, on the one hand, the data will become outdated and, on the other hand, customers will not approve of this behavior. A more elegant approach is taken by PostFinance, which keeps customer data in-house and monetizes it there (after obtaining the corresponding declaration of consent from its customers). Companies can approach the PostFinance customer. First, the company defines the criteria of the target audience it wants to reach (such as market areas, age category, purchase amount) and defines the amount of the discount as well as the number of customers. PostFinance activates the offers for private customers (e-finance, PostFinance app) and the private customer redeems the respective offer in the store and initially pays the full purchase amount. The corresponding discount is debited to the company in the following month and credited to the private customer.

So there is no need to sell data externally. Corporates can give input on what their target segment is and what kind of campaign they want to use. PostFinance itself is responsible for governance, but at the same time, data is more up-to-date if it is hosted in-house[11].

The ultimate step, the marketing of his/her own data by the customer, is the strategy of the data provider. This refers to the use of data by the customer, which the company supports by providing a platform or portal. Banks have not yet adopted this strategy, but there are other providers. One example is BitsaboutMe. People can manage their personal data and sell it through this platform. This offering is also supported by Deutsche Bank, among others.

[1] https://www.deutsche-bank.de/pk/digital-banking/digitale-services/multibanking.html

[2] https://www.afcx.com.au/afcx-exchange/

[3] https://www.finnova.com/de/understand-your-customer.html

[4] https://assets.teradata.com/resourceCenter/downloads/CaseStudies/CaseStudy_EB9821_Danske_Bank_Fights_Fraud.pdf

[5] https://equitable.com/employee-benefits/broker-resources

[6] https://veranstaltungen.handelsblatt.com/bankengipfel/smart-data-aus-daten-wird-wissen/

[7] https://blog.hslu.ch/retailbanking/2017/01/30/wie-koennen-retail-banken-data-analytics-einsetzen-use-cases-und-der-ansatz-der-schwyzer-kantonalbank/

[8] https://paymentandbanking.com/unternehmen-der-fintech-branche-optiopay-gmbh/

[9] https://www.bloomberg.com/news/articles/2020-11-09/mizuho-to-become-first-japan-bank-to-start-selling-consumer-data

[10] https://thenewdaily.com.au/finance/finance-news/2018/04/06/big-banks-sell-data-customer-spending-habits/#:~:text=Inquiries%20by%20The%20New%20Daily,with%20NAB%2C%20ANZ%20and%20Qantas.

[11] https://blog.hslu.ch/retailbanking/2019/12/02/welche-bankkunden-sind-bereit-ihre-kundendaten-fuer-mehrwerte-einzutauschen-erste-auswertungen-von-postfinance-benefit/#:~:text=Seit%20dem%20Start%20von%20PostFinance,CHF%20Verg%C3%BCnstigung%20durch%20Rabatte%20profitiert.