FinTech landscape in Switzerland: Blockchain and DLT

Switzerland is a leading innovation center

With a share of 10% of all FinTech companies in Europe, Switzerland is one of the leading innovation centers [1]. This share is particularly remarkable when one considers that only just over 1 % of all European inhabitants live in Switzerland. The fact that so many FinTechs are located in Switzerland is certainly not only due to advantageous tax regulations and legal framework conditions, but also to innovative business models. The focus on distributed ledger technology is striking in Switzerland, especially in Crypto Valley Zug. In the meantime, 250 crypto companies have already settled there or are planning a location [2]. However, Switzerland cannot rest on its laurels: to remain a leading innovation center, it constantly needs new FinTechs with innovative ideas. In order to identify gaps in the existing range of Swiss blockchain FinTechs and thus the innovation potential for further services, I analyze in this article the current service offering of the Swiss blockchain FinTech scene.

My research is based on data from the platform crunchbase and the FinTech Map from Swisscom [3] (in collaboration with e.foresight, Fintechdb and the Lucerne University of Applied Sciences and Arts). The search for blockchain-/DLT-FinTechs based in Switzerland resulted in 167 hits. Of these, 117 blockchain/DLT-FinTechs still have a valid Internet presence.

In addition to demographic data, the primary technology used, the customer target group, the service offering and the value proposition of each company were investigated and documented.

Services are offered in bundles

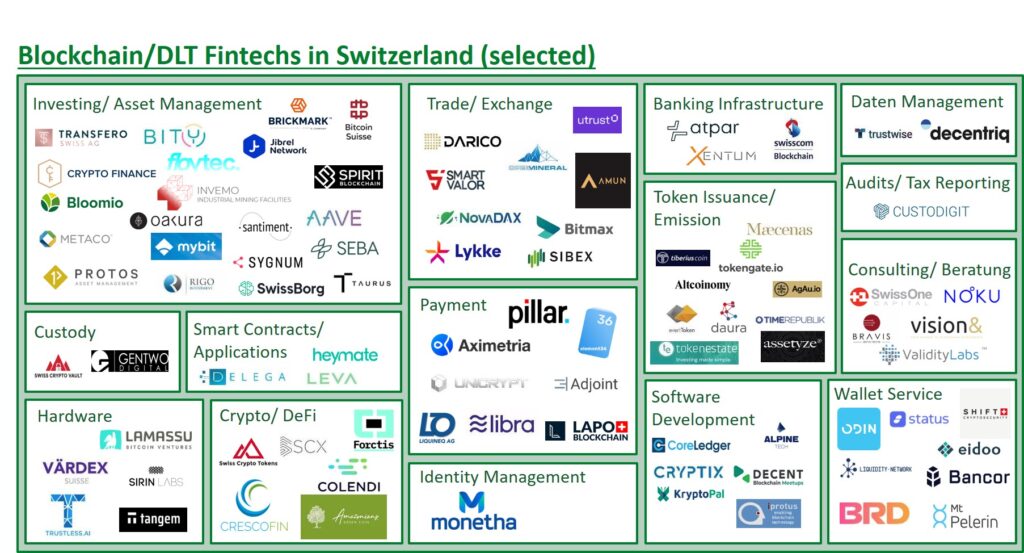

The Swiss market of blockchain/DLT-FinTechs is relatively large, but the number of applications is concentrated in certain areas. The most frequently offered services include applications in the areas of cryptocurrency (59%), investment and asset management (57%) and issuance of tokens (46%). The area cryptocurrency comprises all services that offer the sale and trading of cryptocurrencies (trade and exchange) or wallets for managing and using the currencies. Investment services (investment and asset management) refers to the offering, management and custody of any assets and issuance of tokens includes FinTechs, which use the blockchain to digitally display and distribute assets. However, hardly any blockchain/DLT FinTech offers only one service, but usually between two and five bundled services. This makes sense, since services such as token distribution and the organization and custody of the tokens often complement each other well. Payment applications (35 %) are offered by more than a quarter of the FinTechs analyzed. In last places are consulting and smart contract services with 17 % each of the analyzed blockchain/DLT FinTechs, providers of hardware, such as crypto-ATMs or hardware wallets, with 9 % and lastly tax reporting with only 1 % of the analyzed FinTechs. Thus, blockchain/DLT FinTechs in Switzerland are currently primarily specialized in the use of cryptocurrencies and assets as capital goods and means of payment.

Investment and asset management

More than half of the analyzed blockchain/DLT FinTechs offer services in the area of investment and asset management (57%). This area thus represents the biggest focus of the DLT/blockchain scene in Switzerland, as the cryptocurrency area is composed of several different offerings such as trade/exchange, decentralized finance and wallet service. However, the field of applications is still broad and varies in the type of service and the underlying asset. The services can be divided into different profiles: The largest group consists of companies that market various types of assets. The services range from cryptocurrencies, company shares and real estate to art, wine and precious metals. In addition to the distribution of assets, these companies also offer platforms for the management and organization of such assets. End customers can thus observe the development and possible risks of their investments and react to them. The asset management and asset sales applications are both services for end customers. 42 % of the analyzed blockchain/DLT FinTechs which offer services in the area of investment focus with their current offer only on the B2C area. In addition, 32 % of the blockchain/DLT FinTechs offer innovation services for B2B and B2C customers. These are mostly platforms that connect companies and investors. The remaining 26 % of the companies focus on corporate customers.

The value propositions of the blockchain/DLT FinTechs in the two mentioned service fields are often very similar. The safeguarding of the protected property rights of assets is of great importance. In this context, it is additionally relevant for the users to have access to current information at any time in order to be able to react flexibly. This is possible with the use of blockchain through the distributed storage of the ledger, which is why the value proposition of transparency and real-time information dissemination is significant for 56% of innovation FinTechs. The added value of using a network, which manifests itself, for example, in the fact that customers can share the investment in a valuable object and thus make even small investments, is particularly decisive for platforms.

Blockchain, smartphones and the tokenization of time

The customer benefit from the services offered does not differ significantly from FinTech to FinTech. Services in the same area are almost always structured in the same way and pursue a similar purpose. For example, there are several wallet providers that enable the purchase and administration of different cryptocurrencies, and several trading platforms that offer the exchange of cryptocurrencies. Nevertheless, areas with a large number of similar offerings are also growing. Figure 2 gives an overview of the distribution of Fintechs among the individual product areas.[4]

Despite the high number of FinTechs with similar services in individual areas, there are of course always start-ups with new, innovative ideas. For example, one company offers the management and storage of signatures. This is intended to replace paper-based contracts with digital agreements, thereby enabling automated processes and simplifying complex procedures, e.g. of a regulatory nature. This service can be located in the area of smart contracts. One company in the hardware sector has even developed a blockchain smartphone, which is intended to have a secure operating system that allows cryptocurrencies to be stored and used on a mobile device without any problems.

The service sector issuance of tokens deals mainly with the sale of cryptocurrency tokens or company shares or with tokenization, i.e. the digital representation of assets such as cars, houses or watches for investment and value enhancement. However, blockchain technology can do more than tokenize valuables, as demonstrated by a company dedicated to a new “object”: time. The corresponding company enables users to offer or request assistance such as repairs or tutoring. For each service performed, the time spent is credited to the respective “service provider” on the blockchain. With the credit note, any other service offered on the platform can then be claimed. There is no pegged currency, the only exchangeable currency is time against time.

Another FinTech in Switzerland uses the technology of tokenization for a decentralized power grid for users in South America. The service has above all a sustainable and social background. On the one hand, residents in villages without electricity connection receive a power supply based on solar energy, and on the other hand, by repaying the initial hardware costs in installments, they receive a credit score which they can then use, for example, to apply for microcredits. These two aspects of everyday life, electricity supply and financial inclusion, which are taken for granted in western countries, can change the whole life of those customers.

Mainly services for selected target groups

The number of companies with B2B and B2C business models is relatively balanced. Most blockchain/DLT FinTechs (35%) only address the direct end customer. However, the share of FinTechs in pure B2B business is not much smaller at 31% and 34% of the companies analyzed offer services for both companies and private customers.

Despite the balance between end and corporate customers, the customer profile of blockchain/DLT FinTechs is still very rigid and one-sided. In the B2C segment, cryptocurrency services are mainly offered to investors. In addition, they mostly require employees with equity and reserves as collateral. This shows a gap in terms of potential customer groups. For example, various solutions for teenagers and young people or platforms for the administration of pension payments for senior citizens could be offered. In addition, low-income earners have different needs and demands than financially strong customers.

Steady growth of the FinTech landscape?

Starting up a business requires courage, as this step always involves a risk. The success rate of start-ups seems to be low; figures show that up to 8 out of 10 start-ups fail [5]. It is difficult to estimate the exact number of cases in the FinTech sector in Switzerland. However, the short-lived nature of the companies is also reflected in the analysis conducted. Of the 167 blockchain/DLT FinTechs listed in the search results, only 117 FinTechs with a valid Internet presence currently exist. This means that 30% of the blockchain/DLT FinTechs that were already on the market have disbanded within a very short time.

Nevertheless, the high drop-out rate does not pose a threat to the industry or the degree of innovation in Switzerland, because the number of blockchain/DLT FinTechs is nevertheless increasing continuously in all areas over time. Investment management applications have always been the most strongly represented [6].

Potential for new business models

The current range of blockchain/DLT FinTechs in Switzerland is diverse, but still has potential to develop in other directions. The concentrated service offers in the individual areas are striking. Most blockchain/DLT FinTechs focus on cryptocurrencies and the investment in various assets. The combination of several services in one company makes sense considering that the FinTechs can maintain and expand their basic product and specialize with additional services. This makes it possible to build a more individual business model. Nevertheless, it is important to remember that the development of a start-up is always associated with risks. In addition to the development of already existing companies, continuous growth needs to be encouraged.

[1] Swissquote: Was bedeutet FinTech?, https://de.swissquote.com/robo-advisory/why-robo-advisory/fintech [2] CoinPro.ch: Die Bitcoin-Hauptstadt – Das Crypto-Valley Zug, https://www.coinpro.ch/das-crypto-valley-zug/ [3] Swisscom: FinTech Startup Map, https://fintechmap.ch/ [4] For the sake of simplicity, the areas trade/exchange, crypto/defi and wallet service have been grouped together under the generic term “cryptocurrency” in Figure 1. The same applies to data management and identity management (“data and identity management”) and banking infrastructure and software development (“infrastructure and development”). [5] Startup Unternehmen: Startup-Scheitern / Gründe, https://www.start-up.ch/umstrukturierung-scheitern/start-up-scheitern-gruende/geringe-erfolgsquote [6] Institut für Finanzdienstleistungen Zug (2020): IFZ FinTech Study 2020, https://de.statista.com/statistik/daten/studie/687385/umfrage/fintech-unternehmen-in-der-schweiz-nach-bereich/

- The Business Side of the Blockchain Map - 28.05.2021

- The Technical Side of the Blockchain Map - 28.05.2021

- The BlockWiki – the Blockchain Explained - 14.05.2021