Distributed Ledger Technology for the Real Estate Market – A Meaningful Synthesis?

The real estate industry is a fundamental sector of the economy and has an essential influence on the financial markets [1]. For example, in Germany, 800,000 companies are located in the real estate sector and employ more than 3.5 million people. [2]. The 2008 financial crisis has shown that the link between the real estate and financial industries is not only highly relevant on a national level, but that global spillover effects[a] can occur due to the global interconnectedness of the financial and real estate industries.

Lack of transparency and control led to a global economic crisis in 2008. In the 1990s, a low key interest rate in the USA meant that US citizens were increasingly able to afford a mortgage loan for a home. There was a veritable construction boom, and demand for real estate and its prices rose. Banks used these mortgages to create new financial products, collateralized debt obligations (CDOs). A CDO is rated by a rating agency (e.g. S&P Global Ratings) and is a special type of financial product. The basis for this product is the resale of bank loans to a buyer, such as an investment bank. The buyer assumes the position of the bank and can enforce the credit claims. CDOs bundle a large number of such on-lent bank loans into a single pot. Other investors, insurance companies or pension funds can subsequently invest in this pot [4]. Thus, in the context of the financial crisis, mortgage loans were made “investable” on a large scale through the use of CDOs. In the case of mortgage loans, CDOs are particularly interesting because the loan is secured by the underlying property. In the event of default, the loan creditor can sell the property at any time [5].

Due to attractive interest yields, CDOs with mortgage loans enjoyed increasing popularity. To meet demand, mortgages were also granted to people with poor credit ratings. Manual processes and non-transparent information exchange led to the granting of the so-called subprime loans [6]. Thus, CDOs included not only loans from credible borrowers, but also loans with a high risk of default. Assuming that house prices would continue to rise permanently, this did not pose a problem for banks; real estate could always make up for borrower defaults. CDOs continued to receive top ratings from the rating agencies. When there was a deterioration of the overall economic situation in the U.S. in 2005 (weak consumption, decreased investment) [7], many debtors could no longer repay their loans and had to sell their properties.

The market was flooded with real estate, and a supply overhang caused property prices to fall rapidly. As a result, investors were left with billions of dollars in CDO defaults, also in Europe. Investors sensing this trend strategically bet on the default of the loans and thus also of the CDOs, which harbored a high proportion of default risks, and reaped substantial profits. Non-transparent loan compositions of CDOs eventually led to a loss of confidence both among and in banks [8].

Challenges in the Real Estate Industry

The global financial crisis is a prime example of the relevance of the real estate industry for and the close interdependence with the financial industry. In order to prevent the real estate market from negatively impacting the financial industry, various challenges need to be solved (see Figure 1). These challenges have similarities to the problems of the 2008 financial crisis. Therefore, different challenges in the real estate industry can be derived from the example of the financial crisis.

Fundamentally, transparency needs to be improved with regard to lending as well as the general mortgage process. Stricter regulations for mortgages are needed, and risky derivatives trading on secondary markets must also be curbed [9]. This is the only way to prevent negative scenarios like the 2008 financial crisis in the future.

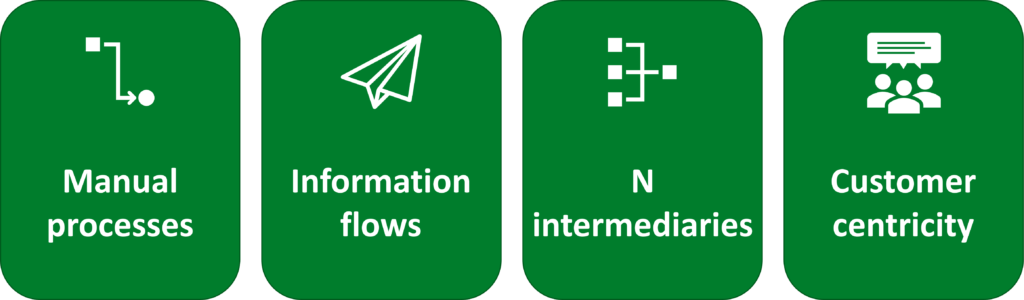

Structural deficiencies in the real estate industry accelerated the devastating effects of the financial crisis and are still highly relevant today. Manual processes as well as a large number of intermediaries in the settlement of real estate purchases create complex relationships between individual contracting parties. On the one hand, this does not always ensure that all parties have the information they need or that this information is trustworthy. The validity and authenticity of documents such as contracts and certificates can currently only be guaranteed via intermediaries (for example, notaries). On the other hand, the process of buying real estate is very inefficient due to the many intermediaries and the low degree of automation, which leads to high expenses for the buyer of a property. The fact that contracts and property certificates are still drawn up in physical form also increases transaction costs. In addition, customers expect advanced services such as proof of past damage, repair work or invoices for a property in digital form and in real time. As a result, the speed of information exchange in the industry needs to increase to meet the new demands [9]-[13].

Technological innovations such as distributed ledger technology (DLT), and blockchain technology in particular, have opened up new opportunities in recent years to address the aforementioned challenges. In this post, we analyze the impact of DLT on the individual steps of real estate acquisition (especially the mortgage process). In order to do this, we first present the characteristics of DLT and the Blockchain as well as the generic value chain of the real estate industry. The explanations are then complemented by potential application areas of the technology.

DLT: Definition and Characteristics

Distributed ledger technology (DLT) is a digital system that uses a distributed database infrastructure. This consists of several independent but interconnected nodes. The goal is the distributed and immutable storage of identical data in chronological order [14]. A node is represented by a person or an organization with access rights to the distributed network [15]. Different concepts of DLT differ in their design, properties, and characteristics (for example, Bitcoin vs. Ethereum). Nevertheless, each DLT concept consists of public-key cryptography, a peer-to-peer distributed network, and a consensus mechanism [16].

Features of the Blockchain

Blockchain is not the only DLT concept, but it is the best known and most widely used. Therefore, we will focus on the blockchain in the following. In presenting its characteristics, we use the categorization from the (German) blog post Blockchain, more than just hype? by Ante Plazibat from 2016:

Data on the blockchain is immutable (1) and stored in cryptographic blocks in a decentralized manner (2). This solves the single point of failure[b] problem of traditional databases. Furthermore, data can be viewed transparently (3) by users authorized to access the blockchain. Data redundancies are solved by the concept of single-source-of-truth (4). All participants always see the same data sets. Another advantage of the technology is programmability (5). This feature allows code to be executed on the blockchain. Thus, contractual terms and processes can be mapped on the blockchain by using so-called smart contracts [18].

Value Chain in the Real Estate Industry:

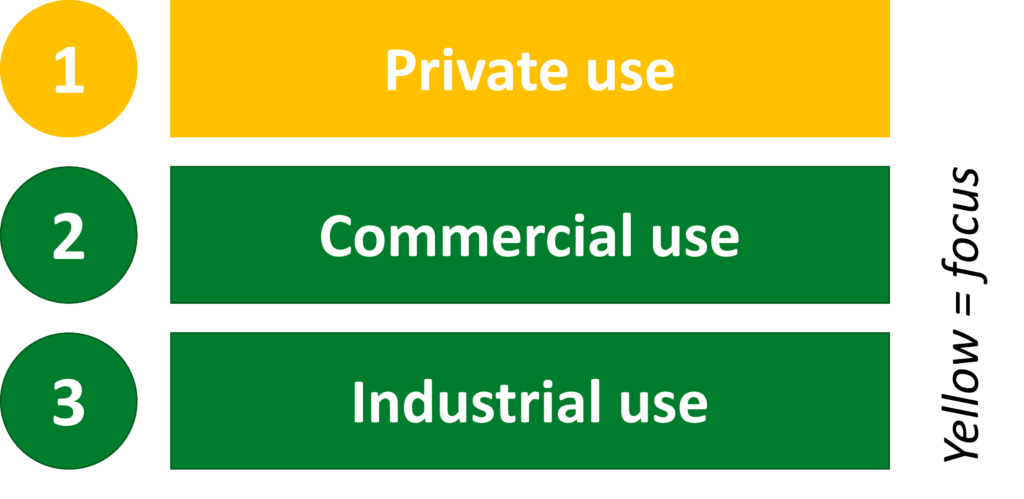

In order to understand the generic value chain of the real estate industry, it is first necessary to differentiate different uses of a property (see Figure 2): private use (1), commercial use (2), and industrial use (3) [19]. Depending on the area of use, the value chains vary.

This article focuses on the value chain for the private purchase and private use of a property (see Figure 3). It shows by way of example how buyers and sellers of a property come together and how DLT can support this process.

In the first step, a broker goes in search of real estate properties available on the market (1: Search). The broker acts as an intermediary between buyer and seller [20]. While this process is currently mapped via centralized Multiple Listing Services (MLS) [c], decentralized directories on the DLT enable fast and more efficient access to real estate information as well as associated building histories. Depending on the DLT design, access rights to the data can be defined. The immutability of the records increases trust in the data provided [22]. By introducing decentralized identity on the DLT, sellers can be identified in advance. This use case guarantees the broker secure, automated KYC processes as early as the property search stage [23].

Brokers provide buyers with further information about the property and arrange the sales process between buyer and seller (2.1: Sales). Examples of this information are for example: previous owners, deeds as well as repair work carried out [10]. Brokers also benefit from secure and transparent data during the sales process. Consultation, valuation of the object as well as the search for the necessary documents can be carried out quickly and securely.

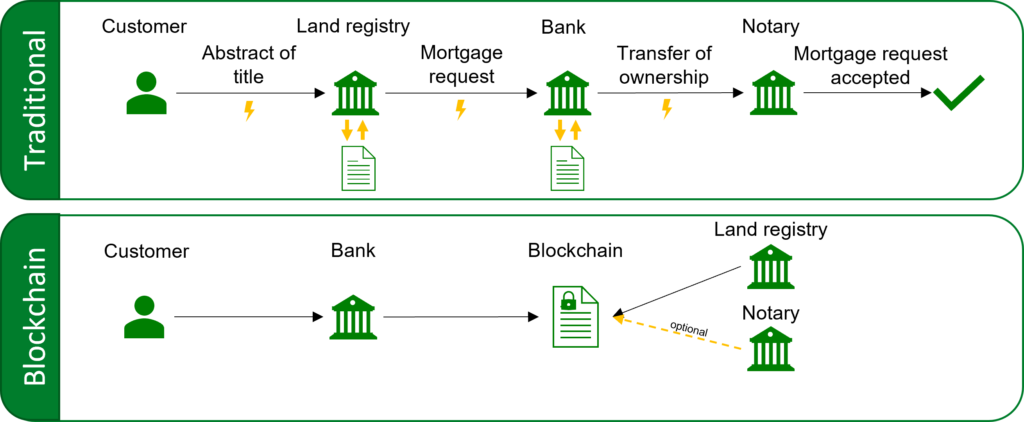

In the financing phase, the financing of the property is negotiated between the buyer of the property and the credit institution (2.2: Financing). In the traditional world, mortgage loans are mainly used for this purpose. Here, the mortgage taken out is registered in the land register of the property to be purchased (see Figure 4, traditional). In the event of default by the property owner, the bank can sell the property through the mortgage registration [24]. Currently, in order to legally conclude a sale (3: Contract), another authority is needed: the notary [25]. A notary confirms the purchase and enters it in the land register. The land register is a public register of land and contains information about legal relationships such as the owner [26]. Thus, the ownership of the property is transferred to the buyer.

By using DLT, process steps 2.1), 2.2) and 3) could be optimized in addition to the real estate search. The prerequisite for this is the digital land register, which is stored on the DLT [27].

Once a loan has been approved by a bank, it would be processed directly via DLT using smart contracts. A smart contract has access to the digital land register and automatically triggers the transfer of ownership in the land register after receipt of payment [28] (see Figure 4). Smart contracts require technological and process standards. The introduction and extensive standardization of real estate processes through smart contracts leads to more efficient and automated processes across the industry [29]. DLT provides a single-source-of-truth for real estate property, thus eliminating the need for multiple intermediaries. For example, notaries are no longer needed due to the transfer of property rights on the DLT. The final step in the value chain involves the buyer’s use of the property. In this step, too, the DLT could support the buyer by converging with other technologies such as the Internet of Things (IoT). The installation of networked sensors allows building data to be collected in real-time and stored directly on the DLT [30]. Data collection is consistent and transparent and could be accessed by future buyers. Thus, based on existing data, buyers could reliably determine expected expenditures for electricity, heating oil, or water consumption.

Conclusion

There are already a large number of use cases for the application of DLT in the real estate industry (search of the property, secure exchange of information, process automation). The introduction of a digital land register or decentralized identity on DLT will further exploit these potentials and new use cases will emerge (mortgage loan on DLT, smart contracts). Steady increases in transparency in the real estate industry with the help of digital technologies such as DLT reduce the risk of negative impacts of the real estate industry on the financial industry. Pilot projects such as the digital land registry “Lantmäteriet” in Sweden already demonstrate the relevance of the technology in practice [31].

[a] “Influencing the international political arena through social and economic decisions and developments at the national level.” [3]

[b] A single point of failure (SPOF) represents a potential risk. It can lead to a situation in which a single malfunction causes an entire system to stop functioning [17].

[c] ”A multiple listing service (MLS) is a database established by cooperating real estate brokers to provide data about properties for sale. An MLS allows brokers to see one another’s listings of properties for sale with the goal of connecting homebuyers to sellers.” [21]

Sources

[1] C. Buch, “Die Rolle des Immobiliensektors für die Finanzstabilität,” Nov. 12, 2019. https://www.bundesbank.de/de/presse/reden/die-rolle-des-immobiliensektors-fuer-die-finanzstabilitaet-814682 (accessed Nov. 29, 2022). [2] ZIA, “Bedeutung der Immobilienbranche,” ZIA, 2022. https://zia-deutschland.de/project/bedeutung-der-immobilienbranche/ (accessed Nov. 29, 2022). [3] P. D. E. Feess, “Definition: Spillover-Effekt,” https://wirtschaftslexikon.gabler.de/definition/spillover-effekt-43401 (accessed Nov. 29, 2022). [4] J. Ogg, “CDOs and the Mortgage Market,” Investopedia, Mar. 23, 2022. https://www.investopedia.com/articles/07/cdo-mortgages.asp (accessed Dec. 05, 2022). [5] C. Tardi, “Collateralized Debt Obligation (CDOs): What It Is, How It Works,” Investopedia, Mar. 08, 2022. https://www.investopedia.com/terms/c/cdo.asp (accessed Nov. 29, 2022). [6] H. Keller, “Definition: Subprime-Kredit,” https://wirtschaftslexikon.gabler.de/definition/subprime-kredit-53290 (accessed Dec. 05, 2022). [7] Handelsblatt, “Gebremstes US-Wachstum Ende 2005: Amerikaner haben zu wenig konsumiert,” Jan. 27, 2006. https://www.handelsblatt.com/politik/konjunktur/gebremstes-us-wachstum-ende-2005-amerikaner-haben-zu-wenig-konsumiert/2606696.html (accessed Nov. 29, 2022). [8] PostFinance, “Finanzkrise 2008 – der Rückblick und die Lehren daraus,” PostFinance, Sep. 05, 2018. https://www.postfinance.ch/de/privat/beduerfnisse/anlagewissen/finanzkrise.html (accessed Nov. 24, 2022). [9] LimeChain, “Blockchain in real estate: benefits and use cases,” Jan. 11, 2021. https://limechain.tech/blockchain-use-cases/real-estate/ (accessed Nov. 24, 2022). [10] A. D., “Blockchain and Real Estate: 7 Ways It Can Revolutionize the Industry,” Cleveroad Inc. – Web and App development company, Oct. 15, 2022. https://www.cleveroad.com/blog/how-blockchain-in-real-estate-can-dramatically-transform-the-industry/ (accessed Nov. 24, 2022). [11] Edelmann, “Immobilienbranche: Herausforderungen & Lösungsansätze,” Dec. 16, 2021. https://digitalland.ch/immobilienbranche-herausforderungen-losungsansatze/ (accessed Nov. 29, 2022). [12] A. Biel, “Einfluss der Digitalisierung in der Immobilienwirtschaft – Herausforderungen und Chancen zur Verbesserung der UX 1/2,” E-Commerce Institut Köln, Nov. 18, 2020. https://ecommerceinstitut.de/einfluss-der-digitalisierung-in-der-immobilienwirtschaft-herausforderungen-und-chancen-zur-verbesserung-der-ux/ (accessed Nov. 29, 2022). [13] M. R. Itani, “The Impact Of Digital Transformation On The Real Estate Sector,” Entrepreneur, May 13, 2022. https://www.entrepreneur.com/en-ae/technology/the-impact-of-digital-transformation-on-the-real-estate/427491 (accessed Nov. 29, 2022). [14] A. Sunyaev, “Distributed Ledger Technology,” in Internet Computing: Principles of Distributed Systems and Emerging Internet-Based Technologies, A. Sunyaev, Ed. Cham: Springer International Publishing, 2020, pp. 265–299. doi: 10.1007/978-3-030-34957-8_9. [15] N. Kannengießer, S. Lins, T. Dehling, and A. Sunyaev, “What Does Not Fit Can Be Made to Fit! Trade-Offs in Distributed Ledger Technology Designs.” Rochester, NY, Jan. 10, 2019. doi: 10.2139/ssrn.3270859. [16] N. El Ioini and C. Pahl, “A Review of Distributed Ledger Technologies,” in On the Move to Meaningful Internet Systems. OTM 2018 Conferences, Cham, 2018, pp. 277–288. doi: 10.1007/978-3-030-02671-4_16. [17] Avi Networks, “What is a Single Point of Failure? Definition & FAQs,” Avi Networks, 2022. https://avinetworks.wpengine.com/glossary/single-point-of-failure/ (accessed Nov. 25, 2022). [18] M. Finck, “Grundlagen und Technologie von Smart Contracts,” in Smart Contracts, M. Fries and B. P. Paal, Eds. Mohr Siebeck GmbH and Co. KG, 2019, pp. 1–12. Accessed: Nov. 25, 2022. [Online]. Available: https://www.jstor.org/stable/j.ctvn96h9r.4 [19] RealT Horizon, “Understanding the reality in RealT – Generic Real Estate Value Chain.” http://www.realthorizon.com/2013/02/understanding-reality-in-realt-generic.html (accessed Nov. 24, 2022). [20] “Aufgaben eines Maklers: Tätigkeiten im Überblick | Makler-Vergleich.de,” 2022. https://www.makler-vergleich.de/immobilienmakler/aufgaben-eines-maklers.html (accessed Nov. 29, 2022). [21] J. Chen, “Multiple Listing Service (MLS): Definition, Benefits, and Fees,” Investopedia, Jan. 21, 2022. https://www.investopedia.com/terms/m/multiple-listing-service-mls.asp (accessed Dec. 05, 2022). [22] T. Merrill, “Blockchain In Real Estate: 6 Ways It’s Changing the Industry,” FortuneBuilders, May 16, 2022. https://www.fortunebuilders.com/blockchain-real-estate/ (accessed Nov. 29, 2022). [23] ConsenSys, “Blockchain in Real Estate | Real World Blockchain Use Cases,” ConsenSys, 2022. https://consensys.net/blockchain-use-cases/real-estate/ (accessed Nov. 29, 2022). [24] I. Fronia, “Hypothek,” immoverkauf24 GmbH, Dec. 23, 2021. https://www.immoverkauf24.de/baufinanzierung/baufinanzierung-a-z/hypothek/ (accessed Nov. 29, 2022). [25] Redaktion Dr. Klein, “Notartermin und Beurkundung: Ablauf beim Hauskauf,” 2022. https://www.drklein.de/notartermin-hauskauf.html (accessed Nov. 29, 2022). [26] D. B. Wischermann, “Definition: Grundbuch,” https://wirtschaftslexikon.gabler.de/definition/grundbuch-33315 (accessed Nov. 29, 2022). [27] S. Herrnberger, “Digitales Grundbuch mit Blockchain – so profitiert die Branche,” Blockchainwelt, Nov. 28, 2020. https://blockchainwelt.de/kein-digitales-grundbuch-mit-blockchain/ (accessed Nov. 29, 2022). [28] A. Plazibat, “Blockchain: Heiliger Gral oder überbewerteter Hype? Erkenntnisse aus der Finanzindustrie | ccecosystems.news,” Dec. 07, 2017. https://ccecosystems.news/blockchain-heiliger-gral-oder-ueberbewerteter-hype-erkenntnisse-aus-der-finanzindustrie/ (accessed Nov. 29, 2022). [29] block.co, “The Potential of Blockchain Technology in Real Estate,” Medium, Aug. 30, 2021. https://blockdotco.medium.com/the-potential-of-blockchain-technology-in-real-estate-d6b1bbd38e73 (accessed Dec. 05, 2022). [30] Intellis, “What are the benefits of Blockchain for Facilities Managers in 2020?,” 2020. https://www.intellis.io/blog/what-are-the-benefits-of-blockchain-for-facilities-managers-in-2020 (accessed Nov. 29, 2022). [31] D. Noll, “Distributed-Ledger-Technologie im Grundbuchwesen,” May 2019.

- Are our jobs at risk? - 23.01.2024

- Are Our Jobs at Risk? - 10.01.2024

- Research Area Distributed Ledger Technology - 29.08.2023