Classification of Blockchain-Based Applications: A Conceptualization from a User Perspective

The blockchain (BC) and its underlying distributed ledger technology (DLT), made famous primarily by the cryptocurrency Bitcoin, offer a much-discussed alternative way to digitally execute, record, and process transactions [1]. Before the introduction of this disruptive technology, transaction data could usually only be managed centrally by one entity. Due to the characteristics of the blockchain[1] and a technical agreement between several different parties, the so-called consensus, it is now possible for the first time to manage any number of identical copies of transactions without a central intermediary and to synchronize them in case of conflict (e.g., double-spending of already issued digital currency) [2].

Despite many known advantages, such as increased authenticity and security, it is still difficult, especially for practitioners, to identify concrete application areas for blockchain-based applications [3]. While startups are quicker to operationalize disruptive technologies and create new business models, large established companies struggle to implement innovative services due to existing processes and legacy systems [4].

This article takes this as its starting point and presents a sector-independent typology of application fields, which not only serves to analyze existing blockchain applications, but also provides users with an orientation as to which general possible uses there are for the blockchain and how complex an initial implementation of the respective applications can turn out to be.

Collaboration and Process Complexity of Blockchain-Based Applications.

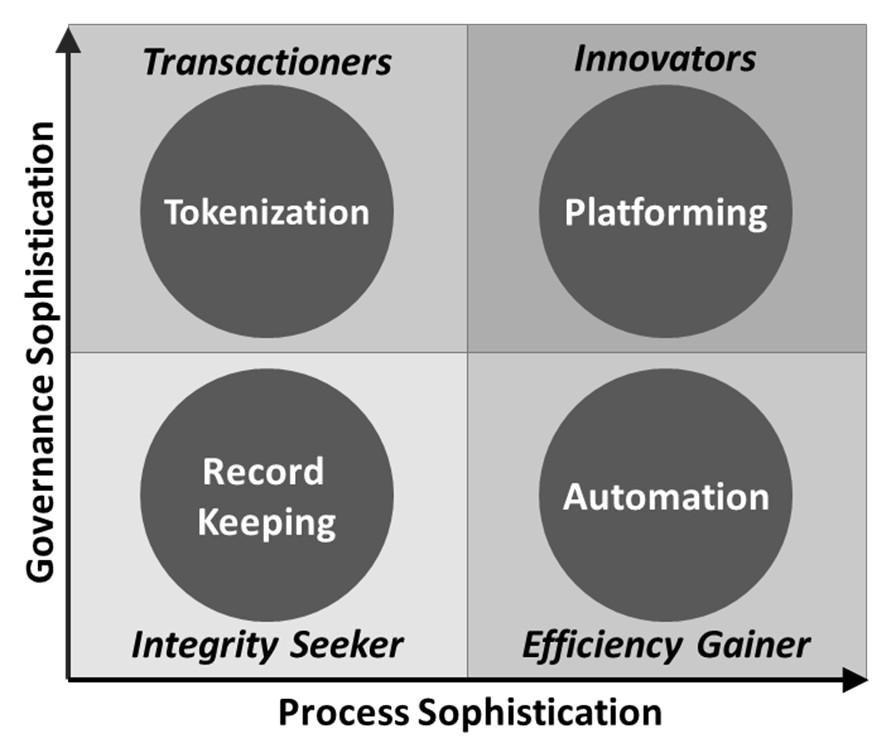

Blockchain applications can be characterized along two fundamental dimensions that represent the impact of using a blockchain-based, decentralized platform on existing cooperation structures and processes: cooperation complexity and process complexity. Because the technical features of the technology enable distributed management of transactions of all types, a trusted party is no longer needed to authenticate transactions. This disintermediation not only leads to a “re-design” of processes, but also results in a change in the participants of existing business structures (e.g., companies in the financial network). Both dimensions are explained in more detail below:

Cooperation Complexity

One difficulty in using blockchain-based decentralized platforms often lies in the peer-to-peer structure, which puts all participants on an equal footing. To implement such a platform, common business processes and activities must be translated into programmable logic as a first step and replicated within a specific blockchain tech stack. Thus, before initiating a specific blockchain network, the various actors must agree on a common platform and a specific protocol, for example. Changes to the protocol, to integrate additional functionalities for example, can only be made with the agreement of all parties involved in the blockchain consortium, which can lead to an extra effort of coordination between the different parties. The more existing cooperation structures are changed by the use of blockchain, the more difficult cooperation becomes. While some use cases change existing structures in the financial industry only marginally, Bitcoin is an example of a complete disintermediation of the payment system and thus probably the biggest possible structural change. Similarly, as more business processes are formalized by the blockchain, coordination among the parties becomes more challenging. Therefore, cooperation complexity is the first dimension of the framework [5].

Process Complexity

The second dimension of the framework is process complexity. The smart contract functionality, i.e., the automatic execution of rules and instructions based on business logic stored on the blockchain, offers enormous potential for many companies. As the consistency of transaction data is improved by the tamper-proof storage of the replicated ledger, smart contracts enable automated execution of almost all upstream and downstream tasks; for example, when a cryptocurrency is purchased, all tax-related data could be forwarded directly to the relevant authority. From a technological perspective, the blockchain is virtually predestined for process optimization and can drastically reduce transaction costs [6]. However, depending on how many processes are automated and how many cooperation partners are involved in a process, the complexity of designing and implementing smart contracts can vary greatly from application to application.

Based on these two dimensions, the following framework emerges with four dimensions: record keeping, automation, tokenization, and platforming:

Record Keeping

All entries that are displayed on an open blockchain can be traced pseudonymously by all participants in the network. Each block consists of cryptographically sealed transaction data, which is more secure against manipulation. A transaction can only be reversed with the consent of all participating nodes. The fact that the data recorded on a blockchain is unchangeable, transparent, complete and therefore has absolute integrity enables a wide range of documenting use cases, from ensuring the origin of any certificates in the area of compliance to automated verification of digitized data records. If complete transparency is not desired, there is the option of a closed solution to which only a limited number of users have access. The digital verification of documents or the tracking of objects kept in registers represent an important economic factor. Possible users are not only verifying companies, auditors or certifiers, but also manufacturers tracking their products. Companies seeking business value in this application area can be called integrity seekers. Primarily, the aim is not to establish new business models, but to use the blockchain as a tamper-proof database. Due to a low level of smart contract functionality, the implementation effort is kept within limits compared to other blockchain solutions and benefits are achieved quickly. A pilot project in this area is, for example, the forgery-proof verification of certificates.

Automation

Distributed ledger technology can not only address inefficiencies in data sharing, but also lead to a paradigm shift in the automation of business interactions. Conventional business processes are based on siloed IT services that are handled within organizations and between business units. For further efficiency potential, business logics must therefore be understood as end-to-end processes across companies. Where a blockchain- and DLT-based, fully distributed peer-to-peer system creates a shared view of a process state, multiple unknown actors can share information and ensure the integrity of the corresponding process. The rules and policies for a wide variety of workflows are mapped into smart contracts in the form of executable code segments. Process steps are more transparently traceable for users with a connection to the decentralized platform. This leads to a new kind of seamless integration and real-time auditing with reduced dependency on individual IT providers. The more processes and functionalities are mapped on the blockchain, the more complex the technical implementation and integration becomes. Companies seeking process optimization through automated business processes are referred to as efficiency gainers. In particular, applications in trade finance and logistics demonstrate these process-related advantages of the smart contract concept. Here, the TradeLens platform contributes to the digitalization of the global supply chain between traders, carriers, inland transport, ports and terminals, maritime shipping, customs, other authorities and other participants by enabling them to collaborate for the first time based on secure authorization and identity frameworks through the blockchain. Where a lack of trust in data exchange between stakeholders hinders collaboration, blockchain enables a single-source-of-truth between equal supply chain partners. Cross-enterprise business processes, such as import and export processing, are pre-programmed, integrated into the blockchain, and distributed and executed on the network so that no participant can change the business logic. However, the implementation of complex smart contracts is more error-prone, which can lead to increased process complexity.

Tokenization

Since the data stored on the blockchain cannot be manipulated, values such as access rights, ownership of goods or intangible assets with certain properties can also be represented and stored on it. These values can be efficiently transferred from one actor to another within the system. This transferability is seen as the basis of the so-called Internet of Values, which is intended to complement today’s centralized information architecture. Cryptocurrencies represent the most obvious applications where property rights are mapped “on-chain,” i.e., on the distributed ledger. A more innovative way of recording transactions is known as tokenization. It describes the digitalization of assets that links specific rights to real-world assets to facilitate trading and settlement. The benefits of the blockchain as a common platform are not based solely on efficiency gains from automated smart contracts, but also on the reduction of interfaces that results from participants not only working with a common, distributed database, but also with a common process logic and thus a common backend. For a token-based business model to establish itself and trigger a network effect, a so-called “minimal-viable ecosystem” is first needed to ensure minimal requirements for the exchange and trading of value, such as liquidity. Cryptocurrencies, such as Bitcoins, are a type of token that have the ability to be exchanged with other assets of the same type. I don’t have to own a specific Bitcoin, as each Bitcoin has the same value and function, and is therefore completely interchangeable. However, unique, non-exchangeable (non-fungible) assets can also be represented on the blockchain. As a result, distributed platforms can emerge to map both ownership and usage rights or the lifecycle of any asset. Organizations engaged in tokenization capabilities are so-called transactioners. The concept of tokenization offers many advantages, such as fractional ownership or increased liquidity. In particular, the digital representation of existing assets, such as stocks or bonds, has so far become a promising use case in the financial industry, with asset management practitioners predicting potential savings of up to $2.7 billion per year in fund buying and selling alone [7]. Binance, one of the largest and best-known crypto exchanges in the world, for example, has already started tokenizing Tesla shares and distributing them on its platform.

Platforming

The decentralization and immutability of the blockchain and the opportunities created by tokenization and smart contracts have the potential to challenge the business models of many organizations. Blockchain-based platforms are expected to transform existing financial market infrastructures, among other things, as the Swiss Digital Asset Ecosystem around Daura has set out to do, for example. As the issuance of shares for tapping debt capital has traditionally been associated with high costs, this market has not been economical or accessible for SMEs in particular. A DLT-based infrastructure helps to democratize the market, since, for example, costs can be reduced by eliminating intermediaries. This opens up new business opportunities that were not possible or economically viable before blockchain.

If we look at the Swiss stock market, for example, we see that only very few companies are listed on the stock exchange. And this despite the fact that SMEs are the backbone of our economy. Similarly, the SME debt market is not publicly accessible, but traditionally in the hands of banks. A DLT trading platform could enable SMEs to tap additional sources of finance through lower issuance costs and access barriers. Opening up this asset class could not only benefit SMEs and investors, but also free up tied-up capital from bank balance sheets and make it available for further economic development activities.

Efficiency gains can also be achieved in the environment of traditional financial assets through the use of DLT. This can be illustrated by the use of smart contracts. For instance, one can imagine smart and automated solutions for the settlement of structured financial products. In the case of so-called special purpose acquisition companies (SPACs), we can concretely see an application example: SPACs raise funds on the stock exchange in order to invest them in private companies over a fixed period of time, usually 18 to 24 months, and thus take them public without going through the costly and lengthy IPO process. However, if no investment target can be identified in the specified time, the funds go back to the investors. This repayment could be completely automated through smart contracts. In addition, this minimizes the investment risk for investors.

Specific technical elements that are inherent to distributed ledger technology, such as cryptography, digital signatures and the peer-to-peer structure, can also create a new basis for business platforms that support the development of ecosystems in interdisciplinary corporate networks. Especially as infrastructure for data-driven business models, so-called blockchain-based ecosystems represent a next step in digitalization. Distributed consensus replaces the role of a trusted third party and ensures that all participants collaborate more efficiently. Since every business ecosystem must generate value for its users and customers, these applications achieve above-average advantages over conventional solutions through high structural as well as process implications. An example of such an implication is the elimination of counterparty risk through rule-based, automatic transaction execution using smart contracts, relevant, for example, for payment against delivery. If both assets, the currency and the asset to be purchased, such as a share, reside on the blockchain in the form of tokens, the need for an intermediary is eliminated, as the transaction is only made when both parties have sent the respective token to the smart contract and thus fulfilled the terms of the contract. Platforming makes it possible to create marketplaces that bring sellers and buyers together directly and allow them to automate transactions through smart contracts. This model is equally suited to the shared economy. Consumers are increasingly becoming “prosumers,” simultaneously acting as providers and demanders of commodities without a middleman to coordinate them.

Since the operationalization of blockchain-based platforms and the transition to the other application areas is fluid, many blockchain applications can develop into such infrastructures. Due to the many stakeholders and the high relevance of smart contract functionality, implementation involves significant complexity. Organizations seeking blockchain-enabled platforms are classified as highly disruptive innovators.

Application, Discussion and Outlook

To illustrate the framework, a sample of Swiss blockchain and DLT fintechs was collected and assigned to the four application fields. The data for this was retrieved from Crunchbase, where searches for “blockchain,” “distributed ledger,” and ” fintech” yielded 47 hits. During a two-month search in March 2020, the individual services were analyzed, grouped, and assigned to the appropriate dimensions. If multiple services were offered, only the core services were considered. Three fintechs were not considered due to undefinable use cases. The results of the analysis are shown in the following table:

| Record Keeping | Automation | Tokenization | Platforming | |

| Cryptocurrencies | – | – | 10 | 2 |

| Asset Management | 1 | 1 | 4 | – |

| Custody | – | – | 4 | – |

| Token Issuance | – | – | 5 | – |

| Smart Contracts | – | 3 | – | – |

| Data Management | 3 | – | – | – |

| Reporting | 2 | – | – | – |

| Banking Infrastructure | – | 2 | – | 2 |

| Identity Management | – | 1 | – | 4 |

| Total in % | 14% | 16% | 52% | 18% |

Interestingly, more than 50% of all offerings in Switzerland are related to tokenization. Only 18% specialize in platforming, while 16% focus on process optimization. Record-keeping solutions are also underrepresented at 14%, although it can be assumed that these applications are in strong competition with traditional ICT. Although the results likely reflect an industry-specific focus and highlight application areas in a particular domain, the practicality of this framework needs to be further validated in practice. Nonetheless, the framework provides an initial guide for practitioners to make the topic of blockchain discussable as a first step. It represents an important step towards understanding and formalizing use cases in a new way.

For those who would like to delve deeper into the subject matter and terminology surrounding distributed ledger technology, we would like to recommend our Blockwiki.com.

[1] Anonymity, immutability, decentralization, transparency, single point of truth, programmability (you can read more in german on the CC Ecosystems Blog).

Sources

[1] S. Nakamoto, “Bitcoin: A Peer-to-Peer Electronic Cash System”, Whitepaper, 2008. [2] R. Beck, M. Avital, M. Rossi and J.B. Thatcher, “Blockchain technology in business and information systems research”, Business & Information Systems Engineering 59(6), 2017, 381-384. [3] M. Rossi, C. Mueller-Bloch, J. Thatcher and R. Beck, “Blockchain Research in Information Systems Current Trends and an Inclusive Future Research Agenda”, Journal of the Association for Information Systems 20(9), 2019, 1388-1403. [4] C. Christensen, The Innovator’s Dilemma: The Revolutionary Book that Will Change the Way You Do Business, HarperCollins, 2003. [5] M. Zachariadis, G. Hileman and S.V. Scott, “Governance and control in distributed ledgers: Understanding the challenges facing blockchain technology in financial services”, Information and Organization 29(2), 2019,105-117. [6] C. Catalini and J.S Gans, “Some Simple Economics of Blockchain”, Communications of ACM 63(7), 2016, 80-90. [7] A. Mooney, Blockchain ‘could save asset managers $2.7bn a year’, Financial Times, 2018, https://www.ft.com/content/b6171016-171f-11e8-9e9c-25c814761640