154 Years of Fintech, 100% Hype, 0% Revolution

Claims such as “robo advisors will replace bankers” or “banks will have disappeared” could be read frequently over the last decade in connection with accelerated digitization. However, the technological development in the financial industry is nothing new, in fact, only the way of doing banking today and especially the speed of progress have changed. For more than 10 years, the new infrastructure – the smartphone – has offered entirely new possibilities, which make it possible to literally carry the bank in your pocket.

A Brief History of Financial Technology

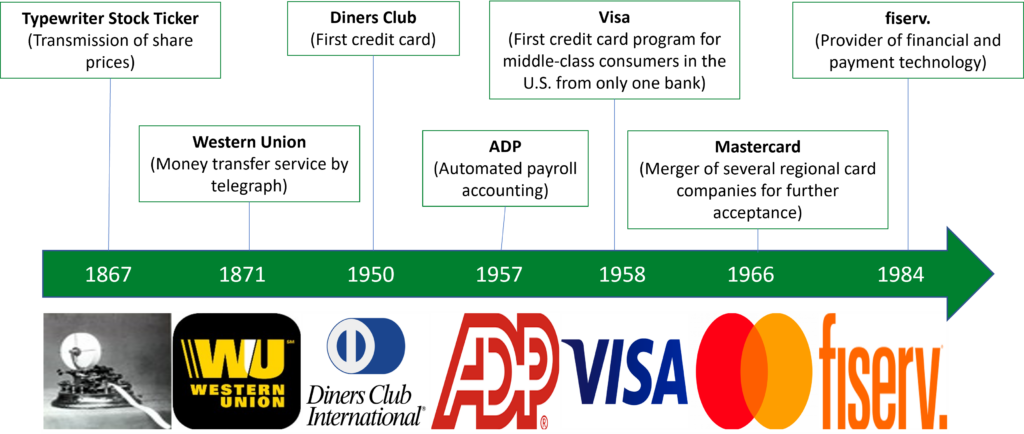

As mentioned earlier, the adaptation of new technologies is nothing new in the financial industry. In 2017, the ATM celebrated its 50th birthday (Reuters, 2017). Accordingly, it was already possible to withdraw money without the service of a bank employee in 1967, albeit at that time in physical form. Then in 1995, Security First Network Bank became the first bank to provide access to online banking (Humphreys, 1997). Similarly, the use of artificial intelligence by Capital One, founded in 1988, to reduce credit risks and increase revenue per customer in the credit card business is not new (Capital One, n.d.). At that time, personalized offers were already recommended to customers based on their data and behavior. Among other things, this led to them using the card more and, as a result, Capital One’s revenue rose steadily. The analyses also helped to adjust interest rates to an appropriate level for different cards (Dee, 2015). Customers with a low credit rating either paid a high interest rate or switched to another provider.

The following figure shows other examples of innovations in the financial industry in the order in which they occurred.

Financial Technology Today

Today, there is a whole range of technological applications in the financial industry. These are also called “fintech” for short, an abbreviation of “finance” and “technology”. The term fintech is associated primarily with young companies (start-ups) that develop innovative financial services. Examples of technology-based innovation projects and technologies in the financial sector, are for example the digitalization of processes, automation, robotics, processing of data, artificial intelligence, distributed ledger technology (DLT) or also quantum computing (Ankenbrand et al., 2021). In addition to the breakdown by technology area just mentioned, innovations can also be differentiated at the level of specific applications. A descriptive overview of fintechs in Switzerland is provided by Swisscom’s FinTech Startup Map (Swisscom, 2021). This map is divided into the four sectors Payment, Deposit & Lending, Banking Infrastructure and Investment Management and also lists the associated companies in the corresponding sector. The number of fintechs listed at the time of writing is 341, while the IFZ study speaks of 405 fintechs in its latest edition (Ankenbrand et al., 2021). Among other things, this is related to the different selection and admission procedures. For publication on the FinTech Startup Map, for example, it is assumed that the company has been in existence for no more than 10 years and focuses on innovative business models and new technology in the financial sector. The IFZ study also counts companies that are older than 10 years.

As figure 2 from CB Insights shows, there are other ways to categorize fintech applications (CB Insight, 2021). In addition to the applications already mentioned, the overview also lists insurance, wealth management and real estate. The associated fintech categories are InsurTech (Insurance + Technology), WealthTech (Wealth Management + Tech) and PropTech (Property + Tech).

Evolution or Revolution?

Although there are already numerous solutions and the applications and technologies are constantly evolving, fintechs in Europe have not yet succeeded in replacing the banker, let alone the banks in Europe. The majority of end customers continue to transact with traditional banks. As the article Robo-Advice – Replacement for the Human Investment Advisor? shows, the use of robo advisory services, for example, leads to a clear step backwards in terms of the quality of the customer advisory process. The NZZ sees further reasons for the lack of disruption in asset management in the small price difference between traditional asset managers and robo advisors, in a lack of trust, and in client inertia (Grundlehner, 2019). While it is thus hardly possible to speak of a revolution in Europe, it looks quite different in other parts of the world.

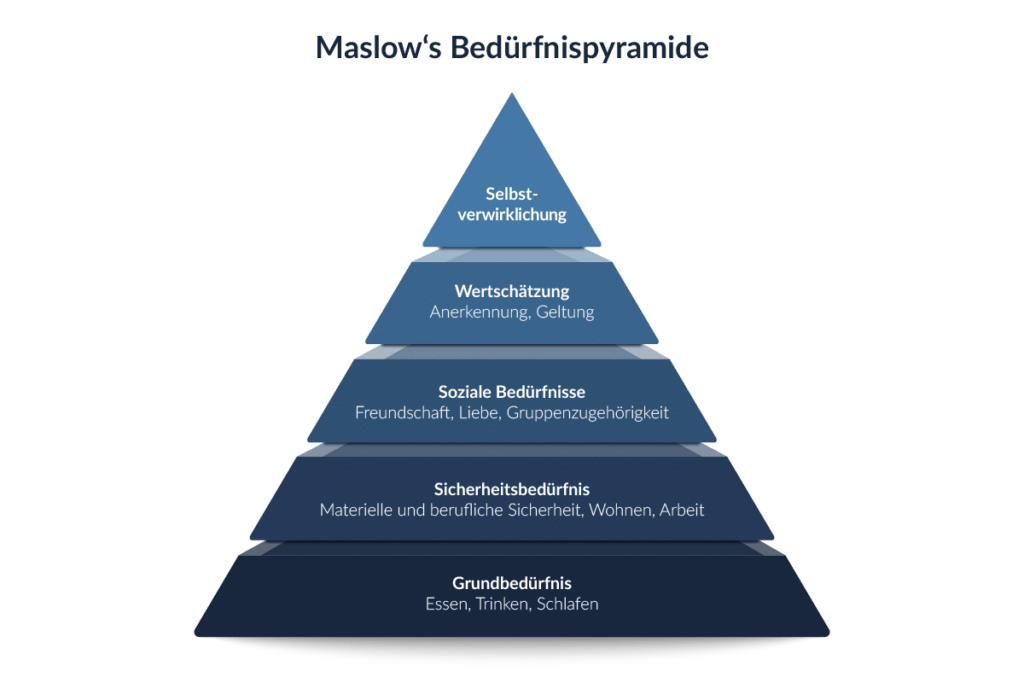

This phenomenon can be explained using Maslow’s pyramid (Figure 3):

Mr. and Mrs. Swiss are basically overbanked. This means that they generally maintain more than one banking relationship and can expand this and others as they wish. The fact that they can conveniently access modern infrastructure in the form of stores and branches means that they do not necessarily have to use digital applications. Thus, in order to survive, the Swiss do not need a smartphone that gives them access to financial services, which they can then use to order food and pay for it securely. In other regions of the world, however, technology suddenly makes it possible to have an account or wallet for the first time, with which one can instantly send funds to relatives and cover basic, safety, and perhaps social needs. There, one has no choice to worry about data security or the like. This thesis can be confirmed approximately by looking at the payment app Twint: The pandemic turned physical contact into a threat, digital payment went from a nice but not really necessary convenience to a means to satisfy the basic need of health. This led to a strong demand for digital payment (Heim, 2021). In such a situation, users break away from the “luxury” of resisting the emerging technology in order to realize themselves through it.

Let us now turn to regions where many people lack access to basic financial services. According to Varga (2018), these include the Middle East, sub-Saharan Africa, Latin America and Asia. In 2014, the number of unbanked worldwide was over 2 billion people. Three years earlier, in 2011, 2.5 billion people were still without access to banking services, a decrease of 20% (Varga, 2018). Unbanked are individuals who do not have access to banking services due to a lack of infrastructure and, in some cases, identity. At this point I focus on the issue of infrastructure, the issue of identity will not be discussed further here. The development of technology, especially the advent of smartphones, has made it possible for even rural residents to access financial services easily and conveniently. Sudden access to a savings account, the ability to transfer money, and loans allows people to escape poverty. This is one of the reasons why the use of new technologies is not a question of age in these regions, compared to Europe. In developing countries, there is evidence of very high activity even among older generations (UY, 2017). The prosperity of people and banks in Europe leads us to speak of a technological evolution here, whereas in Asia and Africa, for example, we can speak of a revolution. The banks are left out and the end customer is served directly by the emerging fintechs, because the banks with their legacy systems cannot keep up with technological developments and take far too long to implement new ideas. In China, the penetration of fintech applications in the payment sector is over 67% (PWC, 2017). In Europe, the penetration is half as much (33%), according to Finextra (2018). It is not a question of age, but of culture.

The example of Alipay, which Christian Betz analyzed on this blog, underscores this statement and shows how far the adaptation of the emerging financial technology has progressed in China. The platform can be used not only to order everyday goods and services, but also to make payments, take out loans (Tudor-Ackroyd & Bray, 2020) and arrange installment payments (Alipay, 2021). If money is left over at the end of the month, it can be invested in the Yu’e Bao money market fund at the touch of a button (Detrixhe, 2020; Valentova, 2015), which is one of the largest money market funds in the world. The development of such platforms and business ecosystems is another consequence of the fintech movement[1].

Will Banks in Switzerland Disappear?

No. Banks will adapt to the circumstances, just as they have done in recent decades. Dealing with new technologies is nothing new for them. While individual fintechs only map parts of the value chain, the bank covers the entire chain (Panetta, 2018). The customer also benefits from a single personal contact to whom they also entrust personal data. The examples of TrueWealth (finews.ch, 2019), Scalable Capital (Schneider, 2019) and Investomat of Glarner Kantonalbank (Fintechnews, 2019) show that the targeted B2C model does not (yet) work in Switzerland, but can be helpful for a bank as an efficiency enhancer, as TrueWealth proves.

It will be other reasons that will cause a bank to disappear from the banking map, such as acquisitions or crises. Or is it perhaps the TechFins?

[1] This blog post enables you to get a good foundation on the topic of business ecosystems.

Image Sources for Figure 1

Typewriter: Stock Tickers – The Edison Papers (rutgers.edu)

Western Union: Western Union IN – Send Money Transfers Quickly – Applications sur Google Play

Diners Club: Datei:Diners Club Logo.svg – Wikipedia

{kind=link}

ADP; Payroll, HR and Tax Services | ADP Official Site

Visa: Visa Logo | The most famous brands and company logos in the world (logos-world.net)

Mastercard: Mastercard Logo | The most famous brands and company logos in the world (logos-world.net)

Fiserv: Fiserv – Wikipedia

Sources

Ankenbrand, T.; Lötscher, D.; Bieri, D.; Grau, M.; Frigg, M. (2021): IFZ FinTech Study 2021 – An Overview of Swiss FinTech. Available at https://blog.hslu.ch/retailbanking/files/2021/03/IFZ-FinTech-Study-2021.pdf, checked on 03/07/2021.

Alipay (2021): Credit Pay Installment. Introduction. Available at https://global.alipay.com/docs/ac/creditpayinstallment/intro, checked on 08/21/2021.

Capital One (o. D.): Capital One Public Community Commitment Available at https://www.capitalone.com/media/doc/about/capital-one-public-community-commitment.pdf, checked on 03/07/2021.

CB Insight (2021): State Of Fintech Report: Investment & Sector Trends To Watch. Available at https://www.cbinsights.com/reports/CB-Insights_Fintech-Report-Q4-2020.pdf?utm_campaign=marketing_fintech_q4-2020-12&utm_medium=email&_hsmi=107280634&_hsenc=p2ANqtz-8pAaHLK-PyZl82Hu3WX2EEe6ahIJpMvSa_1drQ-1cRa7dEqzqySsX4KkRh0kAZ_ogvo-ShmF-bklRWFEbM6dFHTyGDXA&utm_content=107280634&utm_source=hs_automation, checked on 03/07/2021.

Dee, S. (2015): How Does Capital One Differentiate Itself In The Card Industry? In Forbes, 2015. Available at https://www.forbes.com/sites/greatspeculations/2015/09/11/how-does-capital-one-differentiate-itself-in-the-card-industry/?sh=3eea8a623cda, checked on 08/11/2021.

Detrixhe, J. (2020): Ant Financial’s Yu’e Bao is no longer the world’s biggest money market fund. In Quartz, 08.01.2020. Available at https://qz.com/1791778/ant-financials-yue-bao-is-no-longer-the-worlds-biggest-money-market-fund/, checked on 03/07/2021.

finews.ch (2019): True Wealth: Schweizer Robo-Pionier expandiert ins Ausland. Available at https://www.finews.ch/news/banken/39163-true-wealth-oesterreich-erste-gruppe-saas, updated on 03/07/2021, checked on 03/07/2021.

Finextra (2018): European Fintech: Trends, Adoption and Investment. Available at https://www.finextra.com/blogposting/15241/european-fintech-trends-adoption-and-investment, checked on 11.08.2021.

Swisscom (2021): FinTech Startup Map. With assistance of Swisscom, Fintechdb, e-foresight, IFZ. Available at https://fintechmap.ch/, checked on 03/07/2021.

Fintechnews (2019): Schweizer Robo Advisor Pionier Bank Schliesst Robo Advisor Angebot. In FinTech News Schweiz, 9/25/2019. Available at https://fintechnews.ch/roboadvisor_onlinewealth/investomat-glkb-robo-advisor-pionier-schliesst-robo-advisor/30852/, checked on 03/07/2021.

Grundlehner, W. (2019): Warum es die Robo-Advisors noch nicht aus der Nische schaffen. In Neue Zürcher Zeitung, 9/15/2019. Available at https://www.nzz.ch/finanzen/die-robo-advisor-schaffen-es-nicht-aus-der-nische-ld.1507314, checked on 03/07/2021.

Heim, M. (2021): Twint profitiert von Corona. In Handelszeitung, 3/7/2021. Available at https://www.handelszeitung.ch/unternehmen/twint-profitiert-von-corona, checked on 03/07/2021.

Humphreys, K. (1997): Banking and Finance on the Internet. Banking on the Web: Security First Network Bank and the Development of Virtual Financial Institutions.

Lunden, I. (2017): Alibaba taps Kabbage to loan up to 150k to SMBs after it quietly acquired OpenSky to ramp in North America. Available at https://techcrunch.com/2019/01/14/alibaba-taps-kabbage-to-loan-up-to-150k-to-smbs-after-it-quietly-acquired-opensky-to-ramp-in-north-america/, checked on 08/11/20211.

Panetta, F. (2018): Fintech and banking: today and tomorrow. Available at https://www.bancaditalia.it/pubblicazioni/interventi-direttorio/int-dir-2018/panetta-120518.pdf, checked on 03/07/2021.

PWC (2017): Payment, Deposit & Lending, Banking Infrastruktur und Investment Management. Available at https://www.pwccn.com/en/financial-services/publications/fintech/global-fintech-survey-china-summary-jun2017.pdf, checked on 03/07/2021.

Reuters (2017): World’s first ATM machine turns to gold on 50th birthday. Available at https://www.reuters.com/article/us-atm-anniversary-idUSKBN19I166, checked on 03/07/2021.

Schneider, K. (2019): Scalable Capital stellt sein Geschäft in der Schweiz ein. In Handelsblatt, 8/11/2019. Available at https://www.handelsblatt.com/finanzen/anlagestrategie/trends/robo-advisor-scalable-capital-stellt-sein-geschaeft-in-der-schweiz-ein/25203840.html?ticket=ST-12259940-2sXtTlcKTGR0NokMkoRe-ap6, checked on 03/07/2021.

Tudor-Ackroyd, A. & Bray, C. (2020). What is Jack Ma’s Ant Group and how does it make money). Shouth China Moring Post. https://www.scmp.com/business/banking-finance/article/3107294/what-jack-mas-ant-group-and-how-does-it-make-money

Uy, R. (2017): China, India post highest fintech adoption rates in Asia Pacific. Available at https://asianbankingandfinance.net/financial-technology/exclusive/china-india-post-highest-fintech-adoption-rates-in-asia-pacific, checked on 08/11/20211.

Valentova, E. (2015): Yu’E Bao turned 185M e-commerce customers into financial investors. Available at https://digital.hbs.edu/platform-digit/submission/yue-bao-turned-185m-e-commerce-customers-into-financial-investors/, checked on 08/11/20211.

Varga, David (Ed.) (2018): FINTECH: SUPPORTING SUSTAINABLE DEVELOPMENT BY DISRUPTING FINANCE. Spring Wind 2018. Gyor, Hungary.

- OKR – The Key to a Successful Company - 01.03.2022

- 154 Years of Fintech, 100% Hype, 0% Revolution - 27.08.2021

- The Intelligent Future of the Financial Industry – the Business Ecosystem - 12.08.2021